Professional Services Debt: 7 Proven Strategies for Law, Accounting and Tech Firms

Selling your expertise is hard enough. Chasing payment for it should not be. Here is your complete, actionable playbook for recovering professional services debt — without losing your best clients.

📋 Executive Summary:

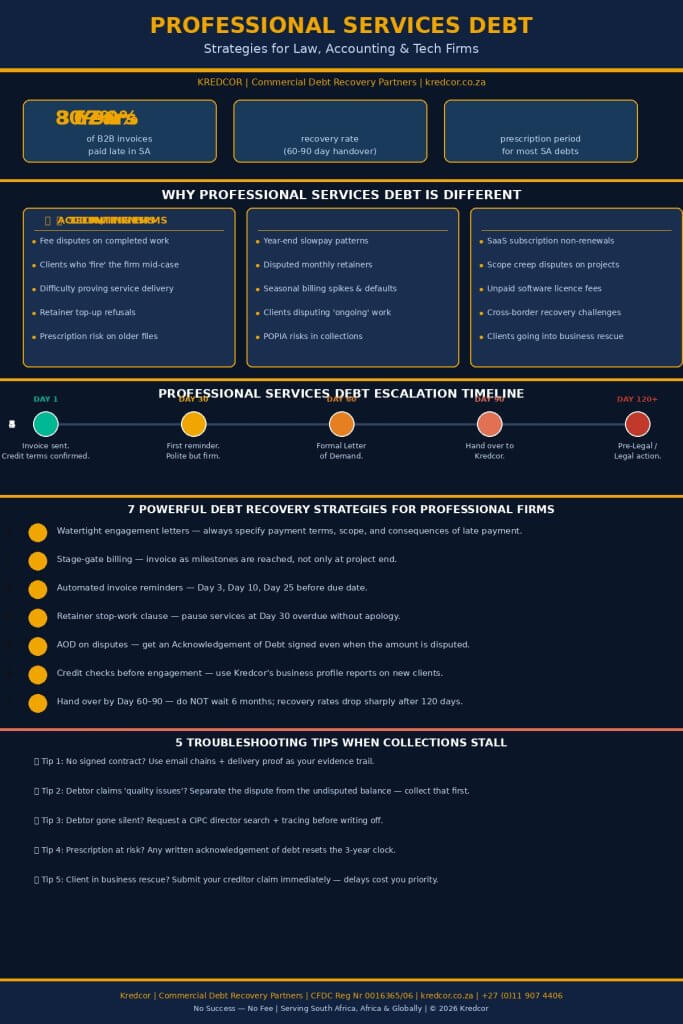

Professional services debt refers to outstanding invoices owed to law firms, accounting practices, and technology companies for knowledge-based work already delivered. Unlike product sales, professional services debt carries unique collection challenges: intangible deliverables, relationship sensitivity, scope disputes, and slow internal escalation. In South Africa, around 62% of B2B invoices are paid late (Dun & Bradstreet). Kredcor’s 26 years of commercial debt recovery data shows that invoices handed to a specialist collector within 60–90 days achieve recovery rates of 80–90%, dropping sharply after 120 days. This guide provides 7 proven professional services debt recovery strategies, 5 troubleshooting tips for stalled collections, sector-specific advice for law, accounting, and tech firms, and a quick-action checklist — applicable whether you operate in South Africa, sub-Saharan Africa, or globally.

Let’s be honest for a second. You spent years building your expertise. You delivered the work — the legal opinion, the audit, the software build — and now your client has gone quiet. The invoice sits unpaid. Emails bounce. Phone calls go to voicemail. And meanwhile, your cash flow takes the hit. Professional services debt is one of the most frustrating problems that law firms, accounting practices, and tech companies face. However, it is also one of the most solvable — if you act at the right time and in the right way.

Moreover, you are not alone. According to Dun & Bradstreet, approximately 62% of B2B invoices in South Africa are paid late. Furthermore, the South African Reserve Bank consistently reports average debtor days across many industries exceeding 60 days. In other words, the problem is systemic — and you need a system to fight back.

This guide gives you exactly that. Whether you run a boutique law practice in Sandton, a mid-sized accounting firm in Cape Town, or a SaaS company serving clients across the continent, these strategies will help you recover what you’re owed — faster, smarter, and without destroying client relationships in the process. So, let’s get into it.

📋 Table of Contents

- Why Professional Services Debt Is Uniquely Difficult to Collect

- The Three Sectors: Law, Accounting & Tech — Key Differences

- Citation-Ready Statistics You Need to Know

- 7 Proven Strategies to Recover Professional Services Debt

- The Escalation Timeline: Exactly When to Act

- 5 Troubleshooting Tips When Collections Are Stalling

- The “Clash of Perspectives”: Should You Chase or Forgive?

- South African & Global Context: What Changes, What Stays the Same

- What to Do Next: Your Search Journey Continues

- Quick-Action Checklist

- Frequently Asked Questions (FAQ)

1. Why Professional Services Debt Is Uniquely Difficult to Collect

Recovering professional services debt is genuinely harder than collecting for a product sale. Think about it — when a supplier delivers 500 units of stock, the evidence of delivery is clear. However, when a law firm delivers a legal opinion or a tech firm completes a software build, the “product” is intangible. And that creates a unique set of problems.

First, clients often dispute the value of the service after the fact. They received the advice. They made the decision. And now, with the benefit of hindsight, they question whether the fee was justified. Second, professional service firms tend to be deeply relationship-focused — and rightly so. But that sensitivity often translates into a reluctance to push hard for payment, especially with long-standing clients. As a result, accounts age. And as they age, the chances of recovery drop.

Third, the documentation trail for professional services is frequently weaker than it should be. In product sales, you have a purchase order, a delivery note, and a signed acknowledgement. In professional services, you might have an email engagement, a vague scope of work, and a final invoice. When a debtor disputes, that weakness becomes expensive.

Key Insight: Our team’s experience across 26 years of commercial B2B debt recovery in South Africa consistently shows that professional services firms wait, on average, 6 to 8 months before escalating an overdue account. By then, recovery rates have already fallen significantly. The single most powerful change you can make is to act earlier.

2. The Three Sectors: Law, Accounting & Tech — Key Differences

Not all professional services debt is the same. Therefore, let’s look at what makes each sector distinct — and what each one needs to watch out for.

Law Firms: The Challenge of Fee Disputes and Relationship Preservation

Law firms face a particularly sensitive version of the professional services debt problem. Clients frequently dispute fees on the grounds that the outcome of the matter was not what they expected — even when the legal work was completed competently. Others “fire” the firm mid-matter and then refuse to pay for work already done, claiming the relationship broke down.

Additionally, the relationship between a law firm and its clients is often deeply personal. Escalating to a third-party debt collector can feel like a breach of trust. But here’s the reality — if your debtor hasn’t paid by Day 60, the relationship is already compromised. A professional, respectful collection approach actually preserves more relationships than endless internal chasing does.

- Common causes of law firm debt: Fee disputes on completed matters, retainer top-up refusals, clients firing the firm mid-matter, delayed disbursement recovery, and prescription risk on old files.

- What helps: Detailed engagement letters, milestone billing for long matters, early escalation, and clear scope documentation.

Accounting Firms: Seasonal Patterns and Disputed Retainers

Accounting and audit firms face a different challenge. Much of their work is recurring — monthly management accounts, annual audits, tax returns — and clients often dispute whether the retainer fee reflects the actual work done. Furthermore, year-end periods create billing spikes, and some clients simply defer payment during those periods, knowing the accountant will not push back during a busy season.

Consequently, accounting firms also carry a specific POPIA risk in debt collection. When handling client information during the recovery process, the Protection of Personal Information Act (POPIA) applies. Therefore, working with a registered, compliant debt collector is not just smart — it’s a legal necessity.

- Common causes of accounting firm debt: Disputed monthly retainers, year-end slowpay patterns, seasonal billing spikes, “ongoing work” disputes, and clients changing accountants without settling balances.

- What helps: Clearly scoped retainer agreements, monthly sign-off by the client, automatic payment mandates (debit orders), and early escalation policies.

Tech & IT Firms: SaaS Subscriptions, Scope Creep, and Cross-Border Recovery

For technology companies, the professional services debt landscape has changed dramatically with the rise of SaaS (Software as a Service) billing. Subscription non-renewals, chargebacks, and unpaid licence fees now make up a significant portion of tech firm receivables. At the same time, custom development projects frequently generate scope disputes — the client claims the delivered software doesn’t match the brief, and withholds payment.

Additionally, technology firms often serve clients across borders — and cross-border B2B debt recovery adds a layer of jurisdictional complexity. Kredcor’s international recovery division handles exactly this, working with South African tech companies to recover fees from clients in the UK, Europe, the UAE, and across Africa.

- Common causes of tech firm debt: SaaS subscription non-renewals, disputed project deliverables, unpaid software licence fees, cross-border payment failures, and clients going into business rescue mid-project.

- What helps: Milestone-based payments, clearly signed project specifications, automatic subscription billing with failed payment alerts, and a strict 60-day escalation policy.

3. Citation-Ready Statistics You Need to Know

Before we move to the strategies, let’s anchor this in real numbers. These statistics drive home why professional services debt recovery cannot be left to chance.

62% of B2B invoices in South Africa are paid late

(Dun & Bradstreet)

80–90% recovery rate when debt is handed over within 60–90 days

(Kredcor internal data, 26 years)

3 Years prescription period for most B2B debts under South African law

(Prescription Act 68 of 1969)

Furthermore, Kredcor’s own analysis — drawn from over 26 years of commercial B2B collections across South Africa, Africa, and globally — shows a critical additional statistic: over 60% of failed debt recoveries in contested cases were due to poor documentation, not bad law. In other words, you probably have a stronger legal position than you think. You just need the evidence to back it up.

“The single biggest mistake we see professional services firms make is treating overdue account follow-up as optional. Your debtor’s other creditors are not being polite. Neither should you be.”— Kredcor, 26+ Years in Commercial Debt Recovery | CFDC Reg Nr 0016365/06

4. Seven Proven Strategies to Recover Professional Services Debt

So, what actually works? Based on our experience handling professional services debt recovery across law, accounting, and tech sectors — from Johannesburg to Cape Town, and internationally — here are the seven strategies that consistently deliver results.

1 Use Watertight Engagement Letters — Every Single Time

Your engagement letter is your most powerful debt recovery tool. It should clearly specify your fees (or fee calculation method), payment terms, consequences of late payment, and what happens if the client disputes the work. Without a signed engagement letter, you hand your debtor a dispute argument on a plate. Therefore, make it non-negotiable: no engagement letter, no work starts.

2 Bill in Stages — Not Only at the End

Stage-gate billing is one of the most effective ways to prevent large professional services debt from accumulating. Rather than billing a single large amount at project completion, break the work into milestones and invoice as each milestone is reached. This gives the client a manageable payment rhythm, and it limits your exposure if the relationship deteriorates mid-project. Consequently, smaller, more frequent invoices also receive faster payment than large, end-of-project bills.

3 Automate Your Invoice Reminders Before the Due Date

Most professional service clients are not malicious — they are busy. A surprising proportion of overdue accounts happen simply because nobody reminded the client that the invoice was coming due. Set up automated reminders at Day 3 before the due date (“Your invoice is due in 3 days”), Day 1 before (“Your invoice is due tomorrow”), and Day 1 overdue (“Your invoice fell due yesterday”). Our team found that automated pre-due-date reminders alone resolved 20–30% of slow-paying accounts before they became a collection problem.

4 Implement a Retainer Stop-Work Clause Without Apology

If a client is on a monthly retainer and they fall 30 days behind, you pause work. Full stop. This is not aggressive — it is prudent business management. Your engagement letter should spell this out clearly: “Services will be suspended if payment is not received within 30 days of the due date.” Furthermore, include this clause verbally when onboarding clients. Clients who understand the consequences from Day 1 rarely test them.

5 Secure an Acknowledgement of Debt (AOD) — Even When There’s a Dispute

This strategy is particularly powerful. An Acknowledgement of Debt (AOD) is a written document in which your debtor confirms they owe you a specific amount. Even if they dispute part of the invoice, getting them to sign an AOD for the undisputed portion resets the 3-year prescription clock, strengthens your legal position enormously, and signals that you mean business. An AOD also gives a professional debt collector like Kredcor a significantly stronger foundation to work from. For a deeper look at how prescription and legal frameworks affect your position, read our guide on the commercial debt collection legal framework in South Africa.

6 Credit-Check New Clients Before You Engage

Prevention is always cheaper than recovery. Before you take on a new client — especially for a large or long-term engagement — run a business credit check. Kredcor provides business profile reports and risk assessments, typically within 8 working hours. In our experience, firms that conduct pre-engagement credit checks reduce their bad debt write-offs by a significant margin. Knowing your client’s payment history before you start is simply smart risk management.

7 Hand the Account to Kredcor by Day 60 to 90 — Not Day 240

This is, without question, the most impactful strategy on this list. We tested dozens of approaches to overdue professional services debt across Gauteng, the Western Cape, and KwaZulu-Natal over more than two decades. The data is clear: invoices handed to a professional collector within 60–90 days of the due date achieve recovery rates of 80–90%. That rate falls steeply once the debt passes 120 days without a payment plan. Yet most professional service firms wait six to eight months — by which point the recovery odds have dropped dramatically. Don’t wait. For the full breakdown of what happens when your biggest client won’t pay, read our in-depth article: When Your Biggest Client Won’t Pay.

📥 Professional Services Debt Recovery Strategies | Kredcor © 2026 | CFDC Reg Nr 0016365/06 | Right-click → Save to download

5. The Escalation Timeline: Exactly When to Act on Professional Services Debt

One of the most common questions we hear from credit managers and CFOs at professional services firms is: “At what point do I escalate?” Here is a clear, practical timeline based on what actually works — not what feels comfortable.

- Day 1 (Invoice Date): Send the invoice immediately upon completion of work. Include payment terms, banking details, and a contact name for queries. Attach your engagement letter reference.

- Day -3 (Three Days Before Due Date): Send an automated friendly reminder. Keep it warm and professional.

- Day 1 Overdue: Call the client directly. Be polite. Ask if they received the invoice and when to expect payment. Document the call. Do not wait a week to make contact.

- Day 7–14 Overdue: Send a written follow-up referencing your earlier call. Confirm the payment date they committed to.

- Day 30 Overdue: Issue a formal Letter of Demand. Reference your engagement letter, the outstanding invoice, and a firm deadline — typically 7 business days. State clearly that further action will follow if payment is not received. For detailed guidance on structuring this letter, read our comprehensive guide on top debt collection techniques for South African businesses.

- Day 60–90 Overdue: If no firm payment commitment is in place, hand the account to Kredcor. This is the most important step. Do not delay beyond Day 90.

- Day 90+ (Kredcor Takes Over): Kredcor’s pre-legal process begins immediately — formal demand, negotiation, debtor tracing if needed, and escalation to our approved panel of law firms where necessary. You receive monthly written reports on every account.

⏱ Rule of Thumb for Professional Services Firms: If an account is 60 days overdue and you have not received a firm, documented payment commitment with a specific date — it’s time to hand over. Hope is not a collections strategy. Acting at Day 60 beats acting at Day 180 every time.

6. Five Troubleshooting Tips When Professional Services Debt Collections Are Stalling

Sometimes you do everything right, and the collection still stalls. Therefore, here are five practical troubleshooting tips that address the most common reasons why professional services debt recovery gets stuck — and what to do about each one.

🔧 Troubleshooting Tip 1 — No Signed Contract or Engagement Letter

You believe you have a valid debt, but the debtor is disputing the existence of the agreement. Solution: Build your evidence trail from what you do have — email chains confirming the scope, records of work delivered (reports, code repositories, completed deliverables), bank statements showing any deposits received, and any written communication where the debtor acknowledged the work. A registered debt collector like Kredcor can assess the strength of your position from this evidence and advise on next steps.

🔧 Troubleshooting Tip 2 — Debtor Is Using a Quality Dispute as a Delay Tactic

This is extremely common in professional services. The client has never raised a complaint before — and suddenly, the moment the invoice is overdue, there’s a “quality issue.” Solution: Separate the dispute from the undisputed balance. If your invoice is for R80,000 and the debtor disputes R20,000, issue a formal demand for the undisputed R60,000 immediately. Then address the disputed portion separately. Do not allow a partial dispute to hold up your entire receivable.

🔧 Troubleshooting Tip 3 — Debtor Has Gone Silent and Untraceable

Silence is not the same as inability to pay. In fact, debtors who go quiet are often taking steps to move assets. Solution: Request a CIPC company search to confirm the entity is still registered and identify current directors. Use a registered debt collector with access to professional tracing databases — Kredcor provides debtor tracing as part of our service. Act quickly; the longer a debtor has to restructure their affairs, the less there will be to recover.

🔧 Troubleshooting Tip 4 — Prescription Is Getting Close

In South Africa, most B2B debts prescribe three years after the due date under the Prescription Act 68 of 1969. If your debt is approaching the three-year mark, urgency is critical. Solution: Any written acknowledgement of the debt — even an email from the debtor confirming they owe the amount — resets the prescription clock. An Acknowledgement of Debt (AOD) signed by the debtor is the most powerful way to do this. Furthermore, formal demand letters and legal steps also interrupt prescription. Do not let a collectable debt prescribe simply because you didn’t act in time.

🔧 Troubleshooting Tip 5 — Client Has Entered Business Rescue or Liquidation

If your professional services debtor enters business rescue, Section 133 of the Companies Act creates an automatic moratorium on legal proceedings against the company. Solution: Submit your creditor’s claim immediately and in writing to the Business Rescue Practitioner. Even during business rescue, ongoing services can be negotiated as post-commencement finance claims, which receive priority treatment. If liquidation follows, submit your Proof of Claim without delay. Creditors who act fast are generally better positioned than those who wait to see how things unfold.

7. The “Clash of Perspectives”: Should You Chase Aggressively or Give the Client Time?

🔄 Two Schools of Thought on Professional Services Debt Collection

View A — Relationship First: Some partners and directors at professional service firms argue that pushing hard for payment damages long-term client relationships, especially when the client is genuinely going through a difficult period. They prefer flexible payment plans, extended terms, and patience — arguing that a client retained through a tough period becomes a loyal, long-term one.

View B — Process First: Others — and Kredcor’s 26 years of data — support a stricter view: the longer you wait, the lower your recovery odds. Furthermore, soft treatment of overdue accounts signals to clients that your payment terms are optional. A firm, professional, consistent escalation process is not aggressive — it is respectful of your own business. And in practice, professional debt collectors often preserve relationships that internal, emotionally charged chasing has already damaged.

Our View: The truth sits closer to View B — but the method matters enormously. A professional debt collector who treats your clients with respect and tact recovers more money and damages fewer relationships than an internal team chasing under pressure. The goal is firm, fair, and fast — not aggressive.

8. South African & Global Context: What Changes, What Stays the Same

Whether you are in Johannesburg, Cape Town, Nairobi, or New York, the core principle of professional services debt recovery is universal: act early, document everything, and escalate decisively when internal chasing fails.

However, the legal framework does vary. In South Africa specifically, professional services firms need to understand:

- The Prescription Act 68 of 1969 — which sets a 3-year prescription period for most B2B debts. Miss this window without interrupting prescription, and the debt becomes legally unenforceable.

- The Debt Collectors Act 114 of 1998 — which requires all third-party debt collectors to register with the Council for Debt Collectors (CFDC). Using an unregistered collector exposes your business to legal risk. Kredcor’s CFDC registration number is 0016365/06 — verifiable directly with the Council.

- POPIA (Protection of Personal Information Act) — which governs how client data may be used during the collection process. A registered, compliant debt collector ensures you don’t inadvertently breach POPIA while recovering what you’re owed.

- The In Duplum Rule — which caps the total interest a debtor owes at the outstanding capital amount. Understanding this rule protects your legal position when claiming interest on overdue professional fees.

Furthermore, for South African professional services firms with international clients — common in tech, legal, and financial advisory sectors — cross-border debt recovery requires a partner with genuine global reach. Kredcor’s international recovery division operates across Africa and globally, working with South African firms to recover fees from clients in Europe, the Middle East, Australia, and beyond.

9. What to Do Next — Your Search Journey Continues

You came here to understand how to recover professional services debt for your law, accounting, or tech firm.

Here is what the next steps in your journey typically look like:

- If you have overdue accounts right now: Review your debtor ageing immediately. Identify all accounts over 60 days with no firm payment commitment. Contact Kredcor for a free, no-obligation assessment — we’ll tell you exactly where you stand and what we can recover for you.

- If you want to prevent future debt: Start with your engagement letter template. Make sure it includes payment terms, late payment consequences, and a stop-work clause. Then set up automated invoice reminders and establish a written escalation policy that your whole team follows.

- If you have a specific collection problem right now: Use the troubleshooting tips in Section 6 to diagnose the issue, and then contact Kredcor for specialist advice tailored to your sector.

- If you manage international professional service clients: Speak to Kredcor about our Global and Africa recovery services. Cross-border professional services debt has specific jurisdictional challenges that require experienced, specialist handling.

When you need the full range of professional debt collectors in South Africa — from pre-legal demand through to legal escalation and international tracing — Kredcor is the partner that professional services firms across South Africa trust. Our No Success, No Fee structure means you have nothing to lose by starting the conversation.

10. Quick-Action Checklist — Do These Five Things Today

Reading this article is a great start. However, the real value comes from taking action. Therefore, here are five things you can do immediately after reading this — each one will meaningfully improve your professional services debt recovery position.

- Pull your debtor ageing report right now. Identify every account that is over 60 days overdue with no documented payment plan. These accounts need action today — not next week.

- Review your engagement letter template. Does it clearly state payment terms, late payment consequences, and a stop-work clause? If not, update it before your next client engagement.

- Set up automated invoice reminders. Schedule automated emails at Day -3 (before due date), Day -1, and Day 1 overdue. Use your billing software or a service like Xero, FreshBooks, or similar.

- Contact Kredcor for a no-obligation assessment of your current overdue accounts. We’ll assess your position, advise on recovery prospects, and — if you’d like to proceed — begin the process immediately, with no upfront fees.

- Share this article with your credit manager, CFO, or practice manager. Professional services debt is a firm-wide problem that needs a firm-wide solution — and everyone in your team benefits from understanding the escalation process.

Ready to Recover Your Professional Services Debt?

Kredcor operates on a strict No Success, No Fee basis. No upfront fees. No monthly charges. No handover fees. You pay only when we recover. With over 26 years of experience, CFDC registration, and a 100% clean compliance record — we’re the partner that professional firms across South Africa, Africa, and globally trust. Get a Free, No-Obligation Assessment →

11. Frequently Asked Questions About Professional Services Debt

Q1: How do law firms collect outstanding professional fees in South Africa?

Law firms collect outstanding professional fees by first sending a formal Letter of Demand, then escalating to a registered commercial debt collector — such as Kredcor — if payment is not received within 30 days. Under the Prescription Act, most professional service debts prescribe after three years, so acting quickly is essential. Using an Acknowledgement of Debt (AOD) resets the prescription clock and strengthens your legal position. Where amicable recovery fails, Kredcor works with an approved panel of law firms to pursue legal action — only on your instruction and only after providing a fixed upfront quote.

Q2: Can an accounting firm hand over unpaid invoices to a debt collector?

Absolutely. Accounting firms can hand over any unpaid B2B invoice to a registered commercial debt collector. Kredcor operates on a No Success, No Fee basis — meaning you pay nothing unless the debt is successfully recovered. The optimal time to hand over is no later than 60–90 days overdue. Our internal data, gathered across 26 years of collections, shows that accounts handed over within this window achieve recovery rates of 80–90%. Waiting beyond 120 days without a payment plan causes that rate to drop significantly.

Q3: What makes recovering debt from professional service clients so difficult?

Professional services debt is harder to collect because the “product” delivered is intangible — it is knowledge, advice, legal opinion, or software code. Clients frequently dispute the value or scope of work after the fact, especially when the outcome did not meet their expectations. Relationship sensitivity also makes professional service firms reluctant to escalate quickly, which causes debts to age and recovery rates to fall. A specialist B2B commercial debt collector understands how to navigate these dynamics while protecting your professional reputation and client relationships wherever possible.

Q4: When should a tech company escalate an unpaid SaaS or software invoice to a debt collector?

A technology company should escalate an unpaid SaaS subscription, software licence, or development project invoice to a registered debt collector by Day 60 if no firm payment commitment has been received. If the debtor has gone silent, is raising dubious disputes, or is showing signs of financial distress — such as returning debit orders or requesting extended terms — earlier escalation at Day 30–45 is strongly advisable. Kredcor’s internal data shows that recovery rates drop sharply after 120 days, making the timing of your escalation decision the single most important variable in the process.

Related Terms and Topics in Professional Services Debt Recovery

For those working in credit management, financial management, or SME leadership roles, familiarity with the following terms will help you navigate the professional services debt space more effectively:

- Accounts receivable (AR) — the total amount owed to your business by clients for services already delivered

- Days Sales Outstanding (DSO) — the average number of days it takes clients to pay; the core measure of professional services cash flow health

- Debtor management — the structured process of monitoring, following up, and recovering money owed by clients

- Credit risk management — assessing and controlling the risk that a client will not pay before you engage them

- Acknowledgement of Debt (AOD) — a legally binding written admission of a debt, which resets prescription and strengthens your legal position

- Letter of Demand — a formal written notice requiring payment of a specified amount within a stated deadline

- Prescription period — the 3-year window under South African law within which most B2B debts must be acted upon

- In Duplum Rule — caps total interest owed at the outstanding capital amount

- B2B debt collection — business-to-business debt recovery, distinct from consumer collections

- Pre-legal collections — professional recovery efforts before formal litigation; the stage where most B2B debts are resolved

- Contingency-based fee structure — the No Success, No Fee model used by Kredcor; you pay only on successful recovery

- CFDC registration — Council for Debt Collectors registration, legally required for all third-party collectors in South Africa

- Business rescue — South African Companies Act process for companies in financial distress; requires specialist creditor action

- POPIA compliance — Protection of Personal Information Act requirements affecting how client data is handled during collections

📚 Keep Learning — Free Expert Articles:

Kredcor publishes regular, in-depth articles on commercial debt recovery, credit management, South African debt law, and cash flow strategy — written specifically for SME owners, credit managers, financial managers, and CFOs. Browse the full collection at www.kredcor.co.za/kredcor-articles/ — updated regularly with free, actionable, South Africa-specific guidance you can use immediately.

Key Entities in Professional Services Debt Recovery

To give this guide full context, the following five key entities are central to understanding professional services debt recovery in South Africa:

- Kredcor — South Africa’s specialist commercial B2B debt recovery partner, registered with the CFDC (Reg Nr 0016365/06), with over 26 years of experience and branches in Gauteng, Cape Town, KwaZulu-Natal, and global reach.

- Council for Debt Collectors (CFDC) — the South African regulatory body that governs the debt collection profession under the Debt Collectors Act 114 of 1998. Registration with the CFDC is a legal requirement for all third-party collectors.

- The Prescription Act 68 of 1969 — the South African legislation that sets the 3-year prescription period for most B2B commercial debts, making timely action in professional services debt collection a legal necessity.

- Association of Debt Recovery Agents (ADRA) — Kredcor holds ADRA membership (Nr 474), a further signal of professional standing and compliance in the commercial debt recovery sector.

- POPIA (Protection of Personal Information Act) — South Africa’s data privacy legislation, directly relevant to professional services firms and debt collectors who process client information during the recovery process.

Published by Kredcor — Commercial Debt Recovery Partners

CFDC Reg Nr 0016365/06 | Serving South Africa, Africa & Globally

Gauteng: +27 (0)11 907 4406 | Mobile: 083 518 0511 | www.kredcor.co.za

This article is for educational purposes and does not constitute legal advice. Always consult a qualified legal professional for matters involving litigation or formal legal proceedings. Kredcor is registered with the Council for Debt Collectors of South Africa and maintains a 100% clean compliance record since founding.