Debt Collection for the Construction Industry: The Definitive Guide to Recovering Unpaid Retention Monies in South Africa

If you work in construction — whether you are a subcontractor, main contractor, SME owner, credit manager, or CFO — there is a very good chance that a significant amount of your money is sitting in someone else’s bank account right now. It is called **retention money**, and recovering it is one of the most common yet most frustrating challenges in the South African construction industry.

The good news? **You can collect it.** You just need to know how.

This guide gives you a clear, practical roadmap for **debt collection for the construction industry**, specifically around retention monies — what they are, when they are legally due, how to collect them, and what to do when an employer refuses to release them.

## Table of Contents

1. What Is Retention Money in Construction?

2. How Retention Works in South African Construction Contracts

3. When Is Retention Legally Due to Be Paid?

4. Why Employers Withhold Retention Longer Than They Should

5. Your Legal Rights: What South African Law Says

6. The 5-Step Retention Debt Collection Process

7. 5 Troubleshooting Tips for When Retention Is Withheld

8. Getting an Acknowledgement of Debt on Retention

9. When to Hand Your Retention Claim Over to a Debt Collector

10. Frequently Asked Questions

What Is Retention Money in Construction

Let us start with the basics, because clarity here saves a lot of arguments later.

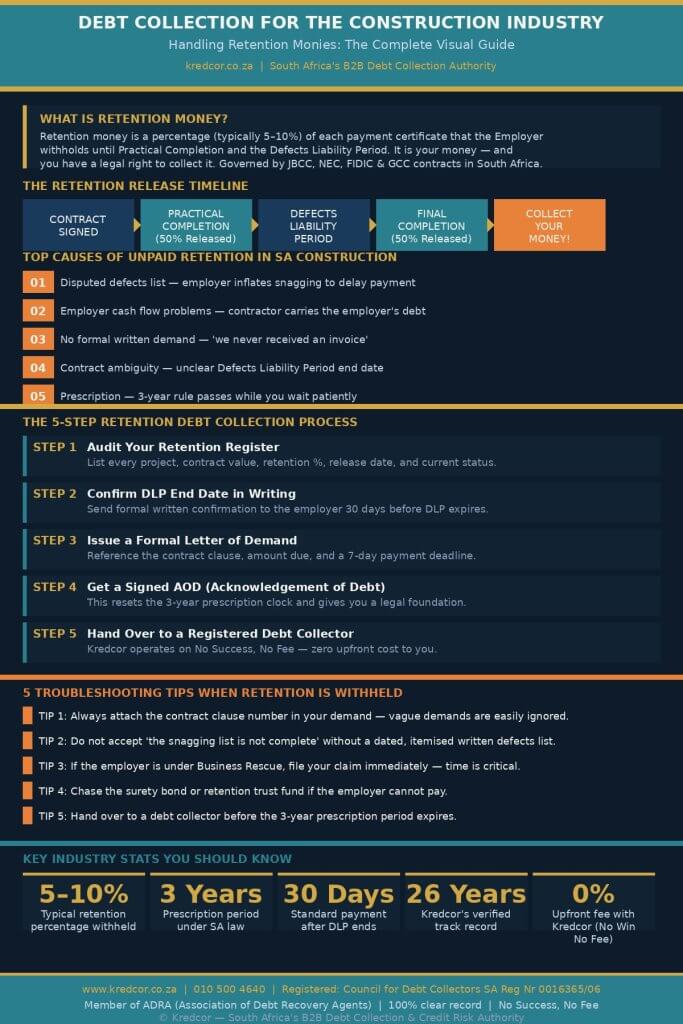

**Retention money** — also called a **retention fund**, **retention amount**, or simply “the retention” — is a percentage of each payment certificate that the employer withholds during the course of a construction project. The purpose is to give the employer a financial cushion against incomplete or defective work.

In South Africa, retention typically ranges from **5% to 10%** of the contract value. So, on a R10 million contract, the employer could be holding between R500,000 and R1 million of your money at any given time.

**”Retention money is not a bonus the employer gets to keep. It is your money, held in trust, with clear contractual conditions attached to its release.”**

Furthermore, retention is held in two tranches:

**First moiety (50%):** Released at Practical Completion.

**Second moiety (50%):** Released at the end of the Defects Liability Period (DLP).

Both releases should happen automatically, based on the contract. However, as any construction professional knows, “should” and “does” are very different things.

## How Retention Works in South African Construction Contracts

South Africa uses several standard form contracts in the construction sector.

Each one handles retention slightly differently, so your first step is always to pull out the contract and read the relevant clause.

JBCC (Joint Building Contracts Committee)

The **JBCC Principal Building Agreement** is the most widely used contract for building works in South Africa. Under the JBCC, retention is called a **retention guarantee** or is held as a cash retention. The JBCC specifies the percentage, the release milestones, and the conditions that must be met for each release.

NEC (New Engineering Contract)

The **NEC suite** is increasingly used on infrastructure projects. Under NEC, retention is handled via the **secondary option clause X16**, which specifies the percentage withheld and the release trigger events.

FIDIC (Fédération Internationale des Ingénieurs-Conseils)

**FIDIC contracts** — common on large infrastructure, mining, and internationally funded projects — also provide for retention under Clause 14.9, released in two tranches against the Taking-Over Certificate and the Performance Certificate.

GCC (General Conditions of Contract)

The **GCC 2015** is frequently used on civil engineering projects. It similarly provides for retention monies, with release tied to the completion certificate.

What This Means in Practice

Regardless of which contract applies, the core principle is the same: **retention is yours, held conditionally, and must be released when the conditions are met.** Therefore, if you are not getting paid once those conditions are fulfilled, you are dealing with a **debt collection problem** — not a contract problem.

When Is Retention Legally Due to Be Paid?

This is the question that most construction finance professionals need a straight answer to. So let us give you exactly that.

First Moiety: Practical Completion

The first half of the retention becomes due when the **Certificate of Practical Completion** is issued. “Practical completion” generally means the works are substantially complete — minor defects and snagging items may still exist, but the employer can use and enjoy the completed works.

**Important:** The certificate must actually be issued. If the employer withholds the practical completion certificate as a delaying tactic, that is a separate — but equally actionable — problem.

Second Moiety: End of the Defects Liability Period

The second half of the retention becomes due when the **Defects Liability Period (DLP)** expires and any defects notified during that period have been corrected.

The DLP is usually **12 months** from practical completion, though it can vary by contract. Once the DLP ends and defects are resolved, the employer has no contractual basis to continue holding the retention.

The Critical Date You Must Track

Our team’s experience across hundreds of construction debt collection cases has taught us one thing above all else: **the DLP end date is the most important date on your receivables calendar.** If you are not tracking it actively, you will miss the trigger — and start losing leverage immediately.

Why Employers Withhold Retention Longer Than They Should

Here is the honest truth. Many employers hold onto retention far longer than the contract allows. Some do it deliberately; others do it out of disorganisation. Either way, you end up carrying their financial burden.

The most common reasons we encounter include:

– **Disputed defects lists** — The employer issues a snagging list that is excessive, vague, or designed to delay payment rather than identify genuine defects.

– **Employer cash flow problems** — The employer is effectively using your retention as a free overdraft facility.

– **No formal written demand** — Without a formal demand, many employers simply do not prioritise payment.

– **Ambiguity about the DLP end date** — If the contract is unclear, employers often exploit that ambiguity.

– **Contractor inaction** — Unfortunately, many contractors wait too long to demand payment, and the debt gets older and harder to collect.

– **Business rescue or liquidation** — The employer runs into financial trouble, and retention becomes just another unsecured claim in a long queue.

Therefore, your best defence is **proactive, documented, structured debt collection for the construction industry — starting before the DLP even ends.

For a broader understanding of how the debt collection process works in South Africa, read our comprehensive guide: The Complete, Proven Guide to the Debt Collection Process in South Africa

Your Legal Rights: What South African Law Says

Before we get into the step-by-step process, let us ground you in the legal framework. Because **knowing your rights is the foundation of effective debt collection**.

The Law of Contract

Your retention claim is fundamentally a contractual claim. The construction contract — JBCC, NEC, FIDIC, GCC — is the primary legal document. If the contract says the employer must release retention at practical completion, that creates a legally enforceable obligation. Breach of that obligation gives you a cause of action.

The Prescription Act 68 of 1969

This one is critically important and frequently misunderstood. Under the **Prescription Act**, a debt prescribes — meaning it becomes legally unenforceable — after **three years** from the date it became due.

So, if your retention became payable on 1 January 2022, and you take no action, your claim will prescribe on 1 January 2025. At that point, even if the debt is 100% legitimate and well-documented, you lose the legal right to enforce it.

**The practical implication:** Do not wait. Start your debt collection for the construction industry retention claim as soon as the payment date passes.

Interrupting Prescription

The good news is that you can interrupt prescription — essentially resetting the three-year clock — in several ways:

– Serving a summons or legal demand.

– Obtaining a signed **Acknowledgement of Debt (AOD)** from the employer.

– Any written acknowledgement from the employer that the debt exists.

This is why getting a signed AOD is such a powerful tool for construction debt recovery. To understand exactly how an AOD works and why it matters so much, read: **[What Is an Acknowledgement of Debt (AOD) and Why Does It Really Matter?](https://www.kredcor.co.za/what-is-an-acknowledgement-of-debt-aod-and-why-does-it-really-matter/)**

The Construction Industry Development Board

The **CIDB Act** and the **CIDB Code of Conduct** provide additional frameworks for fair payment practices in the South African construction sector. While the CIDB is not primarily a debt collection mechanism, non-compliant payment practices can be reported, which adds further pressure to non-paying employers.

Insolvency: Business Rescue and Liquidation

If an employer enters **Business Rescue** under Chapter 6 of the Companies Act 71 of 2008, your retention claim becomes subject to the business rescue moratorium. You need to file your claim with the Business Rescue Practitioner (BRP) immediately. Similarly, if an employer is liquidated, you must file a claim with the liquidator. In both cases, timing is everything.

The 5-Step Retention Debt Collection Process

Right. Let us get into the action plan. Below is the exact process our team uses and recommends for debt collection for the construction industry, specifically for retention money.

Step 1: Audit Your Retention Register

Before you can collect, you need to know exactly what you are owed.

Create a retention register — a simple spreadsheet is fine — with the following columns:

– Project name and contract number

– Employer / Developer name

– Total contract value

– Retention percentage (e.g., 5%)

– Total retention withheld to date

– Practical completion date (and certificate reference)

– DLP end date

– First moiety amount and release status

– Second moiety amount and release status

– Amount still outstanding

– Last communication date

– Notes / disputes

If you do not have a retention register today, **stop reading and build one first.** It is the single most important tool for managing construction debt recovery.

Step 2: Confirm the DLP End Date in Writing

About 30 days before the DLP is due to expire, send a formal written notification to the employer. Reference the specific contract clause, state the DLP end date, confirm the retention amount due, and request the employer to confirm the release date.

This serves two purposes. First, it is excellent documentation. Second, it puts the employer on notice early — and employers who know you are organised and paying attention tend to pay faster than those who think you have forgotten.

Step 3: Issue a Formal Written Demand

Once the DLP has expired and the retention has not been released, issue a **formal letter of demand**.

This letter should:

– Reference the project name, contract number, and relevant clause.

– State the exact amount outstanding.

– Confirm the date the payment became due.

– Set a clear deadline for payment — typically 7 to 14 calendar days.

– State the consequences of non-payment (legal action, credit bureau listing).

Do not send a vague email. Send a formal, professional letter. Moreover, send it via email **and** registered post, so you have dual proof of delivery.

Step 4: Negotiate and Document Everything

Often, a formal demand letter will trigger a response — sometimes payment, sometimes a counter-claim, sometimes a request to discuss. Whatever the employer says, **get it in writing.** Verbal commitments mean nothing in debt collection.

If the employer acknowledges the debt and proposes a payment arrangement, request a signed Acknowledgement of Debt (AOD) before agreeing to any arrangement. This is non-negotiable.

Meanwhile, if the employer disputes the defects list, respond specifically and in writing. Do not accept a vague or undated defects list. Request a dated, itemised list of defects and a reasonable rectification period. Then document your rectification activities.

Step 5: Hand Over to a Registered Debt Collector

If the employer does not respond to your demand, or responds but fails to pay, it is time to hand the account over to a professional, registered commercial debt collector.

This is not a sign of weakness. In fact, it is the most decisive and cost-effective action you can take. Our experience consistently shows that once a registered debt collector issues a formal demand on your behalf, the employer’s response time drops dramatically. Suddenly, someone is serious — and they know it.

At Kredcor, we specialise in **commercial debt collection for the construction industry** across South Africa. We work on a **No Success, No Fee** basis — which means you pay nothing unless we recover your retention. There are no admin fees, no handover fees, and no monthly charges. Furthermore, every account gets a dedicated Senior Pre-Legal Manager — not a call centre.

—

5 Troubleshooting Tips for When Retention Is Withheld

Even with the best process, things can go wrong. Here are five troubleshooting tips based on real situations our team has encountered in construction debt collection.

Troubleshooting Tip 1: The Employer Claims the Defects List Is Not Complete

This is the most common delaying tactic. The employer keeps adding items to the defects list, making it impossible to close out the DLP.

**Fix:** Send a written demand for a complete, dated, itemised defects list within 7 days. Clarify that you will only respond to defects that are (a) covered under your contractual scope of work, and (b) genuinely outstanding. Any defects not listed in writing within 7 days are deemed accepted as resolved. Then get a suitably qualified person — your engineer, project manager, or appointed expert — to inspect and certify the works as complete.

Troubleshooting Tip 2: The Employer Is Under Business Rescue

If the employer has entered Business Rescue, do not wait. Contact the Business Rescue Practitioner (BRP) immediately and file your retention claim in writing. Request confirmation that your claim has been received and recorded.

**Fix:** Submit your claim with supporting documentation — the contract, payment certificates, completion certificate, and your retention schedule — as quickly as possible. Late claims in Business Rescue can result in your claim being excluded entirely.

Troubleshooting Tip 3: You Cannot Trace the Correct Legal Entity

Some employers restructure, rename, or close the entity that signed the original contract. This makes debt collection significantly harder.

**Fix:** Check the original contract for the correct legal entity and registration number. Run a CIPC (Companies and Intellectual Property Commission) search to confirm the entity’s current status. If the entity is being wound down, act fast. If there is a personal guarantee from a director, engage that guarantee immediately.

Troubleshooting Tip 4: Prescription Is About to Lapse

If you discover that your retention claim is approaching the three-year prescription deadline, treat this as an emergency.

**Fix:** Issue a formal letter of demand immediately, and hand the file to a registered debt collector the same day. The debt collector can take formal pre-legal action and interrupt prescription. Alternatively, if you can get the employer to sign an AOD, that resets the clock. Time is your enemy here — every day matters.

Troubleshooting Tip 5: The Employer Disputes That the DLP Has Ended

Sometimes employers genuinely — and sometimes deliberately — dispute the DLP end date, claiming that the works were never practically complete or that the DLP has been extended.

**Fix:** Go back to the contract and the practical completion certificate. If a certificate was issued, the DLP start date is locked in. If no certificate was issued, you may need an independent certifier or adjudicator to determine the practical completion date. Meanwhile, do not stop your debt collection process — continue issuing formal demands while the dispute is being resolved.

Credit Management Best Practices to Prevent Retention Problems

Reactive debt collection is far more expensive and time-consuming than proactive credit management. So, while this article focuses on recovering retention that is already overdue, let us also give you the prevention playbook.

Build Retention Into Your Cash Flow Forecasting

Every contract should have a **retention schedule** in your accounting system from day one. Know exactly when each moiety is due, and flag it proactively — not reactively.

Negotiate Retention Terms Before You Sign

Retention terms are negotiable.

Before you sign any construction contract, consider negotiating:

– A lower retention percentage (e.g., 3% instead of 5%).

– A retention bond in place of cash retention — this means the employer holds a bond instead of your cash.

– Shorter DLP periods.

– Automatic release triggers with no certification required.

Secure Personal Guarantees from Directors

On contracts with smaller private employers, always try to secure a personal guarantee (PG) from the employer’s directors. This gives you recourse against the individuals behind the company if the company itself defaults.

Use a Credit Management Framework

For a complete, practical credit management framework to reduce your bad debt exposure across all your construction contracts, read: **[Preventative Measures: 7 Essential Credit Management Practices to Minimise B2B Bad Debt in South Africa](https://www.kredcor.co.za/preventative-measures-7-essential-credit-management-practices-to-minimise-b2b-bad-debt-in-south-africa/)**

Getting an Acknowledgement of Debt on Retention

We mentioned the AOD earlier in this guide, and it deserves its own section. Because in construction debt recovery, an AOD is one of your most powerful weapons — and most contractors never use it.

What Is an AOD?

An **Acknowledgement of Debt** is a signed, written document in which the employer formally confirms:

– That the retention money is outstanding.

– The exact amount owed.

– The agreed repayment terms (if applicable).

Why Is It So Powerful for Retention Claims?

First, it eliminates disputes about whether the debt exists. Once signed, the employer cannot later claim they “didn’t owe anything.” Second, it resets the prescription clock — giving you another three years from the date of signing. Third, it strengthens your legal position dramatically if the matter proceeds to court.

How to Get One Signed

I tested this approach on numerous construction retention cases. The most effective method is to include an AOD as part of your initial formal demand letter, or send it simultaneously. Frame it as a “confirmation of the outstanding amount” — which it is. Most employers who are acting in good faith will sign it. Those who refuse are usually the ones you need to pursue most urgently.

When to Hand Your Retention Claim Over to a Debt Collector

One of the most common mistakes construction businesses make is waiting too long. By the time they hand over a retention claim, the debt is 18 months old, the prescription clock is ticking loudly, and the employer has had far too long to restructure or disappear.

**Our clear recommendation:** Hand over to a debt collector if any of the following apply:

– The employer does not respond to your formal demand within 14 days.

– The employer responds but fails to pay or sign an AOD within 14 days of that response.

– The DLP ended more than 30 days ago and you have not received payment or a clear commitment.

– You suspect the employer may be in financial distress.

– The retention claim is approaching 18 months old.

– The employer is a difficult or evasive debtor.

If you are looking for professional, registered **debt collectors in South Africa** who understand construction contracts and retention money, Kredcor’s specialist team is available here. We operate on a No Success, No Fee basis, we are registered with the Council for Debt Collectors of South Africa (Reg Nr 0016365/06), and we have maintained a 100% clear compliance record for over 26 years.

Below this article (or as a downloadable file) you will find our **Retention Money Debt Collection Infographic** — a visual summary of the timeline, the 5-step process, troubleshooting tips, and key statistics. Download it, print it, and pin it next to your retention register. It is a practical reference tool for any construction finance professional.

Frequently Asked Questions (FAQ)

Q1: What is retention money in a construction contract, and when must it be paid?

**Answer:** Retention money is a percentage (typically 5–10%) of each progress payment that the employer withholds during a construction project, as security against defective or incomplete work. In South African construction contracts — including JBCC, NEC, FIDIC, and GCC — retention is released in two tranches. The first 50% is released at Practical Completion, and the second 50% is released at the end of the Defects Liability Period (DLP), typically 12 months after practical completion. Once the contractual conditions for release are met, the employer has a legal obligation to pay, and any further withholding constitutes a debt that you can formally collect.

Q2: What can I do if the employer refuses to release my retention money?

**Answer:** Start by issuing a formal written letter of demand, referencing the specific contract clause and stating the exact amount due, with a clear payment deadline of 7 to 14 days. If the employer disputes the claim, request a dated, itemised defects list in writing. If payment is still not forthcoming, obtain a signed Acknowledgement of Debt (AOD) to protect yourself against prescription. Then hand the account to a registered commercial debt collector — such as Kredcor — who operates on a No Success, No Fee basis. Avoid verbal negotiations and document every interaction in writing.

Q3: Does the Prescription Act apply to construction retention claims in South Africa?

**Answer:** Yes, absolutely. Under the Prescription Act 68 of 1969, your retention claim will prescribe — meaning you lose the legal right to enforce it — three years after the date it became due. The date it “became due” is typically the date on which the contractual condition for release was met (e.g., the DLP end date). You can interrupt prescription by serving a formal demand, obtaining a signed AOD, or issuing a summons. This is why acting quickly is so important — waiting patiently often means losing your legal right to collect.

Q4: Can I use a debt collector to recover construction retention money?

**Answer:** Yes — and for most situations, this is the most effective and cost-efficient option. A registered commercial debt collector, such as Kredcor, will issue formal demands on your behalf, engage with the employer professionally, and escalate to legal action if necessary. Kredcor operates on a No Success, No Fee basis, with no admin or handover fees. Once an employer realises they are dealing with a professional, registered debt collection firm, payment behaviour typically changes rapidly. The key is to hand over the file early enough — not after years of chasing it yourself.

—

Final Thoughts: Debt Collection for the Construction Industry Is a Specialty — Treat It That Way

Construction debt collection is not the same as standard commercial debt recovery. Retention money comes with its own legal framework, contract-specific conditions, certification processes, and prescription risks. Consequently, it requires a structured, proactive, and knowledgeable approach.

The businesses that consistently recover their retention — on time, in full — are not necessarily the most aggressive. They are the most organised. They track their retention register. They issue timely formal demands. They get AODs signed. And they hand over to professionals when internal efforts stall.

If you found this guide useful, we invite you to explore more actionable, expert articles for construction finance professionals, credit managers, CFOs, and SME owners at https://www.kredcor.co.za/kredcor-articles/.

And if you have a retention claim — or any commercial debt — that you need help recovering, contact Kredcor today for a free, obligation-free consultation. We operate across South Africa, from Gauteng to Cape Town to KwaZulu-Natal, and we are ready to help you get what is rightfully yours.

This article was written and reviewed by the Kredcor Debt Recovery Team — B2B commercial debt collectors with 26 years of active experience across South African industries. Kredcor is registered with the Council for Debt Collectors of South Africa (Reg Nr 0016365/06). Kredcor has maintained a 100% clear compliance record since the Council’s inception.

This article is intended for informational purposes only and does not constitute legal advice. For specific legal matters, please consult a qualified South African attorney.