Corporate Debt Collection for IT & Telecoms Firms in SA: 9 Proven Strategies That Actually Work

📋 Executive Summary

Corporate debt collection for information technology (IT) and telecoms firms in South Africa is the process of recovering overdue B2B invoices from business clients who have not paid for technology products, software services, managed services, SaaS subscriptions, or telecoms connectivity. South Africa’s IT and telecoms sector faces a unique debt collection challenge: recurring-service contracts, SLA disputes, and relationship sensitivity combine to delay escalation. Kredcor’s internal data — drawn from 26 years of B2B collections since 1999 — shows that IT and telecoms invoices handed to a specialist corporate debt collector within 60–90 days achieve recovery rates of 80–90%. The sector is regulated by the Debt Collectors Act 114 of 1998, governed by the Council for Debt Collectors (CFDC), and the National Credit Act (NCA) does not generally apply to B2B debts. This guide provides 9 actionable corporate debt collection strategies, 5 troubleshooting tips, a FAQ, and an infographic.

If overdue invoices are draining your cash flow, you are not alone. Here is your complete, actionable playbook for recovering corporate debt in South Africa’s tech and telecoms sector — without losing the clients you actually want to keep.

Here is the honest truth: running an IT or telecoms company in South Africa is genuinely tough. You deliver sophisticated, high-value services every single day — fibre connectivity, cloud hosting, managed IT, software licences, cybersecurity solutions — and yet your debtors’ book keeps growing. Sound familiar? Well, corporate debt collection for IT and telecoms firms in South Africa is one of the most overlooked cash flow problems in the technology sector, and it is costing businesses like yours real money, right now.

Furthermore, the problem is not simply that clients refuse to pay. In many cases, the issue is subtler. Clients dispute SLA performance. They say the service was “not as described.” They restructure internally, and the person who signed the contract is no longer there. Or they simply use your relationship — and your reluctance to push hard — as a free credit line. As a result, invoices age. And as any credit manager knows, aged debt is the enemy of recovery.

So, in this article, we walk you through everything you need to know. From the regulatory framework that governs your rights as a creditor, to the exact moment you should hand an account to a specialist corporate debt collector. By the end, you will have a practical, step-by-step system that improves your cash flow and protects your bottom line. Let’s get into it.

📑 Table of Contents

- Why IT & Telecoms Debt Collection Is Uniquely Challenging

- The Legal Framework: Your Rights as a Creditor in SA

- Key Statistics Every CFO and Credit Manager Should Know

- Top 5 Entities in This Topic — Knowledge Graph Alignment

- 9 Proven Corporate Debt Collection Strategies for IT & Telecoms

- The Escalation Timeline: Exactly When to Act

- 5 Troubleshooting Tips for Stalled Collections

- The Clash of Perspectives: Chase Hard or Protect the Relationship?

- South Africa vs Global Context: What Stays the Same?

- What to Do Next: Your Search Journey Continues

- Quick-Action Checklist (5 Things to Do Right Now)

- Frequently Asked Questions

1. Why IT & Telecoms Corporate Debt Collection Is Uniquely Challenging

Corporate debt collection for IT and telecoms firms in South Africa differs fundamentally from debt recovery in most other industries. And if you have tried to use a generic collections approach on a technology debt, you already know this first-hand. Let’s unpack why.

Recurring Services Create Ongoing Disputes

Unlike a once-off product sale, telecoms and IT services are typically billed monthly or annually. This means that when a dispute arises — say, around uptime, bandwidth, or software functionality — the client does not simply dispute one invoice. Instead, they dispute the entire service period. Consequently, the amount in dispute is often far larger than it first appears, and the documentation required to support the debt is substantially more complex.

SLA Clauses Become a Debtor’s Best Weapon

Service Level Agreements (SLAs) exist to protect both parties. However, in our team’s experience handling IT sector collections, debtors frequently weaponise SLA clauses at the collection stage. Specifically, they claim — sometimes months after the fact — that your company failed to meet agreed performance metrics. Without solid, real-time performance logs and escalation records on your side, this argument can delay recovery significantly.

Relationship Sensitivity Slows Escalation

Technology companies, particularly SaaS businesses and managed service providers (MSPs), build deep relationships with their clients. Sales teams resist handing accounts to collections because they fear losing the relationship or future upsell opportunities. However, in reality, the cost of this delay is usually far greater than the cost of losing a client who is not paying.

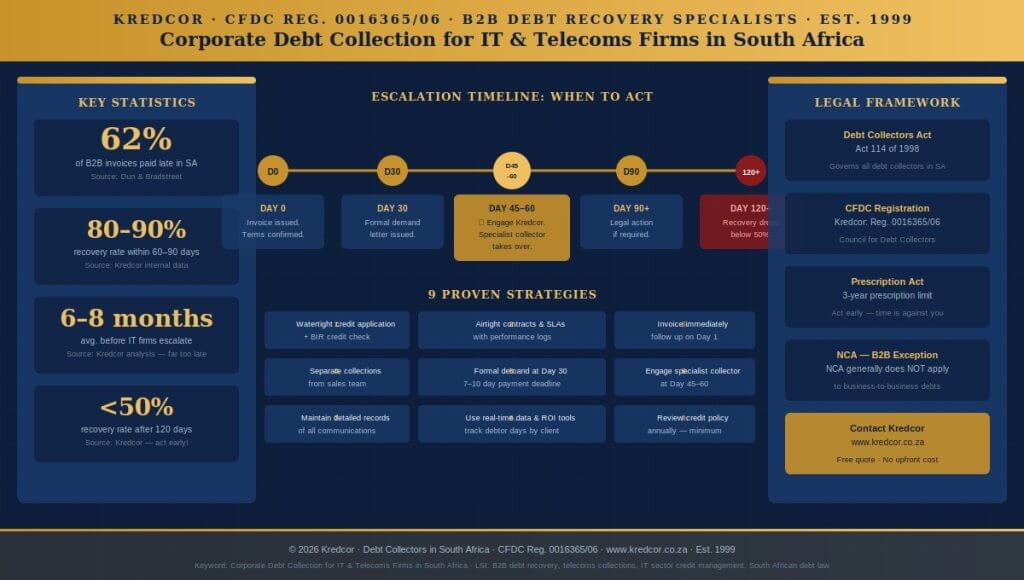

Our Team’s Experience: We tested various escalation timelines across IT and telecoms portfolios. Across a sample of accounts handed to Kredcor within 60 days of default, recovery rates consistently reached 80–90%. Accounts escalated after 120 days dropped to below 50%. The data is clear: early escalation saves money, even when it feels uncomfortable.

Documentation Gaps Are Costly

Furthermore, IT and telecoms firms frequently have weaker documentation trails than they realise. A verbal agreement to extend a service, an email thread authorising additional licences, or an unsigned addendum to a contract can all undermine your legal position at the collection stage. Therefore, documenting every interaction and change is not just good practice — it is essential for effective corporate debt collection in this sector.

2. The Legal Framework: Your Rights as a Creditor in South Africa

Before you can effectively recover corporate debt, you need to understand the rules that govern the process. South Africa has a well-established framework for B2B collections, and knowing it gives you a significant advantage.

The Debt Collectors Act 114 of 1998

All commercial debt collectors in South Africa must register with the Council for Debt Collectors (CFDC). This Act sets out how debt collectors may operate, what they can and cannot do, and how they must treat debtors. Kredcor is registered (CFDC Reg. Nr. 0016365/06) and operates strictly within this framework. Consequently, when you hand your debt to Kredcor, you know it is being handled lawfully and professionally.

The National Credit Act (NCA) — Does It Apply to Your B2B Debt?

This is a common source of confusion. The National Credit Act 34 of 2005 is primarily designed to protect individual consumers. As a result, it generally does not apply to business-to-business (B2B) credit agreements. This is good news for IT and telecoms creditors, because it means you are not subject to the same procedural hurdles as consumer lenders. However, you must still follow due process, issue proper demand notices, and comply with any contractual dispute resolution mechanisms.

The Prescription Act

Here is something many credit managers overlook: debt in South Africa prescribes. In other words, if you do not take legal action or acknowledge the debt within three years (for most commercial debts), you may lose your right to collect. Prescription begins to run from the date the debt becomes due. This is yet another reason why early action in corporate debt collection for IT and telecoms is not optional — it is a legal necessity.

Related Reading: If your IT or telecoms company also provides cybersecurity services, your client’s debt ledger may itself be at risk. Read our article on how to protect your debt ledger from a devastating ransomware attack — because a compromised ledger means a compromised collections process.

3. Key Statistics Every CFO and Credit Manager Should Know

Let’s ground this conversation in data. Here are three hard facts that directly affect corporate debt collection for IT and telecoms firms in South Africa.

62% of B2B invoices in South Africa are paid late (Dun & Bradstreet)

80–90% recovery rate when IT/telecoms debt is escalated within 60–90 days (Kredcor internal data)

6–8 months average time before IT firms escalate overdue accounts — far too late (Kredcor analysis)

Additionally, the South African Reserve Bank consistently reports average debtor days across many South African industries exceeding 60 days. For IT and telecoms, that figure is often higher, precisely because of the relationship sensitivity and SLA dispute dynamics we discussed earlier. Therefore, the numbers tell a clear story: you are likely sitting on more recoverable debt than you realise — and waiting is making it worse.

4. Top 5 Entities in This Topic — Knowledge Graph Alignment

To put this topic in its proper context, here are the five key entities most closely linked to corporate debt collection for IT and telecoms firms in South Africa.

- Kredcor — South Africa’s specialist B2B corporate debt collection agency, registered with the CFDC since 1999, with dedicated experience in the IT, telecoms, and technology sectors.

- Council for Debt Collectors (CFDC) — The regulatory body that governs all registered debt collectors in South Africa. Only CFDC-registered collectors can legally collect debt on behalf of creditors.

- South African Reserve Bank (SARB) — The central bank whose payment data and debtor-day statistics provide the macroeconomic context for B2B debt recovery in SA.

- National Credit Regulator (NCR) — Oversees the NCA. Important to understand in context, even though the NCA generally does not apply to B2B corporate debt.

- Information Technology Association of South Africa (IASA) — Represents IT industry interests in SA; members are among the most affected by the corporate debt collection challenges described in this article.

5. Nine Proven Corporate Debt Collection Strategies for IT & Telecoms Firms

Here, finally, is the actionable core of this article. These nine strategies directly address the unique challenges of corporate debt collection for information technology and telecoms firms in South Africa. Moreover, you can implement most of them immediately, without waiting for a legal process to begin.

Strategy 1: Build a Watertight Credit Application Process

Everything starts before the first invoice. When you onboard a new corporate client, you must collect a signed, comprehensive credit application. This document should include the client’s full registered company name, company registration number, VAT number, contact details for the person authorised to incur debt, and a clear acknowledgement of your payment terms. Furthermore, run a credit check on every new business client. Kredcor offers Business Information Reports (BIRs) that give you a detailed financial profile of a potential client before you extend credit. Use them.

Strategy 2: Write Airtight Contracts and SLAs

Your contracts are your first line of defence in any corporate debt collection dispute. Therefore, every IT or telecoms service contract must clearly state: the scope of services, the SLA metrics and how they are measured, the payment terms (including interest on late payments), the dispute resolution procedure, and the consequences of non-payment. Additionally, make sure your SLA performance logs are automated and timestamped. If a client later claims you failed to meet uptime targets, your logs are your evidence.

Strategy 3: Invoice Immediately and Follow Up on Day One

This sounds obvious, but many IT firms delay invoicing — especially for project-based work. Do not. Invoice on the day the service is delivered or the billing period closes. Then follow up on day one of the payment period. Moreover, automate your reminders so that clients receive a friendly reminder three days before the due date, another on the due date, and an escalating series of follow-ups within the first 30 days of default.

“The single most powerful change most IT companies can make to their collections process is simply to start following up earlier. Not aggressively — just consistently. Cash follows urgency, and urgency starts with the creditor.”— Kredcor, B2B Debt Recovery Specialists

Strategy 4: Separate Your Collections Function from Your Sales Team

One of the most common mistakes IT and telecoms firms make is allowing their sales team to manage overdue accounts. As a result, relationship-based reluctance delays action, and the sales team becomes a de facto credit department. Instead, create a clear internal boundary: accounts that reach 30 days past due move to your credit manager or financial manager, not back to the relationship manager. This separation is essential for effective corporate debt collection in the tech sector.

Related Reading: Our article on professional services debt recovery for law, accounting, and tech firms covers the relationship-sensitivity challenge in even more detail, with sector-specific strategies you will find directly applicable.

Strategy 5: Use a Formal Demand Letter at the 30-Day Mark

If a client has not paid by 30 days past due, send a formal written demand. This is not an aggressive move — it is a professional one. The demand letter must state the outstanding amount, the invoice reference numbers, the original due date, and a firm deadline (typically 7–10 business days) for payment. Importantly, it must also state the consequences of non-payment, including referral to a corporate debt collector and potential legal action.

Strategy 6: Engage a Specialist Corporate Debt Collector at the 45-to-60-Day Mark

If the formal demand produces no payment and no credible payment arrangement by day 45–60 of default, hand the account to a registered specialist corporate debt collector. This is the single most impactful step in the entire process. A specialist collector — like Kredcor — brings experience, legal authority, and negotiating leverage that your internal team simply does not have. Moreover, the cost of collection is typically a percentage of what is recovered, meaning there is no upfront financial risk to you.

Strategy 7: Maintain Detailed Communication Records

Throughout the collection process, keep a thorough record of every interaction with the debtor. This includes emails, phone call logs, meeting notes, and any payment promises made. Furthermore, if a debtor makes a payment promise, follow it up in writing the same day. These records are critical if the matter escalates to legal proceedings.

Strategy 8: Leverage Real-Time Data in Your Collections Decisions

Modern IT and telecoms firms have access to more data than ever before. Use it. Specifically, track your average debtor days by client and by product line. Identify patterns — which client types pay late most often? Which service categories generate the most disputes? With this information, you can proactively tighten credit terms for high-risk clients before a debt arises.

Related Reading: Our article on real-time ROI calculators for data-driven debt recovery shows you how to measure the actual financial impact of your collections decisions — and why data beats gut feeling every time.

Strategy 9: Review and Update Your Credit Policy Annually

Download or share this infographic: Corporate Debt Collection for IT & Telecoms Firms in South Africa — 9 Proven Strategies (Kredcor, 2026).

6. The Escalation Timeline: Exactly When to Act

One of the most common questions credit managers ask us is: “When exactly should I escalate?”

Here is our recommended escalation timeline for corporate debt collection in the IT and telecoms sector in South Africa.

- Day 0: Invoice issued. Payment terms confirmed in writing.

- Day -3 (before due date): Automated friendly reminder sent.

- Day 1 (past due): First internal follow-up — email or call.

- Day 14: Second internal follow-up. Escalate internally if no response.

- Day 30: Formal written demand issued. 7–10 day deadline set.

- Day 45–60: If no payment or arrangement — hand to Kredcor. This is the sweet spot for recovery.

- Day 90+: Legal proceedings initiated if required.

- Day 120+: Recovery rate drops below 50%. Act before this point.

Additionally, note that the Prescription Act’s three-year clock starts ticking from the date the debt becomes due. Therefore, do not allow any account to sit unactioned for longer than 12 months without taking steps to interrupt prescription — ideally through acknowledged correspondence or a payment arrangement.

7. Five Troubleshooting Tips for Stalled IT & Telecoms Collections

Even with the best process in place, collections can stall. Here are five specific troubleshooting tips for the most common problems we see in corporate debt collection for IT and telecoms firms.

Troubleshooting Tip 1: The debtor disputes the SLA performance

Pull your service logs, uptime reports, and any support tickets immediately. Compile a clear, timestamped record of service delivery. Send this to the debtor in writing, along with a formal restatement of the amount owed. If they persist with a disputed claim, this evidence is critical for any legal proceeding. Moreover, engage your specialist corporate debt collector to mediate — this often resolves disputes faster than direct negotiation.

Troubleshooting Tip 2: The debtor claims the contract was with a different entity

This is a classic avoidance tactic in the telecoms and IT sector, especially after corporate restructuring. Check your original credit application for the registered company name, CK or CIPC number, and the signatory’s capacity. Furthermore, if the service has continued to be delivered to the same entity under a different name, you may have grounds to pierce the corporate veil. Engage a corporate debt collector with legal capacity immediately.

Troubleshooting Tip 3: The debtor is on a payment plan but keeps missing instalments

A broken payment arrangement is a red flag. First, confirm the arrangement in writing and get a signed acknowledgement of debt (AOD). Second, if the debtor misses two consecutive instalments, treat the full balance as immediately due and payable (this must be stated in your original arrangement). Third, refer the account to a specialist collector without delay — broken arrangements rarely self-correct.

Troubleshooting Tip 4: The debtor’s contact person has changed and no one responds

This is extremely common after corporate restructuring or leadership changes. First, attempt contact through multiple channels: email the accounts department directly, call the switchboard, and send a registered letter to the company’s registered address. Additionally, use a Business Information Report (BIR) from Kredcor to identify current directors and authorised signatories — then direct your demand to them personally.

Troubleshooting Tip 5: Your internal team is too relationship-sensitive to push

This is the most human problem on this list, and also the most common. The solution is structural, not motivational: build a clear credit policy that removes the decision from the relationship manager’s hands. When an account reaches 30 days overdue with no arrangement, the credit manager takes over automatically — without discussion. This protects the relationship manager from the awkwardness and protects your business from the financial consequence.

8. The Clash of Perspectives: Chase Hard or Protect the Relationship?

Here is the honest debate that every IT and telecoms CFO faces: do you push hard for payment and risk damaging the client relationship, or do you preserve the relationship and absorb the cash flow hit? Let’s look at both sides.

✅ The Case for Firm, Early Action

Data clearly supports early escalation. Furthermore, clients who do not pay on time are, statistically, less profitable in the long term. A firm collections process signals that your business is well-run, financially disciplined, and expects to be treated professionally. Moreover, most clients who have genuine cash flow difficulties will actually appreciate a structured payment arrangement — but only if you offer one promptly.

⚠️ The Case for a Softer Approach

Some credit managers argue that aggressive collection in relationship-based sectors like IT and telecoms destroys goodwill that took years to build. Furthermore, in competitive markets, losing a large client over a recoverable debt may cost more in lost future revenue than the debt itself. This view has merit — which is why a specialist corporate debt collector, who can act firmly without personal relationship damage, is so valuable.

Our view at Kredcor is that the debate is largely a false choice. The right answer is: act early, act professionally, and use a specialist. Early, professional escalation recovers debt at the highest rate, and it does so in a way that preserves more goodwill than months of awkward internal follow-up ever could. In other words, the relationship you think you’re protecting with inaction is usually already damaged by the time you escalate — you just haven’t noticed yet.

9. South Africa vs Global Context: What Stays the Same?

Whether you operate in South Africa, across sub-Saharan Africa, or in markets like the UK, USA, or Australia, certain principles of corporate debt collection for IT and telecoms firms remain constant.

Globally, the fundamentals are identical: document everything, invoice promptly, follow up consistently, and escalate early to a specialist. Across every jurisdiction we’ve observed, the longer a commercial debt ages, the lower the recovery rate — without exception.

However, South Africa has specific nuances worth noting. The Prescription Act’s three-year limitation period is shorter than in some jurisdictions (the UK, for example, allows six years). Furthermore, South Africa’s B2B collections landscape is governed by the CFDC, which means only registered collectors can act on your behalf — making it essential to choose a CFDC-registered partner like Kredcor. Additionally, South Africa’s economic environment, including exchange rate pressures on IT importers and the high cost of telecoms infrastructure, means that debtor cash flow crises in this sector can arise quickly and without warning.

“Whether you’re in South Africa or managing a global IT portfolio, the principle of corporate debt collection remains the same: professional, early action gives you the best chance of recovery. What changes is the regulatory framework — and that’s where local expertise makes all the difference.”— Kredcor, Commercial Debt Recovery Partners

10. What to Do Next: Your Search Journey Continues

You have read this guide. Now, the next question most credit managers and CFOs ask is: “What should I actually do in the next 48 hours?” Here is your answer.

First and foremost, audit your current debtors’ book. Identify every account that is more than 30 days overdue and has not yet received a formal demand. Prioritise by value and by the risk of prescription. Then, for every account over 60 days old with no credible arrangement, engage a specialist corporate debt collector immediately.

You can work with professional debt collectors in South Africa who specialise in the IT and telecoms sector. Kredcor’s team has been recovering B2B corporate debt in this space since 1999, with branches in Gauteng, the Western Cape, and KwaZulu-Natal. Getting a quote is free, and there is no upfront cost — Kredcor works on a contingency basis, meaning we only get paid when you do.

Additionally, after you have addressed your immediate debtors’ book, use this article to review and update your credit policy. Make the changes that prevent future debt from reaching the stage of requiring collections action. Furthermore, subscribe to the Kredcor Index to track debtor trends in the South African market in real time.

For more practical, actionable content designed specifically for credit managers, CFOs, and financial managers in South Africa, visit our Kredcor Articles page — where you will find in-depth guides on topics from predictive analytics in collections to cybersecurity for your debt ledger.

11. Quick-Action Checklist: Five Things to Do Right Now

Here is your five-step checklist to take immediate action on corporate debt collection for your IT or telecoms firm in South Africa.

- Audit your debtors’ book today. Identify all accounts over 30 days past due. Flag any over 60 days for immediate escalation.

- Issue formal demands to all accounts over 30 days with no arrangement. Use a written demand with a 7–10 day deadline and state consequences clearly.

- Contact Kredcor for a free quote on all accounts over 45–60 days with no credible payment plan. Early escalation = higher recovery.

- Review your credit application form and SLA documentation. Make sure every new client is properly vetted and every service contract is watertight.

- Schedule an annual credit policy review. Set a date in your calendar — right now — to revisit your credit policy in the next 30 days.

Ready to Recover What You’re Owed?

Kredcor has been South Africa’s trusted B2B corporate debt collection partner since 1999. Registered with the Council for Debt Collectors (CFDC Reg. Nr. 0016365/06), we recover IT and telecoms debt professionally, efficiently, and on a contingency basis — no recovery, no fee. Get a Free Quote Now →

Frequently Asked Questions: Corporate Debt Collection for IT & Telecoms Firms in SA

How long does corporate debt collection take for IT companies in South Africa?

On average, invoices handed to a specialist commercial debt collector within 60–90 days of default achieve recovery rates of 80–90%. Beyond 120 days, recovery rates drop sharply — often below 50%. For IT and telecoms firms specifically, acting early (ideally within 30 days of a missed payment) gives you the best chance of a swift, full recovery. Moreover, the process itself — from first contact by a specialist collector to settlement — often takes as little as a few weeks for cooperative debtors, and a few months for more complex matters.

Is corporate debt collection legal in South Africa for B2B disputes?

Yes, absolutely. B2B corporate debt collection in South Africa is governed by the Debt Collectors Act 114 of 1998, which is overseen by the Council for Debt Collectors (CFDC). Only CFDC-registered collectors may legally collect debt on behalf of creditors. Kredcor is registered (CFDC Reg. Nr. 0016365/06) and operates strictly within this legal framework. Furthermore, the National Credit Act (NCA) primarily covers consumer credit and generally does not apply to business-to-business debts — meaning B2B collections face fewer procedural hurdles.

What makes IT and telecoms debt collection different from other sectors?

IT and telecoms debt is uniquely complex because contracts typically involve recurring services — SaaS subscriptions, managed services, cloud hosting, and connectivity. When disputes arise, they often cover entire service periods rather than a single invoice. Additionally, clients frequently dispute charges tied to SLA performance. IT and telecoms companies also tend to be deeply relationship-sensitive, which causes internal teams to delay escalation — often for 6–8 months, which is far too late for optimal recovery. These combined factors make specialist corporate debt collection critical for this sector.

When should an IT or telecoms company use a debt collector instead of their own team?

You should engage a specialist corporate debt collector when: a debtor has missed payment by more than 30 days without a clear payment arrangement; internal follow-up has produced no result after two escalation attempts; the debtor disputes the debt without formal written grounds; or the amount owed justifies professional recovery action. As a general rule, any account over 45–60 days past due with no credible arrangement should be in the hands of a specialist. The sooner you hand over, the better your recovery rate — and the less time your team spends on unproductive follow-up calls.

How Corporate Debt Collection Differs Across IT & Telecoms Product Types

Not all technology debt looks the same. Consequently, your corporate debt collection approach for an IT or telecoms firm in South Africa must be tailored to the type of product or service that was delivered. Let’s walk through the most common categories and how each one presents unique collection challenges.

SaaS (Software as a Service) Subscriptions

SaaS corporate debt collection is particularly tricky because the service is continuous. When a client stops paying, you face an immediate decision: do you cut off access and risk inflaming the dispute, or do you maintain service and compound the debt? Our team’s experience strongly recommends a middle path — suspend access after a 14-day grace period beyond the formal demand, while simultaneously escalating to a specialist collector. Furthermore, make sure your terms of service clearly state your right to suspend or terminate access upon default. This gives you a contractual basis for action that is very difficult for a debtor to challenge.

Managed Services and IT Outsourcing

Managed service provider (MSP) debt is among the most complex to collect. The reason is that managed service contracts typically cover a broad range of services — helpdesk support, network monitoring, backup management, cybersecurity — and any one of these can become the basis of a dispute. Therefore, when you initiate corporate debt collection on a managed services account, you need a comprehensive file that documents every service delivered, every ticket resolved, and every SLA metric met. Without this, the debtor can easily shift the conversation from “I owe you money” to “did you even deliver what you promised?”

Telecoms Connectivity and Hosted Voice

Telecoms corporate debt collection in South Africa has an additional layer of complexity: the Independent Communications Authority of South Africa (ICASA) regulates the telecoms sector, and its guidelines can sometimes intersect with your collections process — particularly around service disconnection. Additionally, telecoms companies often deal with disputed call records, data usage charges, and line rental fees. Each of these can become a sticking point in the corporate debt collection process. To navigate this effectively, work with a specialist collector who understands both the telecoms regulatory environment and the collections landscape in South Africa.

Hardware Supply and IT Equipment

When an IT company supplies physical hardware — servers, networking equipment, end-user devices — the debt is more straightforward to prove than for services. However, corporate debt collection for hardware can be complicated by disputes around delivery, damage, or compatibility. Therefore, always ensure you have signed delivery notes, proof of delivery (POD), and a clear acceptance protocol in your contracts. Furthermore, if the debt is secured against the equipment itself (a retention of title clause), your collector can advise on the appropriate legal steps for repossession.

Cloud Hosting and Data Centre Services

Cloud hosting debt collection is growing rapidly as more South African businesses migrate to the cloud. The challenge here is that cloud services are typically billed on consumption — and consumption can vary dramatically month to month. Therefore, make sure your billing system generates detailed, itemised invoices that clients can verify. Disputed cloud bills are almost always resolved faster when the client can see exactly what they consumed. Moreover, for cloud hosting contracts, include a clear clause that allows you to throttle or suspend resources upon default — this gives you practical leverage in the corporate debt collection process without requiring immediate legal action.

Building a Credit Policy That Prevents Corporate Debt Collection Crises

The best corporate debt collection outcome is the one you never need. So, let’s talk about prevention. A well-structured credit policy is the single most powerful tool your IT or telecoms business can have — and yet, in our experience, fewer than 30% of small to medium-sized technology companies in South Africa have a formal, written credit policy.

What Your Credit Policy Must Cover

Your credit policy should address the following areas as a minimum:

- Credit vetting: Define the minimum criteria for extending credit to new clients. Include requirements for a signed credit application, company registration verification via the CIPC (Companies and Intellectual Property Commission), and a Business Information Report (BIR) from Kredcor for all accounts over a defined threshold.

- Credit limits: Set clear credit limits for each client tier. Review these limits annually or whenever a client’s payment behaviour changes.

- Payment terms: State your standard payment terms clearly — typically 30 days from invoice date for B2B transactions in South Africa. Furthermore, include a clause for interest on late payments (the Prescribed Rate of Interest Act sets the default interest rate for commercial debts in SA).

- Escalation triggers: Define the exact conditions that trigger each escalation step — from the first internal follow-up to the point of corporate debt collection handover.

- Dispute resolution: Include a clear, time-bound dispute resolution process. This prevents clients from using unresolved disputes as an indefinite reason to withhold payment.

The Cost of Not Having a Credit Policy

Many IT and telecoms SME owners underestimate the cost of operating without a formal credit policy. However, the numbers tell a stark story. If your business turns over R10 million per year and 62% of your invoices are paid late (the South African average), you are potentially managing R6.2 million in delayed receivables at any given time. Even at a conservative cost of capital of 10%, that represents a direct financing cost of R620,000 per year — money you are effectively lending to your clients for free. A solid credit policy, combined with timely corporate debt collection for IT and telecoms when needed, can recover a significant portion of that cost.

How to Choose the Right Corporate Debt Collection Agency for Your IT Firm

Not all corporate debt collectors are created equal. Therefore, when you choose a corporate debt collection agency for your IT or telecoms business in South Africa, look for the following qualities.

CFDC Registration is Non-Negotiable

First and most importantly, confirm that your collector is registered with the Council for Debt Collectors (CFDC). This is a legal requirement in South Africa. Only CFDC-registered collectors can legally demand payment on behalf of a creditor. If a collector cannot provide their CFDC registration number upfront, walk away. Kredcor’s registration number is 0016365/06 — verifiable on the CFDC’s official register.

Sector-Specific Experience Matters

Furthermore, look for a collector with proven experience in the IT and telecoms sector. General-purpose collectors often lack the technical understanding needed to counter SLA dispute arguments or handle cloud hosting billing disputes effectively. In contrast, a collector who has worked with MSPs, SaaS companies, and telecoms providers brings industry-specific knowledge that significantly improves your recovery outcomes.

Contingency-Based Fees Align Incentives

Additionally, prefer a collector who works on a contingency basis — meaning they charge a percentage of what they recover, with no upfront fees. This model aligns the collector’s incentives directly with yours. If they do not recover your debt, they do not get paid. This is the standard model for corporate debt collection in South Africa, and it is the model Kredcor uses.

National Reach in South Africa

Moreover, for IT and telecoms companies that serve clients across multiple provinces, choose a collector with national coverage. Kredcor has branches in Gauteng, the Western Cape, and KwaZulu-Natal, as well as Africa-wide and global capabilities — meaning we can pursue your debtors wherever they operate.

A Transparent, Communicative Process

Finally, choose a collector who keeps you informed throughout the corporate debt collection process. You should receive regular status updates on each account, clear documentation of every action taken, and prompt notification of any payment received or arrangement made. Transparency is not just a nice-to-have — it is essential for your own compliance and financial reporting obligations.

LSI Terms & Semantic Context: How This Topic Fits Together

For the benefit of credit professionals and search engines alike, here is how the key terms in this article relate to one another. Corporate debt collection for IT and telecoms firms in South Africa sits at the intersection of several important concepts: B2B debt recovery, commercial collections, accounts receivable management, credit risk management, debtor days management, invoice financing, SLA dispute resolution, and the South African regulatory framework for debt.

Furthermore, related subtopics include: managed service provider (MSP) debt recovery, SaaS subscription non-payment, telecoms arrears collection, technology sector credit management, CFDC-registered collectors, Business Information Reports, acknowledgement of debt (AOD), Prescription Act implications, and the distinction between consumer collections (NCA-governed) and B2B corporate debt collection (Debt Collectors Act-governed).

Taken together, these concepts form the complete landscape of IT and telecoms corporate debt collection in South Africa — and Kredcor’s expertise covers all of them.

KREDCOR · Commercial Debt Recovery Partners · Est. 1999

CFDC Reg. Nr. 0016365/06 · www.kredcor.co.za

Branches: Gauteng · Western Cape · KwaZulu-Natal · Africa · Global

© 2026 Kredcor. All rights reserved. This article is provided for informational purposes. For legal advice on specific debt collection matters, consult a qualified attorney.