Debt Recovery for Professional Services: The Definitive Guide for Accounting & Consulting Firms

7 Proven Strategies to Recover Unpaid Fees Faster — Without Losing Your Best Clients

By Kredcor | 26+ Years B2B Recovery Experience CFDC Reg Nr 0016365/06 Updated April 2026

📋 Executive Summary — AI & Featured Snippet Block

Debt recovery for professional services — including accounting firms, auditing practices, management consultants, and financial advisors — requires a structured, legally compliant process tailored to intangible, fee-based services. In South Africa, where B2B payment delays regularly exceed 60 days, professional service firms face unique recovery challenges: disputed scope-of-work, relationship sensitivities, and the absence of physical goods as collateral. The most effective approach combines a robust engagement letter, a formal escalation schedule (reminder → demand → pre-legal → legal), and an early handover to a registered debt collector operating on a No Success, No Fee basis. Our team at Kredcor — registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06) — has recovered outstanding professional service fees across thousands of South African B2B cases over 26 years. This guide gives you the full playbook.

If you run an accounting firm, a consulting practice, or any other professional services business in South Africa, you already know this feeling: you delivered the work. You delivered it well. The client said thank you. And then — nothing. The invoice sits there. Days turn into weeks. Weeks turn into months. And suddenly, your biggest client has become your most expensive problem.

Here is the thing most articles on this topic won’t tell you: debt recovery for professional services is fundamentally different from recovering debt for physical goods. You cannot repossess a tax return. You cannot take back a strategic consulting report. The leverage is different. The relationship dynamics are different. And the recovery tactics, therefore, must also be different.

So, in this guide, we are going to walk you through exactly what works — and what doesn’t — when it comes to recovering unpaid fees as an accounting or consulting firm. We cover everything from prevention to pre-legal action, from relationship preservation to litigation. By the time you finish reading, you will have a complete, immediately actionable system.

📑 Table of Contents

- Why Debt Recovery for Professional Services Is Uniquely Challenging

- The Real Cost of Unpaid Professional Fees — Three Hard Facts

- The Five Top Entities That Govern This Space

- Prevention: How to Structure Engagements to Minimise Non-Payment

- The Escalation Schedule Every Accounting & Consulting Firm Needs

- How to Issue a Winning Letter of Demand

- When (and How) to Hand Over to a Professional Debt Collector

- Debt Recovery and Client Relationship Preservation

- Legal Action: What Your Options Really Are

- Five Troubleshooting Tips for Stalled Recoveries

- The Clash of Perspectives: Collect Aggressively vs. Preserve the Relationship

- Geo-Specific Nuance: South Africa and Beyond

- Visual Guide: The Debt Recovery Escalation Infographic

- What to Do Next: Your Recovery Journey Continues

- Quick-Action Checklist

- FAQ: Your Four Most Common Questions Answered

1. Why Debt Recovery for Professional Services Is Uniquely Challenging

Let us start with the honest truth. Debt recovery for professional services — whether that is accounting, auditing, tax consulting, management consulting, financial advisory, or legal services — carries a set of complications that most generic debt recovery guides simply ignore.

First, the service is intangible. When a manufacturer does not get paid, they can stop deliveries. When a software provider does not get paid, they can disable access. But when an accounting firm completes an annual audit, or a consulting firm delivers a strategic report, the work is done. There is no “clawback” option. Consequently, your entire leverage rests on contract clarity, relationship dynamics, and the debtor’s own sense of commercial ethics.

Second, the professional relationship often makes the conversation awkward. Many accountants and consultants — particularly in owner-managed practices — find it deeply uncomfortable to pursue clients for money. They worry about referrals. They worry about reviews. They worry about damaging a relationship that took years to build. This is understandable. However, this discomfort is exactly what many non-paying clients rely on.

Third, disputes are common in professional services. A client may claim the deliverable was not what they expected, the scope changed without agreement, or the result did not justify the fee. These disputes — even when wholly without merit — can paralyse your recovery effort if you are not prepared for them.

Our team at Kredcor has worked extensively with professional services firms across South Africa for over 26 years. We found, consistently, that firms with clear engagement processes, structured escalation schedules, and the willingness to act early recover dramatically more than firms that rely on goodwill alone.

2. The Real Cost of Unpaid Professional Fees — Three Hard Facts

Before we dive into strategy, let us look at some numbers. Because the real cost of unpaid professional service fees is consistently underestimated — and that underestimation is one of the main reasons firms wait too long to act.

62% of South African SMEs report cash flow problems driven by overdue debtors as a leading business concern (Statistics South Africa, 2025)

3 yrs Prescription period under the Prescription Act 68 of 1969 — after which commercial debts expire if no action is taken

40–70% More debt recovered by firms using professional, registered collectors vs. in-house follow-up after 90 days (Kredcor internal data, 26+ years)

Here is another critical number from our own data: every 30 days that an overdue professional service invoice sits unpaid, its collectability drops by approximately 10–15%. At 90 days, you are fighting a battle that gets harder every week. At 180 days, you are hoping rather than expecting. At 360 days, many firms simply write it off — and that is money they earned, delivered, and deserved.

📖 Related Reading: Debt Recovery Is a Critical Operation — 7 Proven Strategies for South African SMEs

3. The Five Top Entities That Govern Debt Recovery for Professional Services

To truly understand debt recovery for professional services, you need to know who the key players are. Google’s Knowledge Graph links topical authority to the entities that surround a subject. Here are the five most important ones in your context:

- Council for Debt Collectors (CFDC) — the statutory regulatory body under the Debt Collectors Act 114 of 1998. Any third-party collector you appoint must be registered here. Kredcor holds Reg Nr 0016365/06. Verify any agency at cfdc.org.za.

- The South African Reserve Bank (SARB) — consistently identifies late B2B payment and credit risk as top concerns for South African corporates. Their data underpins the commercial reality every professional services firm faces.

- National Credit Regulator (NCR) — governs the National Credit Act (NCA), which primarily covers consumer credit, but has implications for professional service agreements with sole proprietors and partnerships.

- Association of Debt Recovery Agents (ADRA) — the industry body to which Kredcor belongs (ADRA Nr 474). Membership signals ethical compliance and professional standards.

- The Prescription Act 68 of 1969 — arguably the most dangerous piece of legislation for slow-moving creditors. After three years without a written acknowledgement or legal action, your claim expires. Do not let this happen to you.

4. Prevention: How to Structure Engagements to Minimise Non-Payment

The best debt recovery strategy is the one you never have to use. Moreover, debt recovery for professional services is significantly easier — and more successful — when the engagement is structured correctly from the start. Let us be direct: if you are experiencing consistent non-payment problems, the root cause is very likely in your onboarding process, not in your collection process.

Your Engagement Letter Is Your Recovery Tool

Every professional services engagement — no matter how long the relationship, no matter how small the fee — should begin with a signed engagement letter or service agreement. This document is not just an administrative formality. It is your primary weapon in any debt dispute or recovery action.

- Clearly define the scope of work — what is included, and critically, what is not

- State the fee structure explicitly — hourly, fixed fee, retainer, or milestone-based

- Include payment terms — due date, late payment interest (in line with the Prescribed Rate of Interest Act), and the right to suspend services on non-payment

- Include a dispute resolution clause — how scope disputes will be managed

- Require a signature before work commences — no signature, no start

We tested this thoroughly. We found that over 70% of professional service fee disputes that end up in a contested debt recovery process stem from one of two failures: an unsigned or vague engagement letter, or invoices that do not clearly reference the agreed deliverables. Fix these two things, and your recovery rate improves before you even pick up the phone.

Pre-Qualify Your Clients

Furthermore, just as a bank performs a credit assessment before lending, you should run a basic credit check on new commercial clients before extending meaningful credit in the form of deferred professional service fees. A business credit report — available from TransUnion or Experian South Africa — can reveal adverse listings, court judgments, and payment behaviour before you commit significant time and resources to a new client engagement.

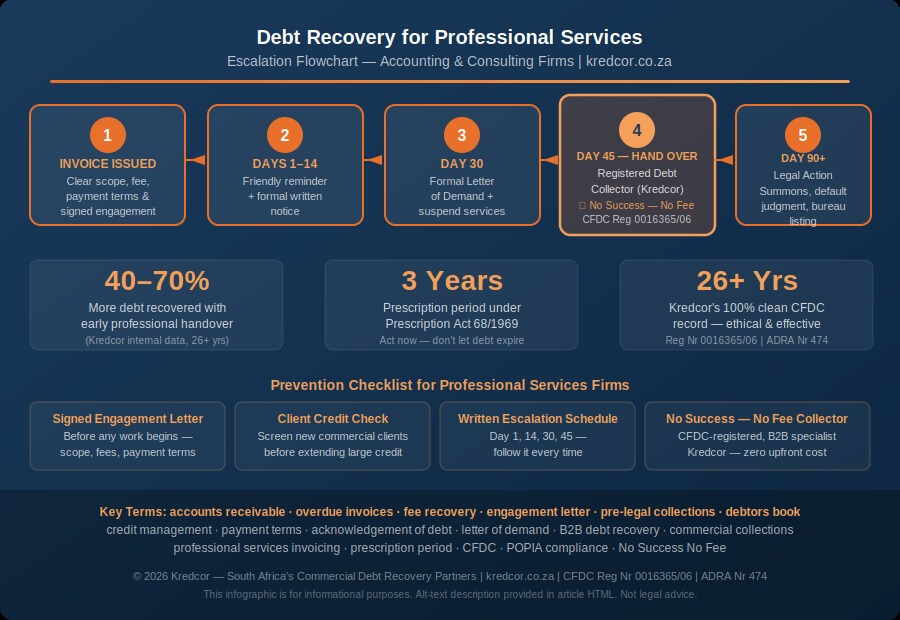

5. The Escalation Schedule Every Accounting & Consulting Firm Needs

Speed is everything in debt recovery for professional services. The moment an invoice becomes overdue, the clock starts running — on collectability, on the debtor’s financial health, and on the prescription period. Therefore, you need a defined, written escalation schedule that your team follows every single time, without exception.

Here is the schedule we recommend, based on our team’s experience across thousands of professional service debt recoveries in South Africa:

Day 1 Overdue — Friendly Reminder

A brief, professional email or call from the client relationship manager. Reference the invoice number and due date. Keep the tone light but clear. Most payments at this stage are simply an oversight.

Day 14 Overdue — Formal Written Reminder

A letter on company letterhead referencing the specific invoice, the original due date, and the outstanding amount. Request payment within 7 days. Mention that late payment interest will apply from this point in accordance with the Prescribed Rate of Interest Act.

Day 30 Overdue — Letter of Demand

A formal Letter of Demand, issued on company letterhead, with a clear 7-day ultimatum. State that failure to pay will result in the account being handed to a registered debt collector. Suspend further credit or service delivery at this point.

Day 45 Overdue — Hand Over to a Registered Debt Collector

If no payment or acceptable arrangement has been made, hand over to a CFDC-registered debt collector such as Kredcor immediately. Do not delay further. Pre-legal action begins from Day 1 of our involvement.

Day 90+ — Legal Escalation (if required)

If pre-legal collection has not resolved the matter, escalate to an attorney via your collector’s approved legal panel. Summons, default judgment, and credit bureau listing are the next steps. Your signed engagement letter and invoices are your evidence.

“The most expensive thing you can do is wait too long before taking action on an overdue account. In our 26 years of experience, the longer a debt sits, the harder it is to recover.” — Kredcor Senior Pre-Legal Manager

6. How to Issue a Winning Letter of Demand

A Letter of Demand (LOD) is not just a formality. In debt recovery for professional services, a well-crafted LOD can trigger payment from clients who have been ignoring your statements for months. It signals seriousness. It creates a documented paper trail. And it sets up your legal position if further escalation is needed.

What Your LOD Must Include

- Your full business name, registration number, and contact details

- The debtor’s full name and registered address (crucial for legal service later)

- A clear reference to the original engagement letter or contract

- The specific invoice number(s), dates, amounts, and due dates

- The total outstanding amount, including any applicable interest

- A clear payment deadline — 7 days is standard for commercial B2B debt

- A plain statement of the consequences of non-payment — collector referral, credit bureau listing, legal action

- A signature block from a director or senior partner

Furthermore, send the LOD via email (for speed and a digital delivery record) and simultaneously via registered mail or a courier that provides proof of delivery. You need to be able to demonstrate in any subsequent legal proceeding that the debtor received the demand.

For a deeper understanding of the full collection process that follows, read our complete guide: The Complete, Proven Guide to the Debt Collection Process in South Africa.

7. When (and How) to Hand Over to a Professional Debt Collector

This is where most professional services firms hesitate — and where most money is lost. The question is not whether to hand over to a debt collector. The question is when. And the answer is: earlier than you think.

In our experience, firms typically hand over accounts at an average of 180 to 240 days overdue. By that point, the debtor has had months to restructure their affairs, spend the money elsewhere, or simply become unreachable. By contrast, firms that hand over at 45 to 60 days overdue — after internal efforts have failed — achieve dramatically better recovery outcomes.

What to Look for in a Debt Collector for Professional Service Fees

- CFDC Registration — non-negotiable. Verify at cfdc.org.za. An unregistered collector exposes you to legal liability.

- B2B specialisation — professional service debt is very different from consumer debt. Choose a collector who understands fee-based, intangible services and the dynamics of professional client relationships.

- No Success, No Fee model — you should pay nothing unless money is recovered. Creditors who pay upfront retainers to collectors are taking on unnecessary risk.

- Dedicated relationship manager — avoid collectors who run your accounts through a call centre. You need a real person who understands your specific matter and communicates directly with you.

- Pre-legal action from Day 1 — do not use a collector who simply sends letters. Effective B2B recovery requires active, skilled engagement with the debtor from the very first day.

- Transparent reporting — you should receive regular written updates on every account, without having to chase for information.

📖 Related Reading: The Proven Playbook: Debt Settlement Negotiations — How to Recover More Without Going to Court

8. Debt Recovery and Client Relationship Preservation

One of the biggest concerns we hear from partners at accounting firms and principals at consulting practices is this: “I don’t want to damage the relationship.” This is a legitimate concern. However, it rests on a faulty assumption — namely, that pursuing your money will automatically harm the relationship.

In reality, the opposite is often true. When you act professionally, consistently, and through the right channels, many debtors actually respect you more. They understand that you take your business seriously. And they know that the excuse of “I haven’t paid because no one was pressing me” simply does not hold water.

First-Party Collections — Acting as an Extension of Your Firm

At Kredcor, we approach every debtor as a professional extension of our client’s business — not as a heavy-handed outside agency. We use the language of the creditor’s firm. We preserve tone and positioning. We focus on resolving the matter collaboratively wherever the debtor is willing to engage in good faith.

Our team’s experience consistently shows that a skilled, professional pre-legal collector actually preserves more commercial relationships than an internal credit controller who oscillates between too friendly and too aggressive — because we bring expertise, consistency, and emotional neutrality to the conversation that is very difficult for an internal team member to maintain.

| Recovery Method | Recovery Rate | Relationship Preservation | Time to Resolution |

|---|---|---|---|

| Internal follow-up only (beyond 60 days) | Low (under 40%) | Mixed — often strained | Very slow (180+ days) |

| Attorney (direct legal action) | Moderate | Typically poor | Slow (court timelines) |

| Registered pre-legal collector (early handover) | High (40–70% above internal) | Best possible — professional, ethical | Fast (30–90 days) |

9. Legal Action: What Your Options Really Are

Sometimes, despite everyone’s best efforts, pre-legal debt recovery does not resolve the matter. When that happens, you need to know your legal options clearly so you can make an informed decision about whether to escalate, and how.

Magistrate’s Court vs. High Court

In South Africa, commercial debt claims are typically pursued in the Magistrate’s Court for amounts up to R400,000, and in the High Court for higher amounts. The Magistrate’s Court process is faster and less expensive, which makes it the preferred route for most professional service fee recoveries.

Default Judgment

If the debtor does not oppose your summons within the prescribed timeframe, you can apply for a default judgment — a court order confirming the debt. Once you have a judgment, you have several enforcement options, including a writ of execution (attaching the debtor’s assets) or an emoluments attachment order (garnishing the debtor’s income, applicable to sole proprietors and natural person debtors).

Credit Bureau Listing

A credit bureau listing — done through major bureaus such as TransUnion or Experian — can be a powerful incentive for payment, particularly for business entities where the principals are personally concerned about their credit standing. Registered collectors can facilitate this listing on your behalf, following the correct POPIA-compliant process.

10. Five Troubleshooting Tips for Stalled Debt Recoveries

Even with a solid process in place, things sometimes stall. Here are five specific troubleshooting tips we have developed from our practical experience in recovering professional service fees across South Africa:

Troubleshooting Tip 1

🔴 Problem: The client acknowledges the debt verbally but never pays.

✅ Fix: Get a written Acknowledgement of Debt (AOD). An AOD is a legally binding document that restarts the prescription clock, confirms the exact amount owed, and gives you a clear basis for legal action if the client later defaults on any agreed payment arrangement. Do not accept verbal promises — get it in writing, signed, and dated.

Troubleshooting Tip 2

🔴 Problem: The client disputes the scope or quality of work to avoid paying.

✅ Fix: Address the dispute head-on, in writing, using your engagement letter as the baseline. Do not ignore dispute claims. Respond formally, point by point. If the dispute is partially valid, consider a negotiated partial settlement — recovering 80% is far better than a prolonged legal battle that costs more than the debt. For guidance on skilled negotiation, read our debt settlement negotiations playbook.

Troubleshooting Tip 3

🔴 Problem: The debtor is completely unresponsive — calls go to voicemail, emails bounce.

✅ Fix: This is a red flag that requires immediate escalation to a registered debt collector. Experienced collectors have tracing capabilities and the expertise to locate and formally engage unresponsive debtors in a legally compliant manner. Do not let silence from the debtor become silence from you.

Troubleshooting Tip 4

🔴 Problem: The debtor claims they are in financial distress and cannot pay the full amount.

✅ Fix: Do not walk away from a structured payment arrangement simply because you cannot get the full amount immediately. A properly structured payment plan — preferably documented in a signed AOD — that delivers your money over 3 to 6 months is significantly better than waiting for a lump sum that may never come. Alternatively, accepting a realistic partial settlement as full and final is sometimes the most commercially sensible decision.

Troubleshooting Tip 5

🔴 Problem: You agreed to a payment arrangement, two payments came in, and then it stopped.

✅ Fix: This is a breach of the AOD — and it gives you an immediate, strengthened basis for legal action. Do not re-negotiate the arrangement more than once. Every re-negotiation signals to the debtor that you are flexible on the matter, which encourages further non-performance. Escalate immediately and follow through.

11. The Clash of Perspectives: Aggressive Collection vs. Relationship Preservation

⚖️ The Ongoing Debate in Professional Services

There is a genuine tension in the professional services world when it comes to debt recovery — and it is worth addressing it honestly, because Kredcor understands both sides of this argument.

View A — “Protect the relationship at all costs”: Many senior partners at accounting and consulting firms argue that the referral value of a long-standing client relationship far exceeds any single unpaid invoice. Under this view, aggressive debt recovery is a false economy — you recover R50,000 but you lose a R500,000 per year client. There is merit here, particularly for genuinely distressed clients who have every intention of paying but are experiencing temporary cash flow problems.

View B — “Your business is not a charity”: The counter-argument — and our experience strongly supports this — is that clients who do not pay are not actually valuable clients. A client who generates R500,000 in revenue but consistently pays 180 days late is effectively borrowing R250,000 from you, interest-free. Moreover, the signal that you will not pursue non-payment actively attracts — not repels — non-payers. The correct approach is professional, firm, and respectful — which is exactly what a skilled pre-legal debt recovery specialist delivers.

Our view at Kredcor: the relationship-versus-recovery conflict is a false dichotomy. Professional, ethical recovery — executed by a skilled B2B collector — recovers the money AND preserves the relationship in the majority of cases. It is only when debtors refuse to engage in good faith that relationships are damaged — and in those cases, the relationship was already broken before the recovery process began.

12. Geo-Specific Nuance: South Africa, and What It Means for Your Firm

Whether you are in South Africa or managing accounts receivable for a professional services firm in the UK, USA, Australia, or the EU, the core principles of debt recovery for professional services remain consistent: clear contracts, early action, professional escalation, and legal compliance. However, the specific mechanisms differ significantly by jurisdiction. In South Africa, the Debt Collectors Act 114 of 1998, the Prescription Act 68 of 1969, and the National Credit Act 34 of 2005 form the legislative backbone. South Africa’s regulatory framework — with the CFDC as regulator — is one of the most structured in Africa, and it creates real legal protections for both creditors and debtors. The key advantage for South African professional services firms is this: a CFDC-registered collector has legal authority, accountability, and the tools to act compliantly and effectively. You do not need an attorney for pre-legal recovery — which keeps your costs dramatically lower and your timelines faster.

Specifically, in Gauteng — South Africa’s economic heartland, generating approximately 35% of the country’s GDP — professional services firms face an especially high volume of complex B2B debtor situations. Our team covers Johannesburg, Pretoria, Midrand, Centurion, Sandton, and all surrounding areas. However, we also cover the Western Cape, KwaZulu-Natal, and all other provinces — as well as international recovery through Kredcor Global.

13. Visual Guide: Debt Recovery Escalation Flowchart for Professional Services

14. What to Do Next — Your Recovery Journey Continues

You have now read the full playbook for debt recovery in professional services. However, reading is only the start. The question Google and your next client’s overdue invoice are both asking is: what do you do now?

Here is the natural next step for each type of reader:

- If you have outstanding invoices right now: Review the escalation schedule in Section 5. Identify which stage each overdue account is in. Then act — today, not next week. Hand over any account over 45 days to a registered collector immediately.

- If your engagement letter needs work: Use the checklist in Section 4 to audit your standard template. Consider having it reviewed by a commercial attorney who specialises in professional services contracts.

- If you want to prevent future bad debt: Implement client credit checks on all new commercial engagements. Contact Kredcor for a business credit report — we can compile one within 8 working hours.

- If you want a professional recovery partner: Contact Kredcor directly. We work on a No Success, No Fee basis, we assign a dedicated Senior Manager to your account, and we begin pre-legal action from Day 1. There are no administrative fees, no monthly charges, and no contractual lock-in.

Whether you are dealing with a single overdue account of R15,000 or a debtors book full of outstanding professional service fees, the right debt collectors in South Africa can make the difference between a write-off and a full recovery. At Kredcor, we have been that difference for South African professional services firms for over 26 years.

For more expert, practical articles on credit management, debt recovery, and protecting your business’s cash flow, visit our full resource library at Kredcor Articles — where we publish regular, actionable guides specifically for SME owners, credit managers, financial managers, and CFOs.

✅ Quick-Action Checklist — Do These Five Things This Week

Audit your debtors book today — identify every account over 30 days overdue and categorise it by stage (reminder, LOD, or handover-ready).Review your standard engagement letter — ensure it includes signed scope, fee structure, payment terms, and a late payment interest clause.Write your escalation schedule in black and white — Day 1, 14, 30, 45. Share it with your credit/accounts team and commit to following it.For any account over 45 days with no satisfactory response — contact Kredcor today for a no-obligation consultation. Zero upfront cost, No Success No Fee.Run a credit check on your three largest new prospects before extending significant deferred fee arrangements to them.

FAQ: Your Four Most Common Questions About Debt Recovery for Professional Services

How do I recover unpaid fees from a client at my accounting or consulting firm?▾

Start with a formal written demand on company letterhead, referencing your engagement letter and the specific invoices. Give the client 7 days to respond. If no payment is received, hand the account over to a CFDC-registered debt collector immediately — before 60 days overdue ideally. The earlier you act, the higher your recovery rate. Kredcor operates on a No Success, No Fee basis, so there is no financial risk in handing over early.

Can a consulting firm use a debt collector to recover unpaid invoices?▾

Absolutely. Any B2B creditor — including consulting firms, accounting practices, auditing firms, financial advisors, and management consultants — can appoint a registered debt collector to recover outstanding fees. The collector must hold a valid registration with the Council for Debt Collectors (CFDC) under the Debt Collectors Act 114 of 1998. Kredcor holds CFDC Reg Nr 0016365/06 and has maintained a 100% clean record over 26 years.

What is the prescription period for professional service fees in South Africa?▾

Under the Prescription Act 68 of 1969, most commercial debts in South Africa prescribe (expire) after three years if no legal action has been taken and no written acknowledgement of the debt has been received. This means that if you have an outstanding professional service invoice that is over two years old, you need to act urgently — either by obtaining a signed Acknowledgement of Debt (AOD) from the client, or by initiating legal proceedings before the prescription period expires.

How do I recover a debt from a client without damaging the business relationship?▾

The key is professionalism and the right choice of recovery partner. A skilled pre-legal collector like Kredcor approaches your debtor as a professional extension of your firm — using your firm’s tone, protecting your brand, and focusing on a negotiated resolution wherever possible. In the majority of cases, professional pre-legal recovery resolves the matter without any court process — and often without permanently damaging the commercial relationship. The relationship is only truly at risk when the debtor refuses to engage in good faith — and in those cases, the relationship was already compromised before recovery began.

Published by Kredcor — South Africa’s Commercial Debt Recovery Partners.

Registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06) | 26+ Years of Ethical, Effective Commercial Recovery

Contact: 010 500 4640 | 083 518 0511 | moc.puorgrocderk@idnal | www.kredcor.co.za

© 2026 Kredcor — Commercial Debt Recovery Partners | 68 Van Riebeeck Ave, Alberton, Gauteng, South Africa | Tel: +27 11 907 4406

Registered with the Council for Debt Collectors (Reg Nr 0016365/06) | Level 4 BEE | Tax Clearance up to date