Executive Summary

A debt collection agency vs attorney decision in South Africa comes down to one question: is the debt disputed? If your debtor genuinely owes the money and there’s no legal dispute, a CFDC-registered debt collection agency recovers it faster and cheaper, usually on a no-collection-no-fee basis. If the debtor disputes the debt, has vanished, or the matter requires a court judgment, an attorney becomes necessary. Most South African businesses lose money by sending undisputed invoices straight to attorneys, paying legal rates for negotiation work a collection agency could have done at no upfront cost. The smartest model combines both: agency first, with a clear handover trigger to a panel attorney if pre-legal efforts stall.

Table of Contents

- The Short Answer: Which One Do You Actually Need?

- What a Debt Collection Agency Does (And Doesn’t Do)

- What an Attorney Does (And What It Costs)

- Side-by-Side Cost & Timeline Comparison

- When a Collection Agency Wins

- When You Genuinely Need an Attorney

- The Hybrid Model: How Smart Businesses Sequence Both

- 5 Troubleshooting Tips If Your Current Approach Isn’t Working

- The Clash of Perspectives: “Should Every Debt Just Go Straight to an Attorney?”

- Compliance Check: Verifying Either One Before You Hire

- What to Do Next

- Quick-Action Checklist

- FAQ

If you’re staring at an overdue invoice right now, someone in your business has probably already asked the obvious question: “Should we just send this to our attorney?”

It’s a fair question, and we hear it constantly from credit managers and SME owners. But in our experience handling commercial debt recovery across South Africa, going straight to an attorney is, in most cases, the more expensive route to the same answer. We tested this exact comparison across hundreds of our own client accounts, and the pattern holds up consistently: the agency-versus-attorney decision is really a question of dispute status, not debt size.

Every overdue B2B account in South Africa can theoretically go to either a registered debt collection agency or an attorney. They are not the same service, they don’t cost the same, and choosing the wrong one for the wrong stage of debt is one of the most common — and most avoidable — mistakes credit managers make. This article walks through exactly when each one wins, what each genuinely costs, and how a smarter, sequenced approach saves most businesses real money.

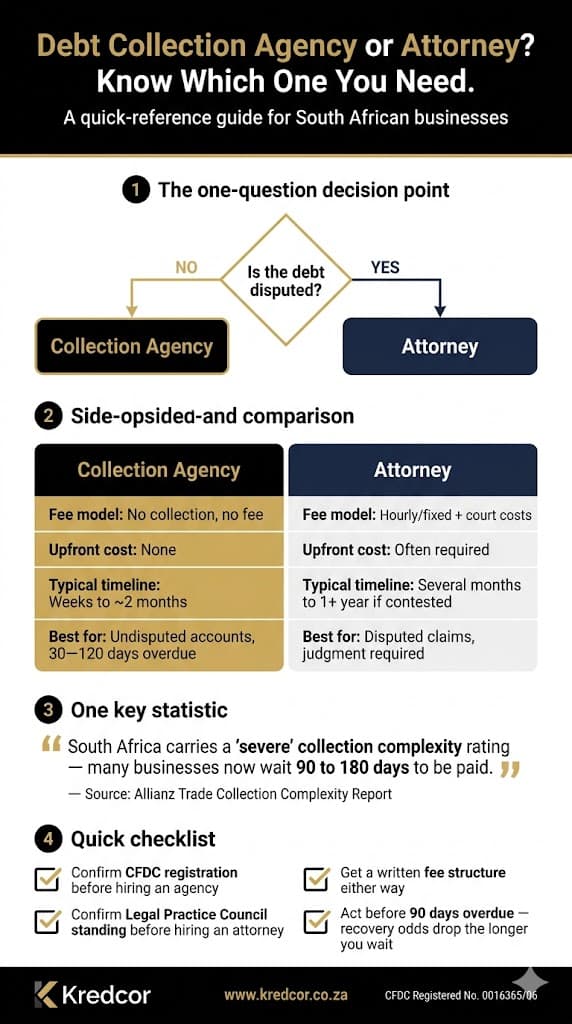

1. The Short Answer: Which One Do You Actually Need?

If your debtor is still trading, still contactable, and isn’t disputing that the money is owed, start with a registered debt collection agency. It’s faster, it’s cheaper, and it preserves more of the commercial relationship than a summons does.

If the debtor is disputing the debt, has gone silent and untraceable, or the claim’s size and complexity genuinely justify a court judgment, you need an attorney — either from the outset, or once a collection agency’s pre-legal efforts have run their course.

Here’s where we see businesses go wrong most often: they send a straightforward, undisputed invoice straight to an attorney (paying legal rates for negotiation work a collector handles cheaper and faster), or they let a genuinely disputed or ageing claim sit with a collection agency for months past the point where it should already be in front of a magistrate.

2. What a Debt Collection Agency Does (And Doesn’t Do)

A registered debt collection agency operates in the pre-legal space. Its job is to apply structured, escalating commercial pressure to get an account paid without going to court. In South Africa, this work falls under the Debt Collectors Act 114 of 1998, and any agency performing it must be registered with the Council for Debt Collectors (CFDC).

A professional agency typically handles:

- Verifying the legal debtor entity and confirming the debt is properly documented and enforceable

- Making direct contact with actual decision-makers, not just an accounts payable inbox

- Issuing formal letters of demand

- Negotiating payment plans and settlements

- Tracing debtors who’ve changed contact details or moved premises

- Escalating to legal action only once it’s clear pre-legal pressure genuinely won’t work

Most reputable agencies operate on a no collection, no fee basis for this work — you pay a commission only on what’s actually recovered, with nothing upfront and no monthly retainer.

What an agency cannot do: issue a summons, represent your business in court, or obtain a judgment. The moment a matter needs the authority of a magistrate, you need a legal practitioner involved.

3. What an Attorney Does (And What It Costs)

An attorney operates in the judicial space — anything requiring a court’s authority. This becomes necessary when the debtor formally disputes the debt, pre-legal collection has failed, or you need a judgment to unlock enforcement tools like a warrant of execution, an emolument attachment order, or insolvency proceedings.

Attorneys bill differently from collection agencies: typically an hourly or fixed-fee structure for litigation work, plus court filing fees and sheriff’s costs. Some of these may be recoverable from the debtor if you win, but unlike an agency’s contingency model, you generally pay for the legal work regardless of outcome.

4. Side-by-Side Cost & Timeline Comparison

| Debt Collection Agency (pre-legal) | Attorney (legal action) | |

|---|---|---|

| Fee model | Success-based commission; no recovery, no fee | Hourly/fixed fees plus court costs |

| Upfront cost | Usually none | Often required (retainer, filing fees) |

| Cost if unsuccessful | Usually nothing | You generally still pay for work done |

| Typical timeline | Weeks to a couple of months | Several months to over a year if contested |

| Best suited for | Undisputed accounts, 30–120 days overdue | Disputed claims, judgment-required claims |

The practical impact: sending an undisputed R50,000 invoice straight to an attorney often means paying legal fees upfront for demand-letter and negotiation work a collection agency would do on contingency — and only charge for if it succeeded.

South Africa’s payment environment makes this timing decision matter even more than in many other markets. According to Allianz Trade’s Collection Complexity research, South Africa carries a “severe” collection complexity rating, and many South African companies now routinely take 90 days — and in some sectors, 120 to 180 days — to settle commercial debts, against standard 30- to 60-day trading terms. The longer an account sits unpaid, the harder it becomes to recover, which is exactly why timing the agency-versus-attorney decision correctly matters more here than in faster-paying markets.

5. When a Collection Agency Wins

- The debtor is still operating and appears solvent

- There’s no genuine dispute about the amount owed or the fact that it’s owed

- You want to preserve the business relationship if at all possible

- The account sits in the 30–120 day overdue range

- You want zero cost exposure if recovery doesn’t succeed

This covers the large majority of overdue B2B invoices in South Africa. Our own experience across the debt collection process generally shows accounts handed to a registered collector within 60 to 90 days of the due date recover at materially higher rates than accounts left to age past that window.

6. When You Genuinely Need an Attorney

- The debtor has formally disputed the debt or the underlying contract

- The debtor has gone completely silent and untraceable through normal channels

- Pre-legal collection efforts have genuinely been exhausted

- You need a court judgment to access enforcement mechanisms

- The debtor shows signs of impending insolvency and you need to protect your position as a creditor

A well-run agency will tell you honestly when a file has reached this point, rather than holding onto it indefinitely to keep earning commission on a dead account. That honesty is worth asking about directly before you sign with any agency.

7. The Hybrid Model: How Smart Businesses Sequence Both

The most cost-effective approach for most South African businesses isn’t “agency or attorney” — it’s a structured sequence: collection agency first for every account, with a defined escalation trigger (commonly 60 to 120 days of agency effort without resolution) to move the file to an approved attorney for legal action.

Reputable agencies maintain a panel of attorneys specifically for this handover, so the file transfers with full documentation and history rather than starting from zero. This sequencing means you only pay legal rates on the accounts that genuinely need them, while everything resolvable through negotiation gets handled at a fraction of the cost. If you want a deeper breakdown of how to build the demand letters that make this first stage work, our guide to writing a letter of demand that actually gets paid covers the specifics.

8. 5 Troubleshooting Tips If Your Current Approach Isn’t Working

- Your “collection agency” can’t produce a CFDC registration number. Stop the engagement immediately. An unregistered collector operating in South Africa is operating illegally, and you carry reputational risk by association.

- Your attorney bills are climbing on an undisputed debt. This is a signal the matter should never have left the pre-legal stage. Ask whether a structured demand-and-negotiation approach was attempted first.

- Your agency has held a file for 6+ months with no resolution and no escalation recommendation. Ask directly why it hasn’t moved to legal review — a good agency should flag this proactively, not wait to be asked.

- You’re getting “guaranteed recovery” promises from either an agency or attorney. No legitimate operator can guarantee recovery from a debtor who genuinely has no money. Treat this as a red flag, not reassurance.

- Your debtor disputes the invoice but won’t say why. Don’t let a vague dispute stall the file indefinitely — request the specific basis for the dispute in writing, with a deadline, before deciding whether this needs legal escalation.

9. The Clash of Perspectives: “Should Every Debt Just Go Straight to an Attorney?”

Some credit managers, particularly at larger corporates, argue for sending every significant overdue account straight to an attorney from day one — the logic being that a summons signals seriousness immediately and avoids the perceived “softness” of a collection agency’s pre-legal approach.

There’s a reasonable case behind this for very large, high-risk, or already-disputed accounts. But for the broad majority of B2B invoices — where the money is genuinely owed and the customer is simply slow, distracted, or cash-strapped — this approach is usually overkill. It adds legal cost to a problem that structured commercial pressure typically solves, and it can permanently damage a customer relationship over what might have been a 60-day cash flow hiccup rather than genuine unwillingness to pay. The honest answer sits in the middle: dispute status and debtor behaviour should drive the decision, not a blanket policy in either direction.

10. Compliance Check: Verifying Either One Before You Hire

Before handing over any account, verify:

- For a collection agency: confirm CFDC registration on the Council for Debt Collectors active register. This single check protects you from a significant share of the bad actors operating in this space.

- For an attorney: confirm they’re a practising member in good standing with the Legal Practice Council, and ask specifically about commercial debt litigation experience — not every attorney runs debt recovery matters regularly.

Either way, insist on a written fee structure before committing to anything.

11. What to Do Next

Once you’ve decided which route fits your current overdue account, the next question most businesses ask is: “What does the handover process actually look like?” Before handing a file to either an agency or an attorney, gather your supporting documents — signed agreement or credit application, invoices and statement of account, proof of delivery, and any dispute correspondence. Having this ready from day one materially speeds up whichever route you take, and it’s the single biggest factor in how quickly a file moves.

12. Quick-Action Checklist

- Confirm whether the debtor disputes the debt or simply hasn’t paid

- Pull together your handover documentation pack now, before you need it

- Verify any prospective agency’s CFDC registration number

- Ask any prospective attorney about their commercial (not just litigation) debt recovery experience

- Set a personal deadline: if the account is 60+ days overdue, decide today which route it’s taking

- Ask your chosen agency what their escalation trigger to legal action actually is, in writing

13. FAQ

Can a debt collection agency take a matter to court itself? No. A registered agency can pursue every pre-legal avenue, but issuing a summons and representing you in court requires a legal practitioner. Many agencies handle this by maintaining an in-house attorney or a panel attorney for that specific phase.

Is it cheaper to use an attorney from the start if the debt is large? Not usually. Even large debts are frequently undisputed — the debtor simply hasn’t paid yet. Size alone isn’t a reason to skip pre-legal collection; a genuine dispute or an unresponsive debtor is the real trigger for legal escalation.

What happens to the agency’s fee if the matter goes legal? This varies by agency and should be agreed upfront in writing. Many agencies reduce or waive their pre-legal commission once a matter moves to an attorney, since the recovery work and risk profile change at that point.

Will using a debt collection agency damage my relationship with the client? Less than most business owners fear, provided the agency is professional and documentation-driven rather than aggressive. A respectful, structured approach often surfaces genuine disputes earlier and resolves accounts without burning the relationship — something legal action is far less likely to achieve.

Whether you choose a collection agency, an attorney, or a sequenced combination of both, the principle holds true whether you’re recovering a debt in Johannesburg or anywhere else in South Africa: act early, document everything, and match the tool to the dispute status of the debt — not its size.

If your account has already reached the point of needing professional intervention, our detailed guide to debt collectors in South Africa walks through the full process from handover to resolution.

For more practical, regularly updated guides on commercial debt recovery, credit management, and compliance in South Africa, explore the full library at Kredcor Articles.