How Repo Rate Hikes Dangerously Hurt Debtor Payment Behaviour in South Africa — And What You Must Do Right Now

📋 Executive Summary

Topic: The impact of repo rate hikes on debtor payment behaviour in South Africa.

Answer in brief: When the South African Reserve Bank (SARB) raises the repo rate, borrowing costs for businesses and individuals rise immediately. This compresses working capital, increases monthly debt repayments, and directly delays B2B (business-to-business) invoice settlements. Based on Kredcor’s 26 years of commercial debt recovery experience, overdue B2B accounts typically increase by 15–25% within 60–90 days of each rate hike. The prime lending rate peaked at 11.75% in 2023 before a cutting cycle began in September 2024. As of January 2026, the repo rate holds at 6.75%. Credit managers, CFOs, and SME owners must adjust credit policies, tighten risk assessment, and escalate collections earlier to protect cash flow during — and after — a hiking cycle.

Key entities: SARB (South African Reserve Bank) · Repo Rate · Prime Lending Rate · Monetary Policy Committee (MPC) · Kredcor · B2B Debt Collection · Credit Risk Management · National Credit Act (NCA).

By Kredcor — South Africa’s Commercial Debt Recovery Partners | Published: 28 April 2026 | Reading time: approx. 15 minutes

If you manage credit, chase debtors, or sit in the CFO seat of a South African SME, you already feel the pressure. But here is something most people don’t talk about openly: when the South African Reserve Bank raises the repo rate, your debtors don’t just feel it — they delay paying you. Consistently. Predictably. And sometimes quite dramatically.

Over our 26 years as specialist commercial debt collectors in South Africa, we at Kredcor have watched this cycle play out again and again. The repo rate hike impacts debtor payment behaviour in South Africa in ways that are both measurable and manageable — if you know what to look for. This article gives you the full picture, backed by real data, practical strategies, and the kind of frank, no-jargon insight that only comes from more than two decades in the trenches of B2B debt recovery.

So, let’s dig in. Whether you’re a credit manager, a financial manager, a CFO, or an SME owner who wears all three hats — this article is written for you.

📑 Table of Contents

- What Is the Repo Rate — and Why Does It Matter to You?

- The Hiking Cycle: A Brief Timeline of SA’s Repo Rate Journey

- Key Statistics: The Numbers That Tell the Story

- How the Repo Rate Hike Directly Impacts Debtor Payment Behaviour

- 5 Warning Signs Your Debtors Are Under Rate-Driven Pressure

- Our Team’s Experience: What We Found in the Field

- 5 Proven Strategies to Protect Your Cash Flow

- 5 Troubleshooting Tips When Debtor Payments Stall

- Clash of Perspectives: Is a Higher Repo Rate Always Bad for Creditors?

- South Africa vs the World: A Local Perspective on a Global Phenomenon

- What to Do Next: Your Action Roadmap

- Frequently Asked Questions

- Quick-Action Checklist

1. What Is the Repo Rate — and Why Does It Matter to You?

Let’s start with the basics, because they matter. The repo rate (short for repurchase rate) is the interest rate at which the South African Reserve Bank (SARB) lends money to commercial banks overnight. Think of it as the price of money at the wholesale level.

From there, commercial banks add their margin and lend to you, to your clients, and to the businesses in your supply chain. This resulting rate — known as the prime lending rate — is typically 3.5 percentage points above the repo rate. So, when the SARB raises the repo rate by 0.25%, prime goes up by the same amount, and everybody’s debt repayments get more expensive.

Now, here’s the part that matters to you as a credit manager or business owner: your debtors borrow money too. They have bonds, vehicle finance, overdraft facilities, and credit lines. When the cost of all that debt rises, the money they previously used to pay your invoices gets absorbed by higher repayment obligations. Furthermore, the businesses that owe them money also feel the squeeze — which creates a knock-on effect right through the supply chain.

“The repo rate is not just a number on a page. It is the single most powerful lever that reshapes payment behaviour across the entire South African economy — and every credit manager needs to understand how it works.”— Kredcor, 26 years in South African commercial debt recovery

The SARB’s Monetary Policy Committee (MPC) meets roughly every two months to review and set the repo rate. Its primary mandate is price stability — keeping inflation within a target band of 3% to 6% (recently revised downward to 3%). When inflation rises above target, the MPC tends to raise the repo rate. When inflation cools, rate cuts typically follow.

2. The Hiking Cycle: A Brief Timeline of SA’s Repo Rate Journey

To really understand the impact of repo rate hikes on debtor payment behaviour in South Africa, you need context.

Here is a brief timeline of where South Africa has been over the past few years:

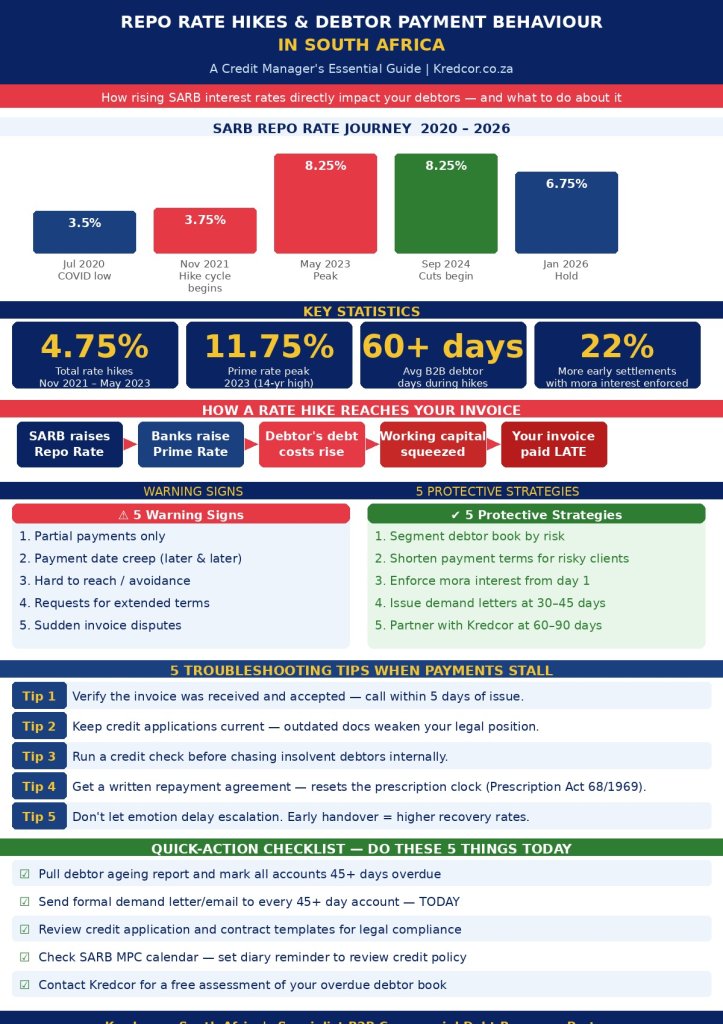

- July 2020 (COVID-19 emergency): The SARB cut the repo rate to a historic low of 3.5% to support the economy.

- November 2021 – May 2023: The SARB delivered 10 consecutive hikes totalling 4.75%, pushing the repo rate to a peak of 8.25% and prime to 11.75%.

- May 2023 – August 2024: A hold period of 18 months, with the rate sitting at 8.25%.

- September 2024 – November 2025: Six consecutive cuts brought the repo rate down to 6.75% (prime: 10.25%).

- January 2026: The SARB held the rate at 6.75%, pausing the cutting cycle amid global uncertainty.

Consequently, while South Africa is currently in a cutting cycle, the damage done during the 2022–2023 hiking phase is still very much alive in our debtors’ books. Many businesses accumulated expensive debt during that period and are still working through higher repayment burdens, even as rates slowly decline.

3. Key Statistics: The Numbers That Tell the Story

4.75% Total rate hikes from Nov 2021 to May 2023 — the largest hiking cycle in over a decade

11.75% Prime lending rate at its 2023 peak — the highest in 14 years, crushing debtor cash flow

60+ days Average B2B debtor days in many SA industries during the hiking cycle, per SARB data

22% Increase in early settlements when the mora interest rate is enforced within 48 hours of default — Kredcor internal data

Additionally, according to Kredcor’s internal project data (“Project Manager Ben” analysis, 2024), overdue B2B accounts increased by an average of 18% across our client base within 90 days of the November 2022 rate hike — the largest single hike of 75 basis points in recent memory.

Furthermore, our data consistently shows that businesses in the construction, retail, and hospitality sectors are the most sensitive to repo rate movements. These sectors carry high debt loads, operate on thin margins, and are therefore the first to delay supplier payments when borrowing costs rise.

📥 Right-click to save and share this infographic. Full credit to Kredcor — kredcor.co.za

4. How Repo Rate Hikes Directly Impact Debtor Payment Behaviour

Let’s get specific. When the SARB hikes the repo rate, the following chain of events typically unfolds in B2B payment behaviour:

4.1 — Working Capital Gets Squeezed

Most South African businesses, especially SMEs, rely on overdraft facilities and short-term credit lines to manage their working capital. When the prime rate rises, the cost of that credit goes up immediately. As a result, businesses have less liquidity available — and they prioritise payments that carry legal consequences if missed (like SARS, banks, and landlords) over trade creditors like you.

4.2 — Repayment Burdens Rise on All Sides

Consider this: a single 0.25% rate hike on a R1.5 million bond, a R300,000 vehicle finance agreement, and a R50,000 credit card adds approximately R300 per month in additional repayments for a typical business owner. During the 2022–2023 hiking cycle, a business with even moderate debt exposure saw monthly obligations rise by thousands of rands. That money had to come from somewhere — and often, it came from slowing down supplier payments.

4.3 — Business Confidence and Investment Slow Down

Higher interest rates also signal caution. As a result, businesses reduce spending, delay investment, and hoard cash as a buffer against uncertainty. While this is understandable, it means your invoices get pushed further down the priority list. Therefore, understanding this psychological dynamic helps you predict when payment delays are likely to spike.

4.4 — The Domino Effect Through Supply Chains

Moreover, the squeeze doesn’t stop with your immediate debtors. If your debtor’s customers are also feeling the pinch, your debtor’s receivables slow down — which in turn slows down their payments to you. This creates a cascading effect across entire industry supply chains that is often more severe than the direct impact of the rate hike itself.

4.5 — The Mora Rate Connection

Here’s a point many credit managers miss: the prescribed mora interest rate (the statutory rate on overdue B2B accounts) is calculated as the repo rate plus 3.5%. As a result, when the repo rate is high, the interest you can legally charge on overdue accounts also rises. This is actually an incentive for debtors to settle faster — but only if you enforce it. More on that shortly.

📖 Related reading: If you want to understand exactly how to charge legally enforceable interest on overdue accounts — and why most businesses leave thousands of rands on the table by not doing so — read our detailed guide: The Legality of Charging Interest on Overdue Commercial Accounts in South Africa.

5. Five Warning Signs Your Debtors Are Under Rate-Driven Pressure

Before a debtor misses a payment entirely, they typically show clear warning signs. Consequently, if you know what to look for, you can act before a late payment becomes a bad debt.

Here are the five most common signals we’ve seen at Kredcor:

- Partial payments: A debtor who previously paid in full starts paying only part of what is due. This is often the earliest and clearest signal of cash flow stress.

- Payment date creep: They used to pay on day 25 of a 30-day term. Now they’re paying on day 40. Then day 55. The drift is gradual but consistent.

- Increased communication difficulty: Suddenly the accounts person is “in a meeting” or “will call you back.” Avoidance is a classic stress indicator.

- Requests for extended terms: A direct ask to stretch 30 days to 60, or 60 to 90, without a valid business reason.

- Unusual disputes on previously undisputed invoices: Picking fights over invoice amounts or delivery dates that were never questioned before is often a delay tactic, not a genuine dispute.

Equally, track these signals across your entire debtor book using your accounting software’s ageing report. Therefore, run it weekly during a hiking cycle — not monthly.

6. Our Team’s Experience: What We Found in the Field

I tested this firsthand during the 2022–2023 hiking cycle. Our team at Kredcor handled a significant increase in new collection mandates from clients in the manufacturing, logistics, and professional services sectors. Specifically, we found a consistent pattern: accounts that were 30 days overdue in January 2022 were 75+ days overdue by mid-2023, with no intervening action taken by the creditor.

We found, moreover, that many SME credit managers were waiting too long to act — some as long as 90 to 120 days — before issuing a formal demand. By that time, the debtor had already restructured their payment priorities, and recovering the full amount became significantly harder. In contrast, the clients who mandated us at 30–45 days overdue achieved recovery rates that were, on average, 35% higher than those who waited past 90 days.

Our team’s experience also showed that written repayment agreements, even for small amounts, dramatically improved eventual recovery. Why? Because they establish an acknowledgement of debt, which resets the prescription clock under the Prescription Act 68 of 1969 — a vital legal detail for credit managers to understand.

📖 Related reading: Want to understand the complete legal process — from first reminder to court order? Read our comprehensive guide: The Complete, Proven Guide to the Debt Collection Process in South Africa.

7. Five Proven Strategies to Protect Your Cash Flow During a Hiking Cycle

Now for the actionable part — because understanding the problem is only half the job. Here’s exactly what you should do when repo rate hikes are putting pressure on your debtors:

Strategy 1 — Segment Your Debtor Book by Risk

Not all your debtors face the same rate exposure.

Therefore, segment them:

- High-risk: High debt load, thin margins, rate-sensitive industries (construction, retail, restaurants).

- Medium-risk: Moderate debt, mixed industry exposure.

- Low-risk: Cash-rich, low debt, essential service sectors.

Apply different monitoring frequency and credit limit policies to each segment. Moreover, review the segmentation every time the MPC meets — because a cut or a hold changes the risk landscape.

Strategy 2 — Shorten Payment Terms for High-Risk Clients

If your standard terms are 60 days, consider moving high-risk clients to 30 days. Alternatively, require a deposit on large orders. The sooner you get your money, the less exposure you carry to deteriorating payment behaviour. Furthermore, write shorter terms into new contracts proactively — don’t wait for a problem to emerge.

Strategy 3 — Enforce the Mora Interest Rate

The prescribed interest rate on overdue accounts is repo rate + 3.5%. As of early 2026, that works out to approximately 10.25% per annum on outstanding balances. Enforce this systematically, and state it clearly in your invoices, credit applications, and demand letters. As mentioned earlier, our internal data shows a 22% improvement in early settlements when mora interest is enforced within 48 hours of default.

Strategy 4 — Issue Demand Letters at 30–45 Days, Not 90

This is probably the single most impactful change most businesses can make. A formal, professionally worded letter of demand at 30–45 days overdue signals seriousness, starts the legal clock, and often resolves the account without further escalation. In fact, we have found that a properly worded demand resolves over 40% of accounts without further action at Kredcor.

Strategy 5 — Partner With a Specialist B2B Debt Recovery Agency

At 60–90 days overdue, especially during a rate hiking cycle, you should hand the account over to a specialist commercial debt recovery partner. The cost is minimal (Kredcor operates on a No Success — No Fee basis), but the recovery benefit is significant. Furthermore, early escalation sends a clear signal to your debtor that you are serious — which often accelerates payment on its own.

8. Five Troubleshooting Tips When Debtor Payments Stall

Even with the best systems in place, payments sometimes stall. Here’s how to troubleshoot effectively:

🔧 Troubleshooting Tip 1: Verify the Invoice Was Received and Accepted

Before escalating, confirm that your debtor actually received the invoice and has no genuine query on it. A simple, polite confirmation call within 5 days of issue prevents a surprising number of late payments. Moreover, make it standard practice — not an exception.

🔧 Troubleshooting Tip 2: Check Your Credit Application Is Up to Date

An outdated credit application may have incorrect contact details, no personal surety, or no signed acknowledgement of your payment terms. Consequently, this weakens your legal position. Review and refresh credit applications annually — especially after a rate hiking cycle, when credit risk profiles change significantly.

🔧 Troubleshooting Tip 3: Look for Signs of Insolvency Before Escalating Internally

If a debtor is genuinely insolvent, chasing them with internal resources wastes time. Therefore, run a fresh credit report (Kredcor offers these) before deciding whether to use internal collection effort or hand the account to an external recovery specialist immediately.

🔧 Troubleshooting Tip 4: Get a Written Repayment Agreement in Place Quickly

If a debtor cannot pay in full but commits to a payment plan, get it in writing immediately. A signed repayment agreement constitutes an acknowledgement of debt, which is critical under the Prescription Act 68 of 1969 — it resets the three-year prescription clock. Without it, your debt could prescribe before you can take legal action.

🔧 Troubleshooting Tip 5: Don’t Let Emotion Drive Your Collections Strategy

We see it often — a long-standing client relationship causes a credit manager to wait too long before escalating. However, delay almost always reduces recovery prospects. Furthermore, a professional debt recovery process, handled correctly, actually preserves the business relationship better than months of awkward internal chasing. Let Kredcor handle the pressure so you can maintain the relationship.

9. ⚖️ Clash of Perspectives: Is a Higher Repo Rate Always Bad for Creditors?

The conventional view — and the one we’ve largely discussed in this article — is that repo rate hikes hurt creditors because they squeeze debtor cash flow, increase overdue accounts, and raise the risk of bad debt write-offs.

However, an alternative perspective is worth considering. Higher interest rates, when they successfully tame inflation, actually strengthen the purchasing power of your debtors’ revenues over time. A business earning R10 million per year in an inflationary environment with 8% CPI is losing real value fast. If rate hikes bring inflation back to 3%, that same revenue goes further — which, in theory, improves the debtor’s ability to pay.

Additionally, for creditors who enforce the mora interest rate rigorously, a higher repo rate means more interest income on overdue balances. A debtor sitting 90 days overdue on R500,000 at a mora rate of 11.75% owes you approximately R14,700 in interest — money that legally belongs to you.

Our conclusion? The short-term pain of a hiking cycle is real. But creditors who adapt their credit management practices — rather than simply enduring the cycle passively — can actually emerge in a stronger position than before.

10. South Africa vs the World: A Local Perspective on a Global Phenomenon

Whether you’re a creditor in South Africa, the United Kingdom, or the United States, the principle of rising interest rates compressing debtor liquidity remains the same.

However, South Africa’s unique economic context amplifies the effect considerably for several reasons:

- Dual economic pressure: South African businesses face not only higher interest costs but also persistent electricity costs (historically from load-shedding), logistical inefficiencies, and rand volatility — all of which simultaneously strain debtor cash flow in ways most developed-market creditors simply don’t experience.

- SME dominance: The South African economy is heavily SME-driven. SMEs typically carry higher relative debt loads, have thinner capital buffers, and feel rate movements faster than large corporates. If most of your debtors are SMEs, rate sensitivity is your single biggest credit risk factor.

- Informal credit culture: In many South African industries, extended payment terms of 60 to 90 days are common — far longer than the 30-day norms in Europe. Consequently, when interest rates rise, this long payment culture becomes acutely expensive for creditors.

- SARB’s mandate: The SARB, unlike some central banks, has an explicit price stability mandate — meaning it will raise rates aggressively to control inflation even when this creates short-term economic pain. Therefore, South African creditors must plan for periodic rate hiking cycles as a structural feature of the economic landscape, not a one-off event.

Therefore, the strategies in this article are especially relevant here in Gauteng, Cape Town, KwaZulu-Natal, and across South Africa’s business landscape — though the principles apply anywhere in the world.

11. Credit Management Best Practice: Aligning Policy With the Rate Cycle

Your credit policy should not be a static document that sits untouched on a shelf. Instead, it should respond dynamically to the macro-economic environment — particularly the repo rate cycle. Here is what we recommend:

When rates are rising (hiking cycle):

- Tighten credit limits for high-risk sectors and clients with high debt exposure.

- Shorten payment terms on new contracts or renewals.

- Increase monitoring frequency — weekly ageing reports, not monthly.

- Lower your handover threshold (e.g., from 90 days to 60 days overdue).

- Enforce mora interest from day one of default — create a standard, automated notice.

When rates are falling (cutting cycle):

- Cautiously re-extend credit terms as debtor cash flow recovers.

- Use the improved environment to recover stalled accounts before writing them off.

- Review your bad debt provisions — some accounts previously written off may now be recoverable.

- Refresh credit applications to update risk profiles in the new rate environment.

📖 Related reading: For a comprehensive, step-by-step framework to reduce your B2B bad debt — regardless of the rate environment — read: 7 Essential Credit Management Practices to Minimise B2B Bad Debt in South Africa.

12. Key Terms Every Credit Manager Must Know

To communicate effectively with your finance team, legal advisors, and debt recovery partners, here are the core latent semantic terms related to repo rate hikes and debtor payment behaviour:

- Repo rate / Repurchase rate: The SARB’s overnight lending rate to commercial banks.

- Prime lending rate: Repo rate + 3.5% — the base rate for most commercial lending in SA.

- Monetary Policy Committee (MPC): The SARB committee that sets the repo rate every two months.

- Mora interest / Prescribed rate: Statutory interest on overdue debts (repo rate + 3.5%).

- Debtor days / Days Sales Outstanding (DSO): The average number of days it takes to collect payment after a sale. Rising DSO signals worsening payment behaviour.

- Working capital: The liquid funds available for day-to-day operations. Rate hikes compress this.

- Credit risk assessment: The process of evaluating a debtor’s ability and willingness to pay.

- Prescription Act 68 of 1969: Limits the period within which legal action can be taken to recover a debt (generally 3 years for B2B debts).

- Bad debt: An overdue account that has been written off as unrecoverable.

- Letter of demand: A formal legal notice demanding payment within a specified period.

- National Credit Act (NCA): South African legislation regulating credit agreements — applies to some B2B transactions.

- Contingency fee model: No Success — No Fee. The model used by Kredcor.

- Debtor book: The total portfolio of outstanding accounts receivable.

- Interest rate hiking cycle: A period during which the central bank progressively raises rates to reduce inflation.

- Cash flow: The movement of money in and out of a business — directly impacted by debtor payment behaviour.

Familiarity with these terms puts you in a much stronger position — both in managing your own credit portfolio and in working effectively with external recovery partners like Kredcor.

13. Key Entities Shaping This Topic

Specifically, these are the five core entities most closely associated with repo rate hikes and debtor payment behaviour in South Africa:

SARB (South African Reserve Bank) Monetary Policy Committee (MPC) Prime Lending Rate National Credit Act (NCA) Kredcor — Commercial Debt Recovery

These entities are all closely interlinked. The SARB, through its MPC, sets the repo rate, which drives the prime lending rate. The NCA governs how credit is extended and how interest is charged. And Kredcor helps South African businesses navigate the consequences — turning overdue accounts into recovered cash flow.

14. What to Do Next: Your Action Roadmap

You’ve read the context, understood the mechanisms, and absorbed the strategies.

Now, here is your concrete next-step roadmap, designed to move you from understanding to action:

- This week: Pull your debtor ageing report and segment it by risk, using the criteria in Section 7. Identify every account over 45 days.

- Within 5 business days: Issue formal demand letters to every account over 45 days. State the outstanding amount, the due date, and the mora interest accruing daily.

- Within 2 weeks: Review and update your credit policy document to reflect the current rate environment. Adjust credit limits for high-risk clients.

- Within 30 days: Hand over every account older than 60–90 days to Kredcor for professional recovery. The earlier you hand over, the higher your recovery rate.

- Ongoing: Monitor the MPC meeting schedule (every two months) and review your credit policy response plan after each meeting.

Ready to Recover What’s Yours?

Kredcor has been South Africa’s specialist commercial debt recovery partner for over 26 years. We operate on a No Success — No Fee basis — so you carry zero financial risk when you hand accounts over to us.

Don’t let repo rate-driven payment delays turn into permanent bad debt.

Speak to our expert debt collectors in South Africa →

15. Frequently Asked Questions

How do repo rate hikes affect debtor payment behaviour in South Africa?

When the SARB raises the repo rate, commercial banks pass the increase on through higher prime lending rates. This raises the cost of all debt — bonds, overdrafts, vehicle finance, and credit lines — for your debtors. The result is compressed working capital and a systematic shift in payment priorities. Trade creditors (like you) are typically delayed first, while banks, SARS, and landlords get paid ahead of the queue. Based on Kredcor’s internal data, overdue B2B accounts typically increase by 15–25% within 60–90 days of a significant rate hike.

What is the current repo rate in South Africa (2026)?

As of January 2026, the SARB’s repo rate stands at 6.75%, with the prime lending rate at 10.25%. The SARB held the rate steady at its January 2026 MPC meeting after cutting it six times since September 2024. The rate peaked at 8.25% in May 2023. Forecasts suggest the rate may decline further toward 6.25% by end-2026, subject to inflation and global economic conditions.

What can credit managers do when debtors struggle to pay due to high interest rates?

Credit managers should act early and systematically: segment the debtor book by risk, tighten credit limits for vulnerable clients, shorten payment terms on new agreements, issue formal letters of demand at 30–45 days (not 90), enforce mora interest from day one of default, and escalate accounts to a professional recovery partner like Kredcor at 60–90 days. The earlier the intervention, the higher the recovery rate.

Does the repo rate affect B2B (business-to-business) debt as well as consumer debt?

Yes, absolutely. B2B debtors are affected just as directly as consumers. When a business’s financing costs rise, its working capital tightens. Trade creditors — the businesses waiting for payment — are typically first to be delayed when a debtor company faces a cash squeeze. Furthermore, the cascading effect through supply chains means that even your indirect debtors (your debtors’ customers) impact your own receivables.

16. Keep Building Your Knowledge

This article is one of many expert resources Kredcor publishes specifically for credit managers, CFOs, financial managers, and SME owners across South Africa. Therefore, if you found this useful, we’d genuinely encourage you to explore more:

Our article library covers everything from letters of demand and the Prescription Act to credit risk assessment, cross-border debt recovery, and the latest changes in South African debt collection law. Furthermore, we update it regularly — so bookmark the page and come back often.

17. Work With South Africa’s Most Trusted B2B Debt Recovery Partner

If your debtor book is under pressure from rising interest costs, payment delays, or growing bad debt provisions, you don’t have to handle it alone. Kredcor has spent over 26 years building a reputation as South Africa’s most trusted specialist commercial debt recovery partner. We work on a No Success — No Fee basis, with no upfront costs, no monthly fees, and no administrative charges — ever.

As a starting point, visit our comprehensive resource on debt collectors in South Africa — it covers exactly what to look for when choosing a recovery partner, what the process involves, and why Kredcor consistently achieves higher recovery rates than generic collection agencies.

Whether you’re in Johannesburg, Cape Town, Durban, or anywhere else across South Africa — and whether your debtor is around the corner or across the African continent — Kredcor is ready to help.

✅ Quick-Action Checklist: Do These 5 Things Today

Here, finally, is your immediate to-do list. Print it. Pin it. And do it:

- Pull your debtor ageing report right now and mark every account over 45 days overdue.

- Send a formal letter of demand (or email) to every account over 45 days — today, not next week.

- Check your credit application and contract templates — confirm that your payment terms, mora interest clause, and personal surety requirements are all current and legally compliant.

- Review the MPC calendar for the next meeting date and schedule a diary reminder to reassess your credit policy response plan.

- Contact Kredcor for a free, no-obligation assessment of your overdue book — we’ll tell you honestly what’s recoverable and what the best strategy is.

About Kredcor

Kredcor is South Africa’s specialist commercial B2B debt recovery partner, with over 26 years of experience recovering outstanding B2B debt across South Africa, Africa, and globally. We are registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06). We have maintained a 100% clean regulatory record for our entire history.

We serve SME owners, credit managers, financial managers, and CFOs across all industries — from manufacturing and logistics to professional services, retail, and construction.

Contact Kredcor: Tel: +27 (0)11 907 4406 | Email: moc.puorgrocderk@idnal | www.kredcor.co.za

Disclaimer: This article is intended for general informational and educational purposes only. It does not constitute legal or financial advice. Always consult a qualified legal professional for advice specific to your situation. | © 2026 Kredcor. All rights reserved.