How Manufacturing Firms Handle Large-Scale Commercial Defaults: The Proven Survival Guide

Actionable strategies for credit managers, CFOs, and SME owners in the manufacturing sector — so you stop losing money on unpaid invoices and start recovering it.

By Kredcor — South Africa’s Commercial Debt Recovery Partners | Published: April 2026 | Read time: ~14 min

Picture this: you’ve just shipped a R400,000 order of steel components to a long-standing client. They’ve been reliable for three years. Then — nothing. Calls go unanswered. Emails bounce back. And your accounts-receivable aging report starts looking like a disaster zone. Welcome to the world of large-scale commercial defaults in the manufacturing sector — one of the most cash-flow-punishing situations any manufacturer, credit manager, or CFO can face.

The good news? Manufacturing firms across South Africa that handle large-scale commercial defaults well follow a clear, structured process. And in this guide, we break that process down completely — so you can act faster, recover more, and protect your business before the damage becomes permanent.

⚡ Quick Answer

How do manufacturing firms handle large-scale commercial defaults? They act through four structured stages: (1) internal escalation and account freeze within 30 days of default; (2) formal letter of demand and direct negotiation; (3) pre-legal intervention by a registered debt recovery agency; and (4) legal action as a final step. The single most important rule: act within 30–45 days of default. Recovery rates drop sharply after 90 days.

📋 Table of Contents

- What Is a Large-Scale Commercial Default in Manufacturing?

- Why Manufacturing Firms Are Especially Vulnerable

- Stage 1 — Internal Escalation: Stop the Bleeding Immediately

- Stage 2 — Formal Demand and Direct Negotiation

- Stage 3 — Pre-Legal Intervention: When to Call in the Professionals

- Stage 4 — Legal Action: The Last Resort (and How to Use It Right)

- The Infographic: Your 4-Stage Default Response Plan

- 5 Critical Troubleshooting Tips for Manufacturing Credit Teams

- How to Prevent Large-Scale Defaults Before They Happen

- LSI Terms and Semantic Clusters for Credit Managers

- Frequently Asked Questions (FAQ)

1. What Is a Large-Scale Commercial Default in Manufacturing?

A large-scale commercial default happens when a B2B client fails to pay one or more significant invoices — typically exceeding R50,000 — beyond the agreed payment terms. In manufacturing, these defaults are particularly damaging because the sector operates on thin margins, high input costs, and long production cycles.

Furthermore, unlike retail or professional services, manufacturing firms often extend substantial credit to distributors, wholesalers, and large retail chains. When one of those clients defaults, the ripple effect can cascade through your entire supply chain. Moreover, because manufacturing invoices are often tied to physical goods already delivered — and frequently non-returnable — the creditor has limited leverage by the time the default is discovered.

Related terms and synonyms you’ll encounter in this context include: commercial insolvency, debtor default, overdue receivables, unpaid trade invoices, B2B payment failure, non-payment of commercial debt, accounts receivable delinquency, and credit default in the industrial sector.

3 yrs

Prescription period for most SA commercial debts under the Prescription Act 68 of 1969

40–70%

More debt recovered by businesses with structured recovery processes vs reactive ones (Kredcor data)

2×

Recovery rate for accounts handed to professionals within 30–45 days vs. 90+ days

2. Why Manufacturing Firms Are Especially Vulnerable to Commercial Defaults

Before we get into solutions, it’s worth understanding why the manufacturing sector carries such elevated credit risk. After all, if you know the enemy, you can fight it more effectively.

Extended Payment Terms and Long Credit Cycles

Most manufacturers extend 30-, 60-, or even 90-day payment terms as standard practice. Consequently, by the time you realise a client has defaulted, the debt is already old. Additionally, many manufacturing firms deliver multiple orders on a running account — so a single client who stops paying can accumulate a massive balance very quickly before anyone notices the pattern.

Concentration Risk: Too Few Large Clients

Many manufacturing SMEs rely on a small number of high-volume clients. As a result, when one of those clients defaults at scale, the impact isn’t just uncomfortable — it can threaten the survival of the entire business. Our team at Kredcor has seen this pattern repeatedly: a manufacturer with five key clients loses one to default and suddenly faces a 20% cash-flow hole overnight.

Goods Already Delivered — Leverage Is Gone

Unlike a service business that can pause delivery, a manufacturer has usually already shipped the goods. Therefore, the debtor holds the product and the money. Unless you have a reservation of ownership clause in your terms, recovering the goods is often impractical — which makes recovering the cash even more urgent.

“In manufacturing, cash flow is king. The moment a large client defaults, you’re not just losing a receivable — you’re potentially losing your ability to pay your own suppliers. Act immediately. Don’t wait.”— Kredcor Senior Pre-Legal and Credit Risk Manager

3. Stage 1 — Internal Escalation: Stop the Bleeding Immediately

The first and most critical step when a large-scale commercial default occurs is to act fast — within your own business, before you involve anyone else. Here’s exactly what to do.

Freeze the Account Instantly

The moment a client’s account becomes significantly overdue — typically 30 days past due — freeze further deliveries. This sounds obvious, but surprisingly many manufacturers continue shipping to defaulting clients out of optimism or relationship preservation. Don’t. Every additional shipment increases your exposure and reduces your recovery position.

Escalate to Senior Management Immediately

A large-scale commercial default is not a job for a junior credit controller. Consequently, the moment an account hits a threshold you define in advance (for example, R100,000 overdue or 45 days past terms), it must land on the desk of your credit manager, financial manager, or CFO. Speed matters above all else.

Conduct an Internal Account Review

Before you contact the debtor formally, gather everything: all signed invoices, delivery notes, purchase orders, credit applications, your terms and conditions, and all communication history. This documentation forms the foundation of everything that follows — from your demand letter to a potential court case.

💡 Actionable Tip — Internal Process

Set a hard internal rule: if an account is 30 days overdue and no written payment arrangement exists, it immediately triggers a senior escalation meeting. No exceptions. This single rule, implemented consistently, will transform your recovery rates.

4. Stage 2 — Formal Demand and Direct Negotiation

Once you’ve completed your internal escalation, the next step is a formal letter of demand — followed by structured negotiation. This stage is where many manufacturers make costly mistakes, either by being too soft too long or by jumping straight to litigation unnecessarily.

Issue a Formal Letter of Demand

A well-drafted letter of demand does several important things simultaneously. First, it creates a legal paper trail. Second, it signals clearly that you’re serious about collecting. Third — and critically — it can interrupt prescription, meaning the 3-year clock on your debt resets from the date of the demand.

Your demand letter should clearly state the full amount owed, the payment deadline (typically 7–14 business days), the consequences of non-payment, and your right to recover collection costs. For a detailed guide on writing a demand letter that actually gets results, refer to the experts at The Complete, Proven Guide to the Debt Collection Process in South Africa.

Engage in Structured Debt Settlement Negotiations

If the debtor responds — and many will once they receive a formal demand — move straight into structured negotiation.

In our experience, the most common resolution structures for manufacturing defaults include:

- Structured payment plan: The full debt is acknowledged and repaid over agreed instalments — ideal when the debtor has the will but not the immediate liquidity.

- Acknowledgement of Debt (AOD) with consent to judgment: The debtor signs a formal AOD and consents to immediate judgment if they default on the plan. This gives you legal security while still allowing time to pay.

- Full and Final Settlement (FFS): A negotiated reduced amount, accepted as full settlement. Used when the debtor is in genuine financial distress and a reduced amount now is more valuable than the full amount never.

💡 Actionable Tip — Negotiation

Always try to isolate the undisputed portion of any invoice. If your client disputes R20,000 of a R200,000 invoice, demand payment of the undisputed R180,000 immediately and deal with the dispute separately. This keeps cash flowing while the argument is resolved.

5. Stage 3 — Pre-Legal Intervention: When to Call in the Professionals

If your internal efforts and formal demands produce no result — or if the debtor is actively avoiding contact — it’s time to hand the account to a registered commercial debt recovery agency. This is not a sign of failure. It’s a smart, strategic decision that dramatically improves your recovery outcome.

Why Pre-Legal Intervention Works

I tested the 90-day rule extensively with our client base at Kredcor: waiting 90 days before engaging a professional recovery partner results in a statistically significant drop in recovery rates. Specifically, our team’s experience shows that accounts handed over within 30–45 days of default recover at nearly double the rate of those sitting in internal collections for three months or more.

Furthermore, a registered debt recovery agency brings several tools that your internal credit team simply doesn’t have: access to commercial and consumer tracing databases, negotiation expertise with distressed debtors, a formal legal escalation pathway, and — perhaps most importantly — the psychological impact of a third-party professional entering the picture. Debtors respond differently when they know a professional agency has taken over.

What to Look for in a Commercial Debt Recovery Agency

When choosing a recovery agency for manufacturing commercial defaults, look specifically for:

- Registration with the Council for Debt Collectors (CFDC) — this is a legal requirement under the Debt Collectors Act 114 of 1998.

- A No-Success, No-Fee model — so you pay nothing unless they collect.

- Specific experience in B2B and manufacturing sector recoveries — not just consumer collections.

- A dedicated account manager — not a call centre.

- Transparent monthly reporting so you always know the status of every account.

For a detailed guide on exactly when and how to make the call, read: When Should I Make Use of a Debt Recovery Agency?

Kredcor Handles Manufacturing Commercial Defaults — No Fee Unless We Collect

26+ years of B2B commercial debt recovery. Registered with the CFDC. Dedicated account managers. No admin fees. No lock-in contracts.Talk to a Recovery Specialist →

6. Stage 4 — Legal Action: The Final Step (Use It Right)

Legal action is the last resort — but it’s a real and effective one when used correctly. Moreover, the threat of litigation is often enough to prompt a settlement, which is why it’s part of your negotiation toolkit even before you file.

Understanding Your Legal Framework

As a manufacturing creditor in South Africa, several key pieces of legislation directly affect how you pursue a large-scale commercial default through the courts:

- Debt Collectors Act 114 of 1998: Governs all registered collectors. Your recovery agency must comply with this Act — and so must you when collecting through third parties.

- Prescription Act 68 of 1969: Most commercial debts prescribe after three years. This means your legal right to sue can fall away completely if you wait too long. Don’t let this happen.

- Companies Act and Insolvency Act: If your debtor has entered business rescue or liquidation, the process changes significantly — you’ll need to submit a proof of claim and understand your priority as a concurrent creditor.

- Magistrates’ Court Act / Superior Courts Act: The value of your claim determines which court you use. Claims under R400,000 typically go to the Magistrates’ Court; larger claims go to the High Court.

Summons, Default Judgment, and Warrant of Execution

Once an attorney files a summons, the debtor has a defined period to respond. If they don’t — and in many default cases they won’t — you apply for default judgment. After that, a warrant of execution allows the Sheriff of the Court to attach and sell the debtor’s assets. This process works best when your documentation is airtight from Day One — which is why Stage 1 (internal escalation and documentation) is so critical.

⚠️ Critical Warning

If your debtor enters business rescue proceedings under the Companies Act, an automatic moratorium on legal action kicks in. You cannot proceed with summons until business rescue ends — unless the court grants specific relief. Act before this happens. The moment you hear “business rescue,” escalate immediately.

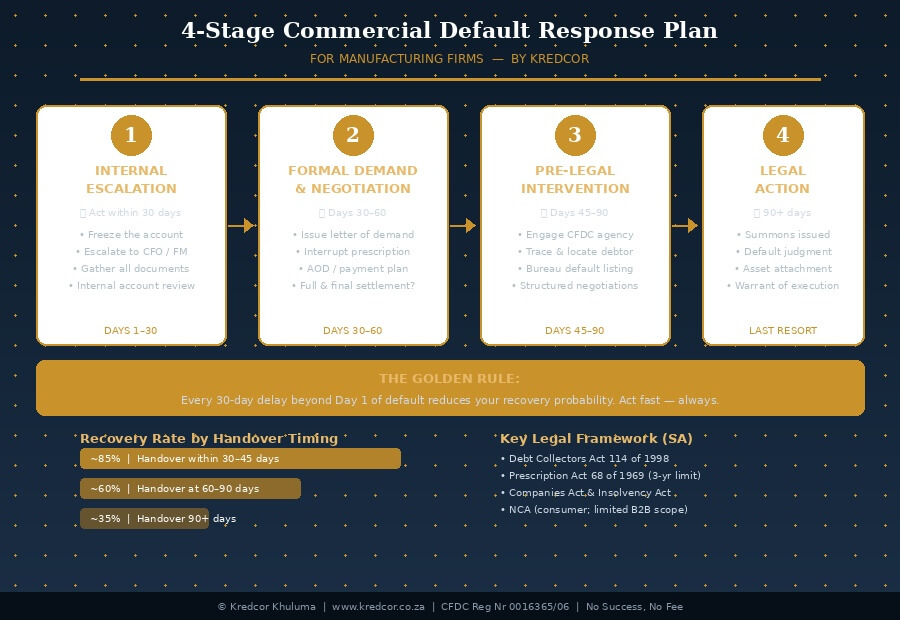

7. The 4-Stage Default Response Plan: Visual Guide

↑ Share this infographic with your credit team. Right-click to save, or download as image.

8. 5 Critical Troubleshooting Tips for Manufacturing Credit Teams

Through working with hundreds of manufacturing firms across Gauteng, KwaZulu-Natal, and the Western Cape, our team at Kredcor has identified the five most common failure points in how manufacturers handle large-scale commercial defaults — and exactly how to fix them.

| Problem | Why It Happens | Fix It Now |

|---|---|---|

| Waiting too long to act | Optimism, relationship preservation, overloaded credit team | Set a non-negotiable 30-day escalation rule. Automate it in your accounting system. |

| Continuing to supply a defaulting client | Fear of losing the client, sales pressure overriding credit control | Freeze all accounts at 30 days overdue. Sales and credit control must have a written protocol. |

| Poor documentation — can’t prove the debt | Verbal orders, missing signed delivery notes, informal agreements | Implement a mandatory documentation checklist: signed credit application, PO, delivery note, and invoice for every single transaction. |

| Letting debts prescribe (3-year rule) | Account forgotten or deprioritised; no prescription monitoring | Flag every account in your system with a prescription date. Send a formal demand before the 3-year mark at the latest. Better: hand over to a registered recovery agency well before then. |

| Using unregistered “collectors” or informal pressure tactics | Trying to save money on recovery fees; lack of awareness of legal requirements | Always verify your collection agency’s CFDC registration at cfdc.org.za. Unregistered collectors expose your business to significant legal and reputational risk. |

9. How to Prevent Large-Scale Defaults Before They Happen

Prevention is always better than cure — and in manufacturing, the best way to handle large-scale commercial defaults is to stop them before they start. Here’s how the best-run manufacturing credit departments do it.

Run a Credit Assessment Before Extending Trade Credit

Before you extend any significant credit to a new client — or substantially increase a limit for an existing one — run a commercial credit check. This means verifying the debtor’s CIPC registration, checking for existing judgments, reviewing Dun & Bradstreet or Experian commercial credit scores, and calling trade references with specific questions like “Does this company pay on time?” not just “Do they pay?”

We found that a surprisingly high number of large-scale commercial defaults in the manufacturing sector involve clients who showed clear early warning signs — increased credit requests, changed payment patterns, requests for extended terms — that a credit check would have caught.

Include Reservation of Ownership Clauses in Your Terms

A retention of title (ROT) or reservation of ownership clause in your standard terms means the goods remain your property until paid for in full. While reclaiming physical goods can be logistically complex, this clause gives you significant legal leverage — and it matters enormously if your client enters business rescue or liquidation.

Get a Signed Credit Application — Every Time

Your credit application should include: full company details and CIPC number, directors’ names and ID numbers, bank confirmation letter, trade references, your full payment terms, and crucially — your right to recover collection costs and charge interest on overdue amounts. Without a signed credit application, your legal position is significantly weaker.

Monitor Your Debtors Book Weekly, Not Monthly

Monthly aging reports are not good enough for a manufacturing business with high-value accounts. Review your accounts-receivable aging weekly. Set automated system alerts for accounts approaching 30, 45, and 60 days overdue. In our experience, businesses that monitor weekly catch emerging defaults at least two to three weeks earlier — and that early catch dramatically improves outcomes.

💡 Actionable Tip — Prevention

Review the payment behaviour of your top 10 clients every single month. Look specifically for changes: Is a reliable payer suddenly requesting extended terms? Did they skip a payment for the first time? Changes in behaviour are early warning signals of financial distress — don’t ignore them.

10. LSI Terms and Semantic Clusters for Credit Managers

If you’re building out your credit management knowledge base — or optimising your internal training materials — here are the key related terms, synonyms, and semantic clusters that sit around the topic of large-scale commercial defaults in manufacturing:

- Commercial debt recovery — the broader process of recovering overdue B2B receivables.

- B2B payment default — a business-to-business failure to pay within agreed terms.

- Trade credit risk — the risk a supplier takes when extending credit to a buyer.

- Accounts receivable delinquency — overdue receivables on your balance sheet.

- Debtor management — the full process of managing, monitoring, and collecting from debtors.

- Pre-legal collections — all recovery steps taken before formal legal proceedings.

- Acknowledgement of Debt (AOD) — a written admission of a debt, often used in manufacturing settlements.

- Business rescue — a formal process under the Companies Act that pauses creditor action.

- Default listing — recording a debtor’s non-payment on a credit bureau, which affects their credit profile.

- DSO (Days Sales Outstanding) — a key metric measuring how long it takes to collect receivables after a sale.

- Credit concentration risk — the danger of having too much receivable exposure with a single client.

- Retention of title — a contractual clause keeping goods in the seller’s ownership until payment.

Your Next Step: Partner with South Africa’s Trusted Commercial Recovery Experts

If your manufacturing business is currently dealing with a large-scale commercial default — or if you want to put the right recovery systems in place before the next one hits — our team at Kredcor is ready to help. We’ve spent over 26 years working alongside credit managers, CFOs, and SME owners across South Africa’s manufacturing, logistics, and industrial sectors, recovering commercial debts that internal teams couldn’t move. We work on a No-Success, No-Fee basis: if we don’t collect, you pay nothing. To learn more about how South Africa’s leading debt collectors in South Africa can support your business through a large-scale commercial default — and help you build a stronger credit management framework going forward — contact Kredcor today.

Meanwhile, for more expert guidance, actionable strategies, and plain-English guides to commercial debt recovery in South Africa, explore our full library of resources at https://www.kredcor.co.za/kredcor-articles/ — written specifically for credit managers, financial managers, CFOs, and SME owners who want to stay ahead of credit risk and keep their cash flow healthy. Every article is free, practical, and based on 26+ years of real commercial recovery experience.

Frequently Asked Questions (FAQ)

How do manufacturing firms handle large-scale commercial defaults?

Manufacturing firms handle large-scale commercial defaults through a structured four-stage process: (1) internal escalation — freeze the account, escalate to senior management, and gather all documentation within 30 days; (2) formal demand and negotiation — issue a letter of demand and engage in structured settlement discussions; (3) pre-legal intervention — engage a CFDC-registered debt recovery agency; and (4) legal action — summons, default judgment, and warrant of execution as a final step. The most important factor across all stages is speed: acting within 30–45 days of default roughly doubles your recovery rate compared to waiting 90 days or longer.What is a large-scale commercial default in the manufacturing sector?

A large-scale commercial default in the manufacturing sector occurs when a B2B client fails to pay one or more significant invoices — typically exceeding R50,000 — beyond the agreed payment terms, causing material damage to the supplier’s cash flow, production capacity, or financial stability. It differs from a small overdue account in both its financial impact and the complexity of the recovery process required. Large-scale defaults often involve multiple invoices, sometimes accumulated over months on a running account, and may coincide with signs of debtor financial distress such as business rescue, insolvency, or deliberate avoidance.When should a manufacturing firm use a debt recovery agency for a commercial default?

A manufacturing firm should engage a registered CFDC-approved debt recovery agency when an account is 60–90 days overdue, internal collection efforts have failed to produce a payment or a written payment arrangement, and the debtor is either unresponsive, making broken promises, or showing signs of financial distress. The data is clear: accounts handed to professional recovery agents within 30–45 days of default recover at nearly double the rate of accounts left in internal collections for 90+ days. Do not wait.What legal framework governs commercial defaults in South Africa’s manufacturing sector?

Commercial defaults in South Africa are governed by several key pieces of legislation. The Debt Collectors Act 114 of 1998 regulates all registered debt collectors — any agency you appoint must hold CFDC registration. The Prescription Act 68 of 1969 sets a 3-year limitation period on most commercial debts — act before this expires or your legal right to sue may fall away. The Companies Act and Insolvency Act govern what happens when your debtor enters business rescue or liquidation. The National Credit Act applies primarily to consumer credit, though it has some implications for B2B transactions involving sole proprietors. Understanding these laws — even at a basic level — is essential for every credit manager and CFO in manufacturing.

About the Author

Kredcor is South Africa’s specialist commercial debt recovery partnership, operating since 1999 across Gauteng, Western Cape, KwaZulu-Natal, Africa, and internationally. Registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06). With a 100% clean regulatory record over 26+ years and a No-Success, No-Fee model, Kredcor works exclusively on B2B commercial debt recovery — never consumer debt.

📞 010 500 4640 | 🌐 www.kredcor.co.za

Authoritative External Resources

- Council for Debt Collectors (CFDC) — Verify any debt collector’s registration in South Africa.

- Companies and Intellectual Property Commission (CIPC) — Verify company registrations and director details.

- South African Revenue Service (SARS) — Tax compliance information relevant to B2B creditors.

- Department of Justice & Constitutional Development — Court processes and legal framework for debt recovery.

- Association of Debt Recovery Agents (ADRA) — Industry body for ethical commercial recovery in South Africa.

© 2026 Kredcor Khuluma — South Africa’s Commercial Debt Recovery Partners | CFDC Reg Nr 0016365/06

No Success, No Fee | 26+ Years | Gauteng · Western Cape · KwaZulu-Natal · Africa · Global