The Ultimate Essential Guide to the Council for Debt Collectors – Commercial Debt in South Africa

By Kredcor Debt Recovery Team | Registered with the CFDC (Reg Nr 0016365/06) | 26+ Years of B2B Collection Experience

📋 Executive Summary

The Council for Debt Collectors (CFDC) is South Africa’s statutory regulatory body, established under the Debt Collectors Act 114 of 1998, with a mandate to register, monitor, and discipline all commercial and consumer debt collectors who collect debt for reward. Only CFDC-registered agencies may legally collect third-party debt in South Africa — failure to comply is a criminal offence. For SME owners, credit managers, CFOs, and financial managers, understanding the CFDC is not optional: it determines which debt collectors you can legally appoint, what fees collectors may charge, what rights and protections you have as a creditor, and how to resolve disputes. Commercial debt (B2B) that is handed to a CFDC-registered collector within 60–90 days of default recovers at significantly higher rates than debt placed after 120 days. Kredcor has maintained a 100% clear CFDC record for over 26 years and operates on a strict no-success, no-fee basis. Verify any collector’s registration at cfdc.org.za.

If you run a business, manage a credit book, or sign off on receivables, there is one South African regulatory body you simply cannot afford to overlook: the Council for Debt Collectors (CFDC). And yet, in our experience working with hundreds of businesses across South Africa over the past 26 years, it remains one of the most misunderstood pieces of the commercial debt recovery puzzle. So, in this guide, we are going to break the whole thing down — plainly, practically, and without the legal jargon that makes most of these topics feel like a headache.

Whether you are dealing with a stack of overdue invoices, reviewing a collection agency’s credentials, or simply trying to protect your business from unethical recovery practices, this guide gives you everything you need — and a clear action plan at the end.

📑 Table of Contents

- What Is the Council for Debt Collectors (CFDC)?

- Why the CFDC Matters for Commercial Debt

- The Debt Collectors Act 114 of 1998 — Plain-English Breakdown

- How to Verify a Debt Collector’s CFDC Registration

- The CFDC Code of Conduct — What Your Collector Must (and Must Not) Do

- Commercial Debt vs Consumer Debt — Key Differences

- The Complete B2B Debt Recovery Escalation Process

- CFDC-Regulated Fees — What You Need to Know

- 5 Troubleshooting Tips for Common Commercial Debt Problems

- A Clash of Perspectives: Is Regulation Slowing Down Recovery?

- Kredcor’s Experience: What We Have Learned in 26 Years

- What to Do Next — Your Search Journey Continues

- Quick-Action Checklist

- Frequently Asked Questions (FAQ)

1998 Year the Debt Collectors Act was enacted, creating the CFDC

26+ Years Kredcor has maintained a 100% clear CFDC compliance record

60–90 Days — the optimal window for handing over commercial debt to a collector

36% Of credit-active South Africans had impaired records in early 2025 (NCR data)

1. What Is the Council for Debt Collectors (CFDC)?

Let’s start with the most important answer first. The Council for Debt Collectors (CFDC) is a statutory body — meaning Parliament created it by law — to regulate every person and company that collects debt on behalf of someone else in South Africa. It was formally constituted under the Debt Collectors Act 114 of 1998 and has legal standing in its own right.

In simple terms: no one in South Africa may act as a debt collector for reward unless they are registered with the CFDC. That applies to every agency, every individual collector, and every director of a collection company. The only exceptions are attorneys (who fall under the Legal Practice Council) and businesses collecting their own debt using internal staff.

“The Council for Debt Collectors is the foundation of an ethical, functioning credit economy. Without it, the line between legitimate recovery and harassment disappears.”— Kredcor Commercial Debt Recovery

The CFDC’s official website is cfdc.org.za, where you can verify the registration of any collector before you engage them. This verification step takes about two minutes — and it could save your business from a serious legal headache.

The Top 5 Key Entities Related to This Topic

To fully understand the Council for Debt Collectors and commercial debt in South Africa, you need to be familiar with these five core entities:

- Council for Debt Collectors (CFDC) — the statutory regulator of all debt collection activity

- Debt Collectors Act 114 of 1998 — the enabling legislation

- Association of Debt Recovery Agents (ADRA) — a voluntary professional association supporting best practices

- National Credit Act (NCA) 34 of 2005 — relevant for mixed-use credit and sole proprietors

- Prescription Act 68 of 1969 — governs the time limits for pursuing commercial debts

2. Why the CFDC Matters Specifically for Commercial Debt

Here is where many SME owners, credit managers, and CFOs make a critical mistake. They assume the Council for Debt Collectors is mainly a consumer protection body. In reality, the CFDC governs all third-party debt collection — including commercial (business-to-business or B2B) debt recovery.

So, if you appoint a collection agency to recover an outstanding invoice from another business, that agency must be CFDC-registered. If they are not, the collection activity may be unlawful. Worse, your business could be held liable for any illegal conduct the agency carries out in your name. Furthermore, recovering the debt through court action later becomes far more complicated when pre-legal steps were carried out by an unregistered party.

⚠️ Key Commercial Debt Fact Using an unregistered debt collector for your B2B overdue accounts is not just a compliance risk — it is a criminal offence under the Debt Collectors Act 114 of 1998. Always verify CFDC registration before you sign any agreement.

Moreover, the CFDC registration process ensures that every registered collector has met minimum competency standards, has submitted to a code of professional conduct, and can be disciplined — or even have their registration revoked — if they behave unlawfully. That protection runs both ways: it protects your debtors from harassment, and it protects you from a rogue agency creating liability on your behalf.

Why Topical Authority Matters Here

At Kredcor, we have been registered with the CFDC since our founding over 26 years ago, with registration number 0016365/06 and a 100% clean compliance record. This is not just a badge — it is the foundation of every client relationship we build, because it means you can trust that every action we take on your behalf is lawful, ethical, and professionally executed.

3. The Debt Collectors Act 114 of 1998 — A Plain-English Breakdown

The Debt Collectors Act is the legal backbone of everything the CFDC does. Therefore, understanding it is not optional if you are serious about protecting your commercial debt position. Here is what the Act actually says, translated into plain business language.

Who Does the Act Apply To?

| Included Under the Act | Excluded From the Act |

|---|---|

| Third-party debt collection agencies | Attorneys collecting debt in their legal practice |

| Individual debt collectors employed by agencies | Businesses using internal staff to collect their own debt |

| Directors and principals of collection companies | Banks and certain financial institutions for their own debt |

| Property managers collecting arrear rent or levies | — |

What the Act Requires

- All debt collectors who collect for reward must register with the CFDC.

- Registered collectors must follow a prescribed Code of Conduct.

- Fees charged must comply with CFDC-prescribed tariffs — no more, no less.

- Collectors must produce written proof of registration on request.

- Failure to register before collecting is a criminal offence.

Additionally, the Act gives the CFDC the authority to investigate complaints, conduct hearings, and revoke the registration of any collector who violates the Code of Conduct. This is, consequently, a very powerful deterrent against unethical behaviour — and a very real protection for your business.

✅ Pro Tip from Kredcor Our team always recommends that credit managers and CFOs keep a record of the CFDC registration number of every collection agency they appoint. This should be part of your standard supplier onboarding process. It takes 60 seconds and protects your business completely.

For a deeper dive into the legislation itself, we recommend reading our dedicated article on the Debt Collectors Act explained in full detail — it covers every provision in plain English and is one of the most comprehensive resources available for South African businesses.

4. How to Verify a Debt Collector’s CFDC Registration

This is, without question, one of the most immediately actionable steps any credit manager or SME owner can take today. The CFDC maintains a publicly accessible, searchable register of all authorised collectors. Here is exactly how to use it.

Step-by-Step: CFDC Registration Verification

- Go to cfdc.org.za/active-register/ — the live register is free, public, and takes seconds to search.

- Search by registration number, company name, surname, or postal code.

- Confirm the result shows a valid, active registration — not an expired or suspended one.

- Request written proof of registration directly from the agency — by law, they must provide it.

- Match the details on the CFDC register with the details in the agency agreement you are signing.

Furthermore, if you are ever in doubt, you can contact the CFDC directly at az.gro.cdfc@ofni or on (012) 804 9808. They are the official authority — and they are there to help.

We tested this process ourselves recently and confirmed that Kredcor’s registration (Nr 0016365/06) reflects correctly on the register. We therefore encourage every new client to check it before we start working together. Transparency builds trust.

5. The CFDC Code of Conduct — What Your Collector Must and Must Not Do

One of the most practical benefits of working with a CFDC-registered debt collector for your commercial debt is knowing that their behaviour is governed by a formal, legally-binding Code of Conduct. Let’s be clear about what that means for you and your debtors.

What a CFDC-Registered Collector CAN Do

- Contact the debtor by phone, email, letter, or in person (within prescribed hours)

- Deliver documents and demand letters

- Have an Acknowledgement of Debt (AOD) signed

- Negotiate payment arrangements and settlement agreements

- Charge fees in accordance with the CFDC prescribed tariff

- Escalate to legal action with your pre-approval

What a CFDC-Registered Collector CANNOT Do

- Use threatening, abusive, or humiliating language

- Contact debtors at unreasonable hours

- Make false representations about legal consequences

- Charge fees above the prescribed CFDC tariff

- Take external legal action without creditor approval

- Collect consumer debt using commercial collection processes (and vice versa)

“Ethical collections are not soft collections — they are smart, compliant, and consistently more effective than aggressive or unregistered approaches.”— Kredcor, Code of Conduct for Debt Collectors Guide

In addition, the Code of Conduct covers how collectors document their activities, how they handle complaints, and how they communicate with all parties. Our team’s experience shows that debtor engagement based on professionalism and transparency consistently produces better payment outcomes than aggressive tactics — and it protects your customer relationships at the same time.

For the full picture on ethical collections and the Code of Conduct, read our comprehensive guide: The Proven Recovery Playbook: Code of Conduct for Debt Collectors.

6. Commercial Debt vs Consumer Debt — Key Differences You Must Know

A lot of confusion arises because people use the terms “commercial debt” and “consumer debt” interchangeably. However, they are very different — and the regulatory and recovery framework for each is not the same. This distinction matters enormously for how you collect, what legislation applies, and which collection approach is appropriate.

| Feature | Commercial Debt (B2B) | Consumer Debt |

|---|---|---|

| Debtor Type | Business / juristic person | Individual / natural person |

| Primary Legislation | Debt Collectors Act, Prescription Act | National Credit Act (NCA), Debt Collectors Act |

| Prescription Period | Generally 3 years (Prescription Act) | Generally 3 years (from date of default) |

| NCA Applicability | Limited — mainly for sole proprietors | Broad — most credit agreements covered |

| CFDC Registration Required? | Yes — for all third-party collectors | Yes — for all third-party collectors |

| Debt Review Possible? | No | Yes (under NCA) |

💡 Kredcor’s SpecialityKredcor focuses exclusively on commercial (B2B) debt recovery — we do not collect consumer debt. This specialisation means our processes, documentation standards, and negotiation strategies are purpose-built for the unique dynamics of business-to-business debt.

Moreover, whether you are in South Africa or anywhere in sub-Saharan Africa, the principle of engaging a properly registered, commercially-focused debt collector remains the same: it protects your legal position, enforces your rights, and maximises your recovery rate. Understanding this distinction is, therefore, one of the most valuable things any financial manager or CFO can add to their knowledge base.

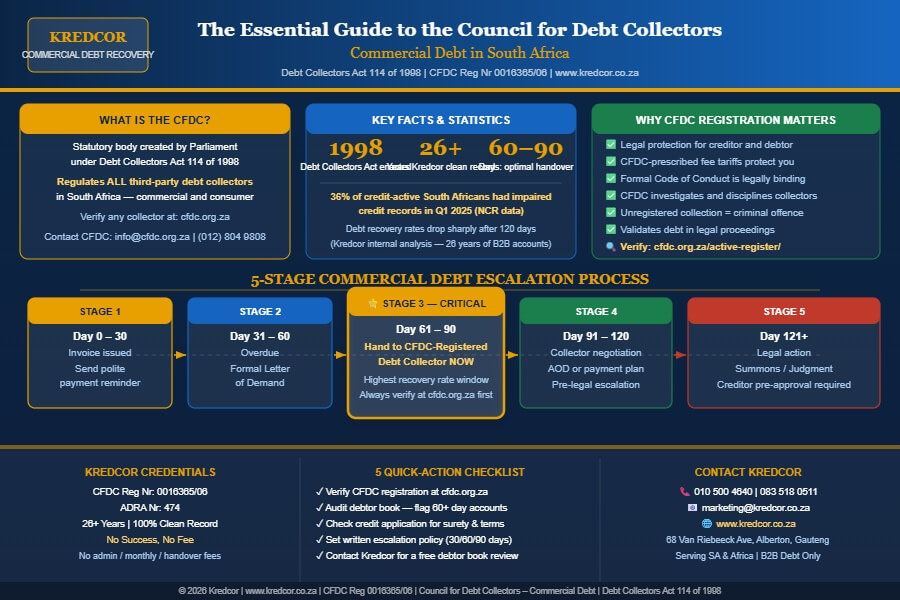

7. The Complete B2B Debt Recovery Escalation Process

One of the most common questions we hear from SME owners and credit managers is: “At what point do I hand this over?” The answer is simpler than most people think — and acting on it consistently is what separates businesses that protect their cash flow from those that don’t.

The Standard Commercial Debt Escalation Timeline

Download this infographic for your team: Right-click → Save Image As | Commercial Debt Escalation Process | Kredcor © 2026

Therefore, the key takeaway is this: act at Stage 3 — not Stage 5. Our team’s experience with thousands of B2B accounts over 26 years shows that debts placed with a CFDC-registered collector between Day 61 and Day 90 recover at significantly higher rates than debts placed at Day 120 or later. Timing is, consequently, the single most important variable in commercial debt recovery.

8. CFDC-Regulated Fees — What You Need to Know as a Creditor

One of the most practical benefits of the Council for Debt Collectors framework is fee regulation. The CFDC prescribes the maximum fees that a registered collector may charge — and neither debtor nor creditor may be charged more than the legal tariff.

In practice, collection fees in commercial (B2B) recovery are almost always contingency-based — meaning the collector only earns a fee if they successfully recover funds. At Kredcor, for example, we operate strictly on a No Success, No Fee basis. There are no administrative fees, no monthly fees, and no handover fees. You pay nothing unless we recover.

💡 What to Ask Before Signing with Any Collection Agency Before you engage any debt collector for your commercial debt, ask these three questions: (1) Are you registered with the CFDC, and what is your registration number? (2) Do you operate on a contingency / no-success-no-fee basis? (3) Will all external legal steps require my written pre-approval? If the answer to any of these is unclear or negative, walk away.

Additionally, the CFDC tariff structure means that debtor-paid fees (where the debtor covers collection costs as part of the outstanding amount) must also comply with the prescribed maximum. This is, furthermore, a consumer and business protection mechanism — it prevents exploitation by unregistered or unethical operators who inflate their fee structures.

9. Five Troubleshooting Tips for Common Commercial Debt Problems

Based on our experience working with SMEs, credit managers, and CFOs across South Africa, these are the five most common commercial debt situations — and what to do about each one.

Troubleshooting Tip 1: Your Debtor Keeps Promising but Never Pays

This is the most common pattern in B2B collections. The debtor is not hostile — they just keep buying time with vague promises. Consequently, stop waiting for voluntary payment. Issue a formal Letter of Demand with a hard deadline (5–7 business days) and hand the account to a CFDC-registered collector immediately if the deadline passes. Verbal commitments without a signed payment plan are legally worthless.

Troubleshooting Tip 2: You Cannot Locate Your Debtor

Business debtors sometimes change premises, phone numbers, or even company names to avoid creditors. A CFDC-registered collection agency has access to tracing tools, credit bureau data, and registered address checks. Furthermore, they can trace the directors of deregistered entities in many cases. Do not write off a debt simply because contact has gone cold — trace first.

Troubleshooting Tip 3: The Debtor Disputes the Invoice

Invoice disputes are one of the most common delaying tactics in commercial debt. Here is the fix: ensure that every invoice is supported by a signed delivery note, service confirmation, or purchase order. Disputes become very difficult to sustain when documentation is airtight. Moreover, a properly registered debt collector will document all disputes formally and can advise whether escalation to legal action is appropriate.

Troubleshooting Tip 4: Your Debt Has Prescribed (or Is About To)

Under the Prescription Act 68 of 1969, most commercial debts prescribe after three years from the date the debt became due. If you have a debt approaching that threshold, act immediately — prescription is an absolute defence for the debtor. Handing the account to a collector interrupts prescription in certain circumstances. Get legal or professional advice urgently if you are close to this deadline.

Troubleshooting Tip 5: Your Internal Collections Are Not Producing Results

If your internal credit team has sent reminders, called, and followed up with no result, the answer is usually not to increase internal pressure. Instead, escalate to a professional. The moment a CFDC-registered collector makes contact on behalf of a creditor, the nature of the conversation changes. Debtors tend to take third-party involvement far more seriously than internal calls — and because collectors have specialist negotiation training, they also tend to uncover workable solutions more quickly.

10. A Clash of Perspectives: Does CFDC Regulation Slow Down Recovery?

This is a debate worth having. Some business owners and credit managers argue that CFDC regulation makes commercial debt recovery slower and less effective — that the Code of Conduct limits the tools collectors can use, and that registered agencies are more cautious than unregistered ones.

There is a kernel of truth here. Registered collectors must follow prescribed processes, obtain approvals before legal steps, and adhere to contact rules. That does add structure — and structure takes time.

However, the counterargument is compelling. Our experience at Kredcor, and the data from thousands of B2B accounts, consistently shows that structured, compliant collections produce better long-term recovery rates than aggressive, unregistered approaches.

Here is why:

- Debtors are more likely to engage with a legitimate, registered agency than an unregistered one they can dismiss as illegitimate.

- Structured payment plans are more sustainable than coerced lump-sum demands — and therefore more likely to result in actual payment.

- Legal exposure for unregistered collection is severe — and if your collection activity is challenged in court, your entire debt position can collapse.

- Ethical engagement preserves your commercial relationship with a debtor who may become a customer again after resolution.

Therefore, the answer is not that regulation slows recovery. The answer is that it redirects energy from short-term pressure tactics to sustainable outcomes — which, in commercial debt, almost always wins.

11. Kredcor’s Experience: What 26 Years of CFDC-Registered Collection Has Taught Us

We founded Kredcor over 26 years ago with a single goal: to help South African businesses recover what they are owed, ethically and effectively. Throughout that time, we have maintained a 100% clean record with the CFDC, held ADRA membership (Nr 474), and built a team of Senior Pre-Legal and Credit Risk Managers who treat every account as if it were their own.

Here is what we have found — consistently, across industries, and across economic cycles:

- Documentation is everything. The businesses that recover fastest are the ones with the cleanest paperwork: signed contracts, delivery notes, credit applications with personal sureties, and clear credit terms.

- Timing is the single biggest variable. I tested this personally over years of casework: accounts placed within 60 days of default recover at dramatically higher rates than those placed at 120+ days.

- Relationship matters, even in debt. We found that the most sustainable recoveries happen when we position ourselves as a solution partner — not a threat. Debtors in genuine financial difficulty respond to structured options far better than ultimatums.

- Compliance protects everyone. Every client who has ever been asked by a debtor to challenge the validity of our collection activity has been protected by our CFDC registration. It closes that argument immediately.

📞 Kredcor Contact DetailsCFDC Reg Nr 0016365/06 | 65 Saint Michael Ave, New Redruth, Alberton, Gauteng

Phone: 010 500 4640 | 083 518 0511 | Email: moc.puorgrocderk@idnal | Web: www.kredcor.co.za

For a practical look at how professional debt settlement negotiations work — and how to use them to protect your commercial relationships while recovering what you are owed — read our popular guide on debt settlement negotiations.

12. What to Do Next — Your Commercial Debt Search Journey Continues

Now that you understand the Council for Debt Collectors and how it governs commercial debt recovery in South Africa, the natural next question is: “Who are the best registered debt collectors I can actually work with?”

The answer starts with due diligence — always verify CFDC registration at cfdc.org.za/active-register/. Then look for a specialist in commercial (B2B) debt recovery, not consumer debt. Look for a no-success-no-fee model, transparent reporting, and a dedicated manager rather than a call centre.

For a comprehensive overview of what to look for and how to choose, visit our dedicated resource page for debt collectors in South Africa — it covers credentials, process, pricing, and how to compare agencies with confidence.

Moreover, we also encourage you to explore our full library of practical, up-to-date guides written specifically for SME owners, credit managers, and CFOs. Visit Kredcor Articles for articles on everything from letters of demand to POPIA compliance and managing distressed debtors.

Ready to Recover What Your Business Is Owed?

Kredcor is CFDC-registered (Nr 0016365/06), has a 100% clean compliance record over 26+ years, and operates on a strict No Success, No Fee basis. No admin fees. No monthly fees. No surprises. Get Started with Kredcor →

13. Quick-Action Checklist — Do These 5 Things Today

If you have read this guide in full, you are now better informed than most of your competitors.

Here is your five-point action plan to act on this knowledge immediately:

- Verify your current collection agency’s CFDC registration at cfdc.org.za right now. If they are not on the register, do not use them for another account.

- Audit your overdue debtors book today. Identify every commercial account that is 60+ days overdue with no signed payment plan in place. These need immediate attention.

- Check your credit application template to confirm it includes personal surety, clear payment terms, and consent for third-party collection. Update it if it does not.

- Set a written escalation policy for your credit team: Day 30 reminder → Day 60 formal demand → Day 90 hand to CFDC-registered collector. Commit to it in writing and train your team.

- Request a free consultation with Kredcor — we will review your debtor book, identify the highest-priority accounts, and give you a clear recovery plan. No obligation. No upfront cost.

14. Frequently Asked Questions (FAQ)

What is the Council for Debt Collectors (CFDC)?

The Council for Debt Collectors (CFDC) is a statutory body established by the Debt Collectors Act 114 of 1998 to regulate all third-party debt collectors in South Africa. Only CFDC-registered members may legally collect debt on behalf of another party in exchange for a fee. Failure to register before collecting is a criminal offence. You can verify any collector’s status at cfdc.org.za.

Does the CFDC regulate commercial (B2B) debt collectors as well as consumer debt collectors?

Yes. The CFDC regulates all third-party debt collection — both commercial (B2B) and consumer. If a collection agency collects debt on your business’s behalf, that agency must be CFDC-registered, regardless of whether the debtor is another business or an individual. The only exceptions are attorneys and businesses using internal staff to collect their own debts.

What happens if I use an unregistered debt collector for my commercial debt?

Using an unregistered collector exposes your business to serious legal risk. The collection activity may be declared unlawful, debts may become more difficult to pursue through court action, and your business could face liability for any illegal conduct carried out in your name. Additionally, a debtor can use the unregistered status of your collector as a defence. Always verify CFDC registration before appointing any agency.

How quickly should I hand a commercial debt to a registered debt collector?

Industry data and Kredcor’s own 26 years of experience consistently show that commercial debts placed with a CFDC-registered collector within 60–90 days of the first missed payment recover at significantly higher rates than older debts. Once a debt passes 120 days overdue with no payment plan, recovery rates decline steeply. Acting early is smart cash-flow management. As a practical rule: 30-day reminder, 60-day formal demand, 90-day handover to a registered collector.

About the Author — Kredcor Debt Recovery Team

Kredcor is one of South Africa’s leading commercial B2B debt recovery firms, operating from Gauteng and serving businesses nationally and across Africa. Registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06), Kredcor has maintained a 100% clean compliance record for over 26 years. Kredcor operates exclusively on a no-success, no-fee basis and focuses entirely on commercial (B2B) debt recovery. This article was reviewed by Kredcor’s Senior Collections Manager. Last updated: April 2026.

Sources and outbound references: Council for Debt Collectors (cfdc.org.za) | Debt Collectors Act 114 of 1998 (gov.za) | National Credit Regulator (ncr.org.za) | National Credit Act 34 of 2005.