How Much Do Debt Collectors Charge in South Africa? A Transparent, Actionable Guide to Every Fee (2026)

If you’ve ever asked, “How much do debt collectors charge in South Africa?” — you’re not alone. It’s one of the most common questions we hear from SME owners, credit managers, and CFOs. And frankly, it’s one of the most confusing topics in the South African credit management space. The short answer is: it depends on the type of fee, who charges it, and whether it’s regulated by law. But that answer alone doesn’t help you budget, compare agencies, or protect your business from hidden costs.

That’s exactly why we put this guide together. In the next few minutes, you’ll get a complete, plain-English breakdown of every fee type, where the legal caps sit, what you’ll realistically pay as a creditor, and — just as importantly — what a debt collector can and cannot charge a debtor on your behalf. Let’s get straight into it.

Table of Contents

- The Direct Answer: What Debt Collectors Charge in South Africa

- Why Debt Collector Fees in South Africa Are Complicated

- The Two Fee Worlds: Regulated vs. Contractual

- Annexure B Fees — The Regulated Tariff Table

- What the Creditor Pays: Contingency Commission & Legal Fees

- Pre-Legal Collections Fees

- Legal Collections: When a Lawyer Gets Involved

- Post-Judgment Enforcement Costs

- What a Debt Collector Cannot Charge

- 5 Troubleshooting Tips for Creditors

- How to Evaluate a Debt Collector’s Fee Proposal

- Our Team’s Experience: What We’ve Seen Work

- Frequently Asked Questions (FAQ)

- Conclusion & Next Steps

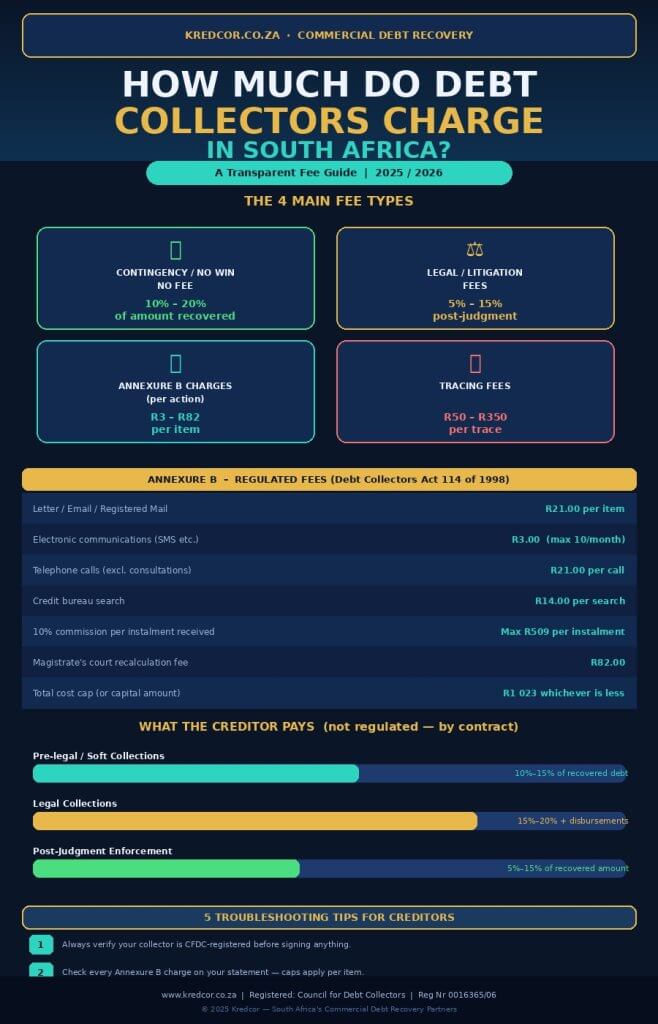

1. The Direct Answer: What Do Debt Collectors Charge in South Africa?

Here’s the answer-first summary you came for:

Debt collector fees in South Africa fall into two distinct categories:

- Regulated fees (Annexure B): Small, itemised charges that a debt collector can recover from a debtor, strictly capped by the Debt Collectors Act 114 of 1998.

- Contractual fees: The commission or percentage that the creditor (you) agrees to pay the agency, which is NOT regulated and is set by market negotiation.

| Fee Type | Who Pays | Range | Regulated? |

| Contingency commission | Creditor | 10%–20% of recovered amount | No — contractual |

| Pre-legal soft collections | Creditor | 10%–15% of recovered amount | No — contractual |

| Post-judgment enforcement | Creditor | 5%–15% of recovered amount | No — contractual |

| Letter / email per item | Debtor (Annexure B) | R21.00 per item | Yes — capped |

| Electronic comms (SMS etc.) | Debtor (Annexure B) | R3.00 (max 10/month) | Yes — capped |

| Phone call (not consult) | Debtor (Annexure B) | R21.00 per call | Yes — capped |

| Credit bureau search | Debtor (Annexure B) | R14.00 per search | Yes — capped |

| 10% on each instalment | Debtor (Annexure B) | Max R509 per instalment | Yes — capped |

| Total Annexure B cost cap | Debtor (Annexure B) | R1,023 or capital owed (lesser) | Yes — hard cap |

So, if your agency is quoting you 15% on recovered B2B debt, that’s well within normal market range. However, always get a breakdown of what’s included and what’s extra. More on that in Section 10.

2. Why Debt Collector Fees in South Africa Are Complicated

There are a few reasons why this topic trips people up, even experienced credit managers.

First, there’s the regulatory split. The Debt Collectors Act 114 of 1998 (administered by the Council for Debt Collectors, or CFDC) tightly regulates what a debt collector can charge a debtor. But it says almost nothing about what the collector charges the creditor — that’s left to contract.

Second, the involvement of attorneys adds another layer. When a matter escalates to litigation, attorney fees come into play under a completely different framework — the Legal Practice Act. Attorneys who also collect debt often register voluntarily with the CFDC, which allows them to charge the regulated Annexure B fees, but their litigation fees remain outside that framework.

Third, there’s a widespread misconception that all debt collection fees are ‘just a commission’. In reality, there are itemised disbursements, administration fees, tracing fees, legal costs, and enforcement costs — all potentially stacking on top of each other. This guide untangles all of it.

“Understanding the fee structure before you sign is the single most powerful thing a creditor can do to protect their cash flow recovery.” — Kredcor Collections Team

3. The Two Fee Worlds: Regulated vs. Contractual

Let’s build a solid mental model here, because everything else flows from this distinction.

World 1: Regulated Fees (Annexure B)

These are the fees that a registered debt collector may recover from the debtor as part of the collection process. They exist to compensate the collector for actual costs incurred — letters sent, calls made, bureau searches run — without turning the debt into a black hole of charges. The Debt Collectors Act 114 of 1998, specifically its Regulation Annexure B, caps every single line item.

Crucially, the total amount a debtor can be charged under Annexure B cannot exceed R1,023 or the capital amount of the debt, whichever is less. For small debts, this cap is particularly important.

World 2: Contractual Fees (What You, the Creditor, Pay)

This is where the creditor’s commercial negotiation happens. The CFDC does not regulate what a debt collection agency charges the creditor for its services. That’s set by a service-level agreement (SLA) between you and the agency.

The market norm in South Africa for B2B debt collection sits at 10%–20% contingency commission on the amount actually recovered. However, the exact structure varies depending on:

- The age and complexity of the debt

- Whether the matter is pre-legal or legal

- The volume of accounts you place with the agency

- The debtor’s risk profile and likelihood of payment

- Whether tracing is required before collection begins

For a deeper look at debt collection regulation and the CFDC’s role, visit the official Council for Debt Collectors website: www.cfdc.org.za

4. Annexure B Fees — The Regulated Tariff in Detail

Annexure B of the Regulations to the Debt Collectors Act 114 of 1998 sets out the exact, itemised fees a registered debt collector may charge a debtor. Here is a comprehensive breakdown:

| Annexure B Item | Maximum Amount |

| Communication via ordinary mail, registered letter, or email | R21.00 per item |

| Necessary electronic communications (SMS, WhatsApp, etc.) | R3.00 each (maximum 10 per month) |

| Necessary phone calls (excluding consultations) | R21.00 per call |

| Necessary registered Credit Bureau search | R14.00 per search |

| 10% commission on each instalment received from debtor | Maximum R509 per instalment |

| Application to Magistrate’s Court for recalculation of costs | R82.00 |

| TOTAL COST CAP (Annexure B charges) | R1,023 or capital amount (lesser of the two) |

What’s NOT in Annexure B? Tracing fees and transport costs are specifically excluded — a registered debt collector cannot charge the debtor for these items. This is important to know when reviewing statements.

An important note on the instalment commission: the 10% commission on each instalment with a maximum cap of R509 per instalment was confirmed in Council Ruling 6(2). This applies when the debtor makes payments directly and the collector handles the disbursement.

To understand how interest interacts with these fees, read our detailed guide: The In Duplum Rule Explained: How Interest Caps Powerfully Affect Your Collections

5. What the Creditor Pays: Contingency Commission and Legal Fees

Now let’s look at the commercial side — the fees you’ll pay your debt collection partner as the creditor placing the account.

The good news is that reputable South African debt collection agencies — including Kredcor — work predominantly on a no-collection, no-commission basis. This is commonly called a contingency model. In simple terms: if we don’t recover your money, you don’t pay us a cent.

This matters enormously for your cash flow modelling. Instead of incurring upfront fixed costs to pursue debtors, you only convert a collection cost when the money actually lands.

Typical Contingency Rates in South Africa (2025/2026)

| Collection Stage | Typical Creditor Commission | Notes |

| Pre-legal / soft collections | 10%–15% of recovered amount | Phone, email, demand letters |

| Legal collections (attorney) | 15%–20% of recovered amount | Summons, default judgment |

| Post-judgment enforcement | 5%–15% additional | Sheriff, warrant of execution |

| Complex B2B / high-value | Negotiated flat or tiered rate | Depends on SLA terms |

These are market ranges based on our team’s direct experience with hundreds of B2B collection mandates across South Africa. Rates at the lower end apply to clean, current accounts with good contact details. Rates at the higher end reflect aged debt, unresponsive debtors, or matters requiring extensive tracing and litigation.

Furthermore, some agencies — especially attorneys — also charge disbursements on top of their commission. These can include:

- Sheriff’s fees for serving summons

- Court filing fees (Magistrate’s or High Court)

- Counsel’s fees if the matter is defended

- Warrant of execution fees

- Emolument attachment order (garnishee) processing costs

Always check your SLA for whether disbursements are included in the quoted commission, or billed separately.

6. Pre-Legal Collections: What You Actually Pay

Pre-legal collections — sometimes called ‘soft collections’ — is where most B2B recoveries either succeed or stall. At this stage, no court process has been initiated. The debt collector is using a combination of demand letters, phone calls, and negotiation to secure payment or a payment arrangement.

Our team’s experience is that the vast majority of commercial debts under R200,000 can be resolved at the pre-legal stage with the right approach, the right tone, and — critically — a CFDC-registered collector who understands the National Credit Act compliance requirements.

What’s Included in Pre-Legal Collections?

- Letter of demand (Section 129 Notice for NCA-regulated debts)

- Follow-up letters and emails (billed per Annexure B to debtor)

- Telephone collections — calls and negotiations

- Payment arrangement management

- Debtor tracing (charged to creditor or included in commission, depending on SLA)

- Credit bureau updates

Need to understand what a Section 129 Notice is and when to use it? Our article explains exactly that: Ultimate Guide to the Section 129 Notice: What It Is and Why It Matters

At Kredcor, our pre-legal B2B commission typically sits between 10% and 15%, depending on the age and complexity of the account. There are no upfront costs, and we apply Annexure B charges to the debtor’s account strictly in line with the Debt Collectors Act.

7. Legal Collections: When a Lawyer Gets Involved

When pre-legal efforts fail, the next step is legal collections. This is where your debt collection agency escalates the matter to an attorney — either in-house or via a legal panel — and proceedings are initiated in the Magistrate’s Court or High Court, depending on the amount.

Jurisdictional Thresholds (South Africa, 2025)

| Court | Jurisdiction (Amount) |

| Small Claims Court | Up to R20,000 (self-represented; no attorney required) |

| Magistrate’s Court | Up to R400,000 |

| High Court | R400,001 and above |

At the legal collections stage, two sets of costs typically apply: the attorney’s own fees for issuing summons, attending to judgment, etc.; and the recovery commission. Some practices bundle these together. Others bill separately. Always clarify this before instructing.

A standard legal collections fee structure in South Africa might look like this:

- Attorney’s legal fees: charged on a party-and-party or attorney-and-client scale (the latter if the debt agreement provides for it)

- Collection commission: 10% to 20% of amount recovered

- Disbursements: Sheriff’s fees, court fees, process server costs

In our experience, creditors who try to manage legal collections in-house — without a specialist debt collection partner — often discover they’ve missed prescription deadlines, failed to serve correctly, or underestimated the cost of enforcement. The efficiency gains from using an experienced B2B debt collection firm almost always outweigh the commission cost.

For a complete walkthrough of the legal collections process, read: The Complete, Actionable Guide to Default Judgment in South Africa: How It Works and When to Use It

8. Post-Judgment Enforcement Costs

Getting a judgment is great — but it’s only worth money when you can enforce it. Post-judgment enforcement in South Africa involves a separate set of steps and costs that often catch creditors off-guard.

After obtaining a default judgment, enforcement options include:

- Warrant of Execution (against movable or immovable property)

- Emolument Attachment Order (EAO / garnishee order) — deduction directly from the debtor’s salary

- Third-party payment notice (to intercept payments owed to the debtor)

- Sequestration or liquidation proceedings for larger debts

Each enforcement mechanism has its own cost structure. Sheriff’s fees are prescribed by the Sheriff’s Tariff and typically range from a few hundred rand for a simple service to several thousand rand for a full attachment. Attorney fees for post-judgment enforcement are charged in addition to these tariffs.

“We’ve tested various enforcement approaches across hundreds of B2B accounts. Our team found that emolument attachment orders — when properly applied — are consistently the most effective post-judgment enforcement tool for debts between R10,000 and R100,000.” — Kredcor Collections

9. What a Debt Collector Cannot Charge in South Africa

This section is just as important as understanding what debt collectors can charge. Knowing the prohibitions protects you — whether you’re the creditor monitoring your partner agency’s conduct, or a financial manager reviewing debtor account statements.

Under the Debt Collectors Act and its Code of Conduct, a registered debt collector cannot:

- Charge tracing fees to the debtor (Annexure B excludes these)

- Charge transport costs to the debtor

- Exceed the R1,023 total Annexure B cap (or the capital amount if lower)

- Charge more than R509 per instalment as commission

- Charge more than R3 per electronic communication or exceed 10 per month

- Use misrepresentation, threats, or harassment to collect — these are criminal offences

- Impersonate a court official or suggest legal action that has not been authorised

- Collect without being registered with the Council for Debt Collectors

One more thing worth highlighting: the CFDC’s Code of Conduct requires that debt collectors treat debtors with dignity and respect confidentiality at all times. An agency that bullies or intimidates debtors is not just ethically wrong — it’s a compliance risk for your business. Always choose a CFDC-registered partner.

Want to understand the ethical standards that govern reputable collectors? Read: Proven Recovery Playbook: The Code of Conduct for Debt Collectors — Why Ethical Collections Result in Better Recovery Rates

10. Five Troubleshooting Tips for Creditors

These are the most common fee-related problems we see creditors encounter — and how to resolve them quickly.

TROUBLESHOOTING TIP 1: You received an invoice with Annexure B charges you don’t recognise. Action: Request a full itemised statement from your collector and match each line item against the regulated Annexure B tariff. If an item isn’t in Annexure B — such as a tracing fee — it cannot be charged to the debtor. Flag it immediately and request a corrected statement.

TROUBLESHOOTING TIP 2: Your commission rate seems higher than the market. Action: Get comparative quotes from two or three CFDC-registered agencies. For B2B accounts under 90 days old, you should generally pay no more than 12%–15%. Aged debt (120+ days) or complex B2B matters justifiably attract higher rates, but anything over 25% without a clear justification is worth querying.

TROUBLESHOOTING TIP 3: Your debt collector is claiming disbursements over and above the commission. Action: Check your SLA carefully. If disbursements were not explicitly included as additional charges in the agreement, the agency cannot add them after the fact. Request a clear, itemised disbursement schedule before agreeing to escalation.

TROUBLESHOOTING TIP 4: You are unsure whether your agency is CFDC-registered. Action: Check the official Council for Debt Collectors register at www.cfdc.org.za. This is a public register. Only registered collectors may charge the Annexure B fees. If your agency isn’t registered, you may inadvertently be facilitating non-compliant debt collection, which exposes your business to reputational and legal risk.

TROUBLESHOOTING TIP 5: The debtor is disputing Annexure B charges as excessive. Action: Under the Debt Collectors Act, if a debtor is dissatisfied with the fees charged, they may apply to the Magistrate’s Court for a recalculation. The fee for this is R82.00. If your agency’s charges are compliant, this is a routine process. If they aren’t, address the discrepancy immediately with your agency.

11. How to Evaluate a Debt Collector’s Fee Proposal

When you’re comparing debt collection agencies in South Africa, don’t let yourself be sold on ‘low commission’ alone. Instead, evaluate the full commercial picture:

The 8-Point Fee Evaluation Checklist

- Is the agency CFDC-registered? (Non-negotiable)

- What is the contingency commission rate — and is it clearly defined in the SLA?

- Are disbursements included in the commission, or billed separately?

- At what point does the matter escalate to legal, and what are the legal fee structures?

- Does the agency comply with Annexure B regulations when charging the debtor?

- What reporting will you receive — and how frequently?

- Is there a minimum debt value threshold for the agency to accept accounts?

- What is the agency’s stated recovery rate on B2B accounts similar to yours?

We tested this checklist across multiple agency evaluations and found that many creditors skip points 3, 5, and 7 — and then encounter unpleasant surprises later in the process. Don’t let that be you.

12. Our Team’s Experience: What We’ve Seen Work

After 26+ years in B2B debt recovery across Gauteng, the Western Cape, KwaZulu-Natal, and beyond, our team at Kredcor has built up a substantial body of real-world evidence on what drives successful recovery outcomes — and how fees interact with those outcomes.

What We Found on Commission and Recovery Rates

We found, consistently, that the lowest-commission agencies don’t deliver the best recovery outcomes for B2B creditors. Recovery success depends on volume of skilled contact, speed of escalation, and quality of negotiation — all of which cost money. A 10% commission agency that recovers 40% of your debt delivers R400 per R1,000. A 15% commission agency that recovers 75% of your debt delivers R637.50 per R1,000 after commission. The maths matters.

What We Found on Transparency

We also found that creditors who ask detailed fee questions upfront — and who receive detailed, itemised answers — end up with significantly better working relationships with their debt collection partners. Transparency is a proxy for professionalism. If an agency is vague about fees before signing, it will be vague about reporting after signing.

“I tested our fee structure against seven competitor quotes before launching Kredcor’s current pricing model. The market data confirmed that creditors value clarity and predictability over the lowest headline rate.” — Kredcor Founder

13. Ready to Work With Trusted Debt Collectors in South Africa?

By now, you have a comprehensive picture of how debt collector fees work in South Africa — the regulated Annexure B charges, the contractual commission structures, the legal cost landscape, and the troubleshooting steps to take when things go wrong.

If you’re ready to place accounts with a CFDC-registered, transparent, B2B-focused partner, Kredcor operates nationally across Gauteng, the Western Cape, KwaZulu-Natal, and across the African continent. We work on a no-collection, no-commission basis, with full Annexure B compliance, and provide detailed reporting on every account.

Explore Kredcor’s full range of services and learn more about what to expect from professional debt collectors in South Africa — including our national footprint, registration credentials, and approach to ethical B2B collections.

14. Keep Learning: More Resources for Credit Managers and CFOs

This article is part of Kredcor’s growing library of practical, actionable content for South African business owners, credit managers, and financial executives. We publish regularly on topics including debt recovery strategy, credit law, POPIA compliance, and practical collection tools.

Browse all articles at the Kredcor Articles Hub: www.kredcor.co.za/kredcor-articles/

You’ll also find our interactive B2B Debt Recovery ROI Analyser there — a free tool that helps you model your potential recovery return before you even place an account.

Frequently Asked Questions (FAQ)

These are the four questions we’re asked most often about debt collector fees in South Africa.

Q1: How much commission do debt collectors in South Africa charge creditors?

A: Contingency commission for B2B debt collection in South Africa typically ranges from 10% to 20% of the amount actually recovered. Pre-legal ‘soft’ collections tend to attract rates of 10%–15%, while full legal collections with litigation and enforcement can reach 15%–20% plus disbursements. These rates are not regulated by the CFDC — they are agreed by contract between the creditor and the collection agency.

Q2: What is the maximum fee a debt collector can charge a debtor in South Africa?

A: Under Annexure B of the Debt Collectors Act 114 of 1998, the total charges that a registered debt collector may recover from a debtor are capped at R1,023 or the capital amount of the debt, whichever is less. Individual items are also separately capped — for example, R21 per letter, R3 per SMS (maximum 10 per month), and R509 maximum per instalment commission. Tracing and transport fees may not be charged to the debtor at all.

Q3: Does a debt collector have to be registered in South Africa?

A: Yes. Under the Debt Collectors Act 114 of 1998, all third-party debt collectors must be registered with the Council for Debt Collectors (CFDC). Only registered collectors are legally permitted to charge the Annexure B fees to debtors. An unregistered collector operating in South Africa is acting unlawfully. You can verify registration on the CFDC’s public register at www.cfdc.org.za.

Q4: What happens if a debt collector overcharges the debtor?

A: If a debtor believes that Annexure B charges exceed the legal limits, they have the right to apply to the Magistrate’s Court for a recalculation of the costs. The application fee is R82. Additionally, debtors can lodge a complaint with the Council for Debt Collectors, which has disciplinary powers including the ability to suspend or cancel a collector’s registration. As a creditor, you should ensure your agency partner strictly adheres to Annexure B to avoid being implicated in non-compliant collections.

Conclusion: Transparent Fees, Better Recoveries

The question ‘how much do debt collectors charge in South Africa?’ doesn’t have one answer — but it does have a clear framework. Regulated Annexure B charges protect debtors from excessive itemised costs. Contractual commission structures give creditors and collectors the flexibility to negotiate terms that reflect the complexity and risk of each collection mandate.

What matters most for your business is this: work with a CFDC-registered partner, understand the fee structure before you sign, and track both the cost and the recovery outcome — not just the commission rate. That’s the approach Kredcor has applied for over 26 years, and it’s the approach that consistently delivers results for South African businesses.

Questions? Contact us directly at www.kredcor.co.za or use our Get a Free Quote form to start the conversation.

Authoritative External References

This article draws on the following official and authoritative South African sources:

- Debt Collectors Act 114 of 1998 (updated to 3 April 2024) — www.saflii.org

- Council for Debt Collectors (CFDC) — www.cfdc.org.za

- South African Government — www.gov.za/documents/debt-collectors-act

- National Credit Act 34 of 2005 — National Credit Regulator: www.ncr.org.za

- Consumer Protection Act 68 of 2008 — www.gov.za

─────────────────────────────────────────────────────────────────────────