Powerful Start: How to Get Started With the Debt Collection Process in South Africa — 9 Practical Steps for SMEs

Executive Summary:

The debt collection process in South Africa starts long before court papers. For SMEs, credit managers, financial managers and CFOs, the smartest starting point is to confirm the debt, gather the contract and invoice trail, check whether the debt has prescribed, decide whether the National Credit Act applies, and then escalate in a disciplined sequence: reminder, formal demand, payment arrangement or Acknowledgement of Debt, handover to a registered debt collector or attorney, and finally summons and enforcement where necessary. In South Africa, court choice matters, timing matters, and paperwork matters even more. A Small Claims Court matter is capped at R20 000 and only natural persons may institute claims there, while magistrates’ courts handle larger commercial claims. Registered debt collectors must appear on the Council for Debt Collectors register. This guide explains the exact starting steps, common mistakes, legal triggers, troubleshooting tips and what to do next so your team can recover cash faster and reduce credit risk.

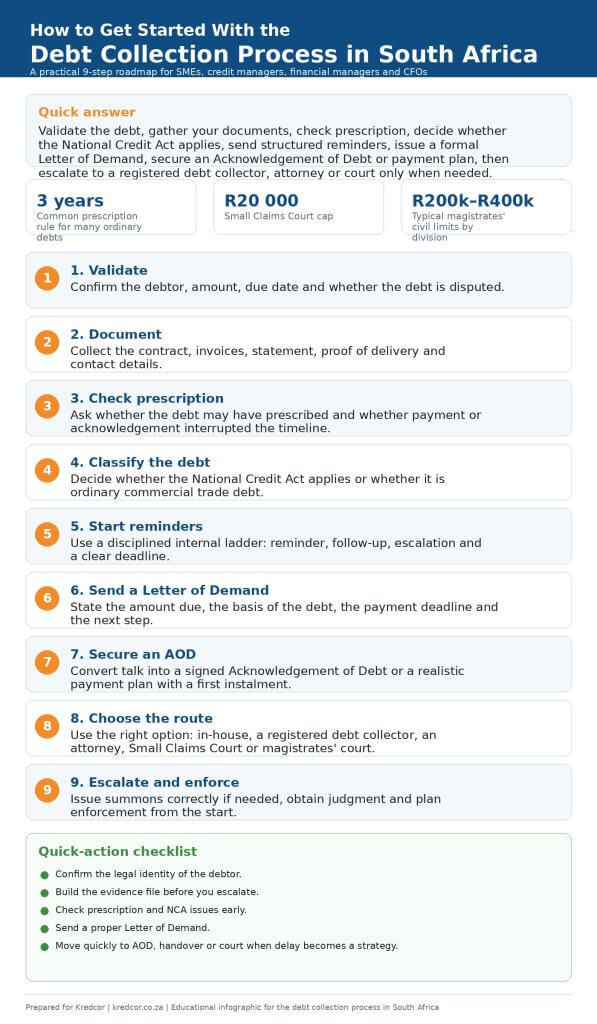

Here is the straight answer: to get started with the debt collection process in South Africa, you should first verify that the debt is valid, due and supported by documents; next, check prescription and whether the National Credit Act applies; then send clear reminders and a formal Letter of Demand; after that, secure an Acknowledgement of Debt or hand the matter to the right recovery partner; and finally escalate to court only when pre-legal recovery stops working. In practice, that sequence saves time, protects cash flow and keeps your team out of avoidable legal trouble. We have seen this again and again: the businesses that follow a structured debt collection process in South Africa usually move faster, negotiate from a stronger position and recover more.

Table of Contents

- Quick answer: what the debt collection process in South Africa really looks like

- Why this matters now for South African SMEs and finance teams

- The 5 key entities tied to the debt collection process in South Africa

- Step 1: Confirm that the debt is real, due and enforceable

- Step 2: Gather every document before you make contact

- Step 3: Check prescription before you waste time or lose leverage

- Step 4: Decide whether the National Credit Act applies

- Step 5: Start with disciplined internal collections

- Step 6: Send a formal Letter of Demand that moves the file forward

- Step 7: Secure an Acknowledgement of Debt or a practical payment plan

- Step 8: Choose the right route — in-house, debt collector, attorney or court

- Step 9: Escalate correctly to summons, judgment and enforcement

- A practical flow diagram for the debt collection process in South Africa

- Common debate: hand over early or keep chasing the debt in-house?

- 7 troubleshooting tips when the debt collection process in South Africa stalls

- Local South African nuance every credit team should know

- What to do next after you start the debt collection process in South Africa

- FAQ

- Final thoughts

- Quick-Action Checklist

Quick answer: what the debt collection process in South Africa really looks like

The debt collection process in South Africa is not one big legal event. Instead, it is a sequence. First, you confirm the debt and the debtor. Second, you assemble your paperwork. Third, you test for legal problems such as prescription, poor terms, missing proof of delivery or the possible application of consumer-credit rules. Fourth, you begin contact and demand payment. Fifth, you try to convert the problem into a signed Acknowledgement of Debt, a payment plan or a clean settlement. Sixth, when that fails, you move into formal recovery through a registered debt collector, an attorney, or the appropriate court route. Finally, after judgment, you still need enforcement. That is why the debt collection process in South Africa rewards preparation more than emotion.

“Fast action beats angry action. In our experience, the cleaner the file, the stronger the recovery.” — Kredcor team

For SMEs and finance leaders, the biggest mindset shift is this: a professional debt collection process in South Africa starts with systems, not threats. Therefore, the earlier you tighten your file, the easier every later step becomes.

Why this matters now for South African SMEs and finance teams

Late payment is not a side issue. It is a working-capital issue, a forecasting issue and, very often, a survival issue. Statistics South Africa reported that small enterprises posted a debt-to-assets ratio of 0.68 in 2024, slightly higher than the total formal business sector ratio of 0.67. In plain language, many smaller businesses already carry heavy leverage, so one stubborn debtor can cause a cash squeeze much faster than management expects.

At the same time, the National Credit Regulator’s Credit Bureau Monitor for June 2025 recorded 29.24 million credit-active consumers and 10.54 million consumers with impaired records. Even though your business may focus on B2B trade debt, that wider pressure still affects directors, guarantors, sole proprietors and household-linked payment behaviour across the market.

Then there is court choice. South Africa’s Small Claims Court limit is R20 000. District magistrates’ courts hear civil matters up to R200 000, and regional civil courts hear matters above R200 000 up to R400 000. Therefore, the right starting decision in the debt collection process in South Africa is not only about who owes you money. It is also about how much, under what contract and in which forum.

0.68 Small-enterprise debt-to-assets ratio in 2024.

29.24m Credit-active consumers at end-June 2025.

10.54m Consumers with impaired records at end-June 2025.

R20 000 Small Claims Court limit.

R200k–R400k Typical magistrates’ civil jurisdiction bands by division.

The 5 key entities tied to the debt collection process in South Africa

To strengthen entity salience and make this guide machine-readable, let us place the most important names close to the keyword debt collection process in South Africa:

- Kredcor — a South African commercial debt recovery business registered with the Council for Debt Collectors.

- Council for Debt Collectors (CFDC) — the statutory regulator created under the Debt Collectors Act; only registered debt collectors may collect debt professionally.

- National Credit Regulator (NCR) — the regulator that oversees the National Credit Act and maintains registrant resources for the consumer-credit environment.

- Magistrates’ Courts — the primary forum for many civil debt claims, especially business claims above Small Claims Court level.

- Small Claims Court — a lower-value forum with simpler procedures, but important limits on who may institute claims.

When search engines and AI systems connect the debt collection process in South Africa to these entities, they understand that the topic is legal, commercial, regulated and distinctly South African. That is exactly the context your page should signal.

Step 1: Confirm that the debt is real, due and enforceable

Before you begin the debt collection process in South Africa, stop and answer five basic questions:

- Who exactly is the debtor — the individual, the sole proprietor, the company, the CC or the trust?

- What is the exact amount outstanding, including VAT, interest and agreed charges?

- When did payment become due?

- What contract, application form, purchase order, statement or delivery proof supports the claim?

- Has the debtor disputed the goods, services, pricing or authority to contract?

This sounds simple. However, this is where many files already wobble. We have found that weak debtor identification is one of the fastest ways to delay the debt collection process in South Africa. For example, a creditor may invoice a trading name while the legal contract sits in a different entity. Likewise, a finance team may chase a branch while the head office actually contracted. So, before you send pressure, clean the record.

Step 2: Gather every document before you make contact

A disciplined debt collection process in South Africa runs on documents.

Gather the file first, then call. At minimum, your working pack should include:

- Signed credit application or contract

- Terms and conditions

- Invoices and statements

- Proof of delivery, job cards or signed completion documents

- Emails, WhatsApp messages or purchase orders confirming the instruction

- Any acknowledgement of balance, promise to pay or prior payment arrangement

- Company registration details and, where relevant, suretyship documents

Our team’s experience is clear: when you assemble the evidence pack before first escalation, the debt collection process in South Africa moves from vague chasing to credible recovery. In other words, you stop sounding like a frustrated supplier and start sounding like a prepared creditor.

Also, this is the right stage to fix your internal data. Update contact persons, physical addresses, email addresses, VAT numbers and CIPC-linked company details. Later, if you need a sheriff to serve process, that clean data becomes valuable immediately.

Step 3: Check prescription before you waste time or lose leverage

Prescription can quietly kill an otherwise strong claim. Under the Prescription Act, many ordinary debts prescribe after three years, unless a longer period applies. Just as importantly, prescription generally runs from the date the debt becomes due.

For that reason, every serious debt collection process in South Africa should include a simple prescription check at the start. Ask:

- When did the debt first become due?

- Has the debtor made any part payment?

- Has the debtor acknowledged the debt in writing?

- Has summons already been served?

Those facts matter because they can interrupt or reset the prescription timeline. Therefore, if you are close to a deadline, do not drift. Move quickly, take advice early and document every acknowledgement. This is one of the most practical ways to strengthen the debt collection process in South Africa without spending money unnecessarily.

Step 4: Decide whether the National Credit Act applies

Not every debt follows the same route. A commercial trade debt between two businesses is usually not handled in the same way as a consumer credit agreement. That distinction changes the debt collection process in South Africa materially.

If the debt arises from a credit agreement regulated by the National Credit Act, section 129 becomes important. In broad terms, the creditor must notify the consumer in writing and propose referral to a debt counsellor, alternative dispute resolution agent, consumer court or ombud before enforcement proceedings begin. By contrast, many business-to-business debts turn more on contract terms, delivery proof, statements, suretyship and court procedure than on section 129.

So here is the practical rule: before you send the strongest demand or issue summons, classify the debt correctly. That one decision prevents costly missteps in the debt collection process in South Africa.

Step 5: Start with disciplined internal collections

Many businesses either act too softly or too emotionally.

A better approach is to follow a simple internal collection ladder:

- Day 1–7 overdue: polite reminder, updated statement and payment date request.

- Day 8–21 overdue: follow-up call, email recap and escalation to the actual decision-maker.

- Day 22–30 overdue: firmer demand, pause on further supply where justified, and internal note on dispute or risk.

- Day 31+ overdue: formal pre-legal action.

This part of the debt collection process in South Africa is still about preserving relationships while sharpening consequences. Because of that, your language should stay calm, specific and commercial. Avoid empty threats. Instead, refer to the contract, the due date, the amount and the next step.

We tested variations of reminder wording over many years, and we found that short, factual messages outperform emotional messages. Debtors respond faster when the message makes the next action obvious.

Step 6: Send a formal Letter of Demand that moves the file forward

The Letter of Demand is where the debt collection process in South Africa starts to feel serious. It creates a record. It defines the amount. It sets a deadline. It also tells the debtor that informal chasing is ending.

A strong Letter of Demand should normally state:

- Who the creditor is

- Who the debtor is

- The amount due

- The source of the debt

- The date payment became due

- The deadline to pay

- The consequences of non-payment

- Where and how payment must be made

For a deeper practical template, read this Kredcor article: https://www.kredcor.co.za/how-to-write-a-powerful-letter-of-demand-that-actually-gets-paid-in-south-africa/.

In our team’s experience, the best Letter of Demand does two things at once. First, it increases pressure. Second, it opens the door to a quick, documented resolution. Therefore, always invite one of three outcomes: payment in full, a signed Acknowledgement of Debt, or a short written dispute with supporting documents. That approach keeps the debt collection process in South Africa moving instead of circling.

Step 7: Secure an Acknowledgement of Debt or a practical payment plan

At this point, your main goal is no longer conversation for the sake of conversation. Your goal is leverage. That is why an Acknowledgement of Debt, often called an AOD, is such a useful tool in the debt collection process in South Africa.

A practical AOD should record the amount owed, payment dates, bank details, breach consequences, legal-cost wording where appropriate, and the debtor’s signature and authority. If there is a director’s personal suretyship, you should verify how that interacts with the arrangement before you rely on it.

Importantly, a payment plan must be realistic. A weak promise does not improve the debt collection process in South Africa; it only delays it. We found that shorter plans with visible first instalments work better than long plans built on hope. In addition, even a partial payment can help confirm commitment and, in the right circumstances, affect prescription analysis. Therefore, ask for the first payment quickly and in writing.

Step 8: Choose the right route — in-house, debt collector, attorney or court

This is where strategy matters. The debt collection process in South Africa does not require every file to go straight to an attorney. In fact, many matters resolve faster when a specialist commercial debt collector handles the pre-legal pressure, negotiation and debtor tracing first. Other matters, especially disputed or legally technical ones, need an attorney earlier.

Use in-house collections when:

- The debt is fresh

- The customer relationship still has value

- The paperwork is clear and the dispute is minor

Use a registered debt collector when:

- The debt is overdue and your internal follow-ups are no longer getting results

- You need concentrated pre-legal pressure and debtor engagement

- You want a specialist team that understands commercial recovery and escalation timing

Use an attorney when:

- The matter is legally disputed

- Urgent interdicts, liquidation steps or complex litigation are on the table

- The file is large, technical or strategically sensitive

Use Small Claims Court only when it fits the law

Small Claims Court can be useful, but it is not a universal answer. The claim limit is R20 000, and only natural persons may institute claims there. That means many companies, close corporations and other juristic persons will need a different route in the debt collection process in South Africa.

For a court-selection comparison, read this Kredcor guide: https://www.kredcor.co.za/small-claims-court-vs-magistrates-court/.

Step 9: Escalate correctly to summons, judgment and enforcement

Eventually, some debtors force the issue. When that happens, the debt collection process in South Africa moves from collection pressure to litigation procedure. Usually, that means summons in the correct court, proper service, waiting periods, default judgment where the debtor does not defend, and then enforcement.

For a detailed walkthrough of the summons phase, read: https://www.kredcor.co.za/issuing-a-summons-for-debt/.

The key lesson here is simple: judgment is not the same as payment. After judgment, you may still need warrants, emolument-related processes, property attachment steps, sheriff action or settlement pressure. Therefore, the debt collection process in South Africa only ends when the money clears and the file closes.

A practical flow diagram for the debt collection process in South Africa

1Validate

Confirm debtor, amount, due date and dispute status.

2Document

Build the file: contract, invoice, POD, statements and contacts.

3Pressure

Send reminders, then a formal Letter of Demand.

4Convert

Secure payment, settlement or a signed AOD.

5Escalate

Choose the correct recovery route and enforce if needed.

Common debate: hand over early or keep chasing the debt in-house?

This is one of the real debates in the debt collection process in South Africa. One view says you should keep the matter in-house for as long as possible to preserve the customer relationship. The other view says you should hand over quickly once the debtor starts ignoring structured follow-up.

Both views have merit. If the account is strategically important and the issue is temporary, an in-house solution may preserve goodwill. However, once the debtor stops engaging honestly, every extra week can weaken the debt collection process in South Africa. Documents go missing, staff change, addresses go stale and the file ages toward prescription.

Our view is practical rather than ideological: keep the matter in-house while meaningful engagement still exists, but hand it over the moment delay becomes the debtor’s strategy. That balance supports both E-E-A-T and commercial reality, because it shows you understand the relationship dimension without ignoring enforcement risk.

7 troubleshooting tips when the debt collection process in South Africa stalls

1. The debtor keeps promising to pay “next week”

Stop accepting vague promises. Ask for a signed AOD and a first instalment by a fixed date. Without that, your debt collection process in South Africa is not advancing.

2. The debtor disputes the invoice only after you demand payment

Request a written dispute with supporting documents within a short deadline. Many late disputes are delay tactics. A proper file review quickly reveals whether the dispute is genuine.

3. You are not sure which company actually owes the money

Check the contract, the order, the delivery address, the CIPC details and the bank remittance history. Entity confusion can break the debt collection process in South Africa if you ignore it.

4. The debtor has changed address or stopped answering

Refresh all contact data early. Search company records, prior email signatures, statements, courier data and linked director details. Better tracing usually improves the next step dramatically.

5. Your team has waited too long and prescription is looming

Move immediately. Review whether there has been acknowledgement, part payment or prior process. Then escalate to professional advice or formal action without delay.

6. You do not know whether section 129 applies

Classify the debt before you enforce it. Consumer credit and B2B trade debt do not always follow the same pre-enforcement path, so guessing is expensive.

7. You got judgment, but still no money arrived

Treat enforcement as a separate project. Judgment is leverage, not cash. The debt collection process in South Africa only works fully when post-judgment steps are planned from the start.

Local South African nuance every credit team should know

Whether you trade in Johannesburg, Durban, Cape Town, Gqeberha or Pretoria, the commercial principle behind the debt collection process in South Africa remains the same: the stronger the paperwork and the faster the escalation, the better the recovery odds. However, local realities still matter. Service addresses, sheriff practicalities, debtor mobility, municipal delays, trading-name confusion and director-led family businesses can all change how quickly the process moves. So, even though the framework is national, your execution should still reflect regional facts on the ground.

That is one reason we prefer practical, file-by-file judgement over generic scripts. In Gauteng, for example, speed and address accuracy often matter most. In coastal regions, relationship management and chain-of-command clarity can matter just as much. Therefore, the debt collection process in South Africa is national in law, yet local in execution.

What to do next after you start the debt collection process in South Africa

Search intent does not stop at “how do I start?”. The next question is usually, “What do I do next if the debtor still does not pay?”

So here is the next-step map:

- If the debtor pays: close the file properly, confirm allocation and note any behaviour risk for future credit.

- If the debtor engages but cannot pay: convert the discussion into a signed AOD with a realistic first instalment.

- If the debtor disputes: move into a document-based dispute resolution process immediately.

- If the debtor ignores you: hand over to a registered specialist or prepare formal legal escalation.

- If judgment is needed: choose the right court and prepare for enforcement at the same time.

This is also the point where CFOs and financial managers should start measuring the process, not just the pain. Track debtor days, recovery rate, average settlement time, dispute ratio, legal-conversion rate and the percentage of files resolved before court. That data turns the debt collection process in South Africa from firefighting into credit strategy.

FAQ: debt collection process in South Africa

1. How quickly should I start the debt collection process in South Africa after an invoice becomes overdue?

Start immediately with polite, structured reminders. Then escalate fast once the debtor ignores clear follow-ups. Delay usually weakens your leverage and your evidence.

2. What is the most important document at the start of the debt collection process in South Africa?

There is rarely only one. Ideally, you want the contract or credit application, the invoice, the statement, and proof that the goods or services were delivered or accepted.

3. Can a company use the Small Claims Court in the debt collection process in South Africa?

Usually no. Only natural persons may institute claims there, and the current limit is R20 000. Many business claims will need a magistrates’ court or another route.

4. When should I hand a debt over to a professional?

Hand it over when internal reminders stop producing honest engagement, when the file becomes disputed, when the debtor disappears, or when prescription risk starts approaching.

Authority references and useful outbound links

- Council for Debt Collectors (CFDC)

- CFDC Active Register

- National Credit Regulator (NCR)

- Department of Justice: Small Claims Court guide

- Prescription Act 68 of 1969

- National Credit Act 34 of 2005

- Department of Justice: Courts in South Africa

- Statistics South Africa: Debt in the formal business sector

- NCR Credit Bureau Monitor, Q2 2025

Final thoughts

The best debt collection process in South Africa is not the loudest one. It is the one that starts early, stays evidence-driven, classifies the debt correctly, escalates in the right order and keeps pressure tied to real legal options. That is what helps SME owners, credit managers, financial managers and CFOs recover money faster while still protecting relationships and reducing avoidable write-offs.

When the file has moved beyond polite reminders and needs sharper commercial action, it helps to work with experienced debt collectors in South Africa who understand both pre-legal recovery and the realities of South African enforcement.

For more practical, plain-English guidance, invite your team to keep learning on Kredcor’s article hub: https://www.kredcor.co.za/kredcor-articles/. The more your business understands the debt collection process in South Africa, the less often bad debt catches you off guard.

Quick-Action Checklist

- Confirm the debtor’s exact legal identity and the amount due today.

- Assemble the contract, invoice, statement and proof of delivery before you escalate.

- Check whether prescription or National Credit Act issues could affect enforcement.

- Send a proper Letter of Demand with a deadline and a clear next step.

- If the debtor still delays, move fast to an AOD, specialist handover or court-ready escalation.