The Dangerous Truth About No Collection No Fee: 7 Things Every South African Business Owner Must Know Before Signing

Quick Answer — What Does No Collection No Fee Mean?

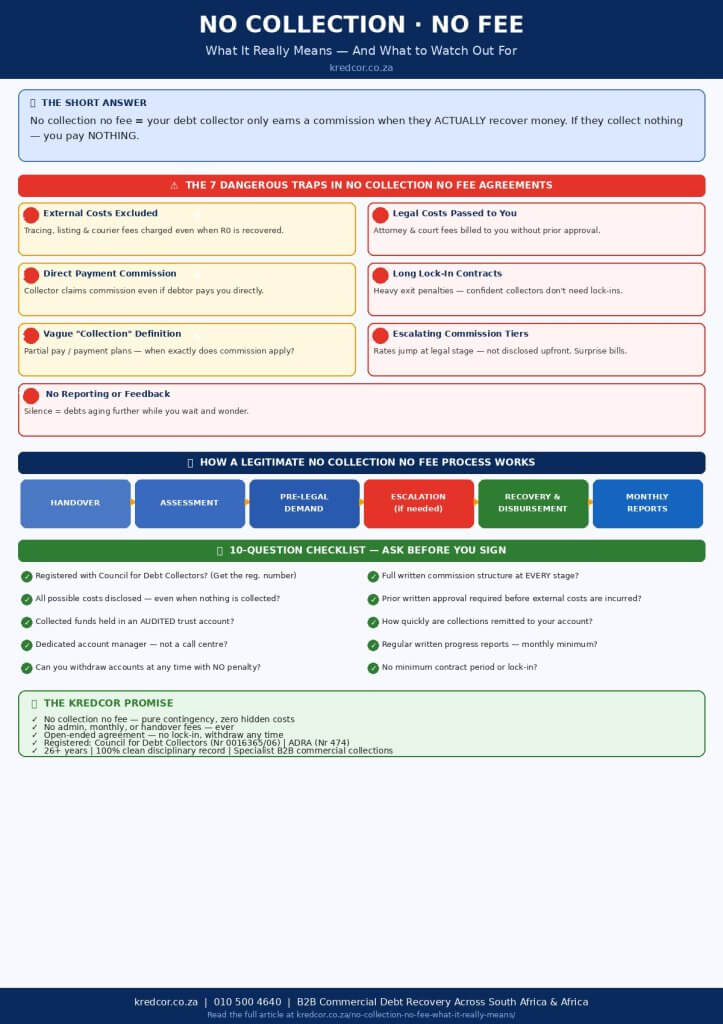

No collection no fee means your debt collector only earns a commission when they actually recover money from your debtor. If nothing is collected, you pay nothing. It is also called a contingency fee or no success no fee model. However — and this is critical — some agencies still charge separate fees for tracing, legal action, or administration, even when zero money is recovered. Before you sign anything, you need to know exactly which costs are and are not covered. This article breaks it all down for you.

Here’s a scenario that plays out every single day across South African businesses: you’ve been chasing a client for months. The invoice is overdue, the excuses are endless, and your cash flow is suffering. Then a debt collector promises you the magic words — no collection no fee. Zero upfront costs. Nothing to lose. Just sign here and we’ll get your money back.

It sounds perfect, doesn’t it? And in many cases, it genuinely is the best model for recovering B2B debt. But — and this is a big but — the phrase “no collection no fee” is not a standardised legal term in South Africa. What it means in practice varies significantly from one agency to another. Some firms genuinely operate on a pure contingency basis with complete fee transparency. Others use the phrase as a marketing hook, then layer in additional costs that catch you completely off guard.

After working with hundreds of SME owners, credit managers, financial managers, and CFOs across South Africa, our team at Kredcor has seen both ends of this spectrum. So, in this article, we’re going to pull back the curtain entirely. We’ll show you exactly what no collection no fee really means, where the hidden traps are, how to evaluate any contingency agreement before you sign, and what troubleshooting steps to take if things go wrong. This is the article we wish every business owner had read before they picked up the phone to a random collector.

📋 Table of Contents

- The Definitive Meaning of No Collection No Fee in South Africa

- How the No Collection No Fee Model Actually Works — Step by Step

- The 7 Dangerous Traps Hidden in No Collection No Fee Agreements

- What Legitimate No Collection No Fee Debt Collectors Look Like

- How to Evaluate a Contingency Fee Agreement — Before You Sign

- Our Team’s Experience: What We’ve Seen in Practice

- 5 Troubleshooting Tips When Your No Collection No Fee Deal Goes Wrong

- No Collection No Fee vs. Other Fee Models: A Straight Comparison

- The South African Legal Framework That Governs Contingency Collections

- Actionable Checklist: Questions to Ask Every Debt Collector

- Frequently Asked Questions

1. The Definitive Meaning of No Collection No Fee in South Africa

At its simplest, no collection no fee — also referred to as “no success no fee” or “contingency fee collection” — means that the debt collection agency ties its remuneration entirely to results. They don’t earn a cent in commission unless they recover money on your behalf. Consequently, the risk of trying to recover the debt shifts away from you and onto the collector.

This model is widely regarded as the fairest approach for creditors, because the interests of the creditor and the collector become perfectly aligned. The collector has every reason to work hard on your account, because their income depends directly on their success.

“The most powerful thing about a genuine no collection no fee model is that it makes the debt collector your partner, not just your service provider. Their success is your success. Their failure costs them too.”

Furthermore, the no collection no fee approach is particularly well-suited to the South African B2B environment, where many businesses hesitate to pursue overdue debtors because they fear throwing good money after bad. With contingency-based collection, that hesitation disappears. You have nothing to lose by submitting the account.

That said, the term has no single, legally defined meaning in South Africa. This means two different agencies can both claim to offer “no collection no fee” while operating very differently. Therefore, it is essential to understand precisely what the phrase covers — and, more importantly, what it does not.

2. How the No Collection No Fee Model Actually Works — Step by Step

Understanding the process helps you manage your expectations and spot anomalies early.

Here is how a legitimate no collection no fee debt recovery process typically unfolds:

- Handover of account: You submit the overdue account to the collector with supporting documentation — invoices, statements, delivery notes, signed agreements, communication records.

- Initial assessment: The collector evaluates the debtor’s profile, the age of the debt, and the likelihood of recovery. A good collector will flag unrecoverable debts early rather than waste everyone’s time.

- Pre-legal demand phase: The collector contacts the debtor directly — by phone, letter, email, and in person where necessary — to negotiate payment. This is where most debts are resolved, often quickly.

- Escalation if needed: If the debtor does not respond or refuses to pay, the collector may escalate to credit bureau listings, more formal letters of demand, or referral to attorneys for legal action. At this stage, external costs may arise — and this is precisely where transparency becomes critical.

- Recovery and disbursement: When money is collected, it flows either directly into your bank account or into the collector’s audited trust account, from which your share is paid after deducting the agreed commission.

- Reporting: A professional collector provides you with written progress reports throughout the process, so you’re never left in the dark.

This flow works beautifully when both parties understand it clearly from the start. Consequently, the onboarding conversation — where terms, commissions, and costs are discussed and agreed — is arguably the most important interaction you’ll have with your debt collector.

3. The 7 Dangerous Traps Hidden in No Collection No Fee Agreements

This is the section that most collectors would prefer you didn’t read. Based on our experience working across multiple industries in South Africa, these are the seven most common traps that catch businesses off guard — even when they thought they had a “no collection no fee” deal in place.

Trap 1: External Costs Are Excluded From the No Fee Promise

The commission is contingency-based, but the agent charges separately for tracing fees, credit bureau listings, skip-tracing, and the like. These costs apply whether or not money is recovered. Therefore, you can end up paying hundreds — or thousands — of rands in ancillary costs even when the collector recovers zero rands.

⚠ Red Flag: Any collector who cannot provide a written, itemised list of all potential costs within 24 hours of being asked should be treated with extreme caution.

Trap 2: Legal Action Costs Are Passed Through to You

When a matter escalates to court, sheriff fees, court filing fees, and attorney fees are real costs. In a genuine no collection no fee arrangement, the collector will discuss these costs with you upfront and get your prior approval before incurring them. Problematic collectors, however, simply instruct attorneys and then pass the bill to you — surprise!

Trap 3: Commission Applies Even on Amounts You Settle Directly

Some agreements include a clause stating that if your debtor contacts you directly and you accept payment without going through the collector, the collector still earns a commission. This is not unreasonable if clearly disclosed and agreed upfront. It becomes a trap when it’s buried in the fine print and you’ve never been warned about it.

Trap 4: Prohibitively Long Minimum Contract Periods

Some collectors lock you into a 12- or 24-month contract with heavy exit penalties. A genuinely confident collector — one who knows their service speaks for itself — doesn’t need to chain you to a contract. Look specifically for open-ended, no-obligation agreements that you can exit if you’re unsatisfied.

Trap 5: Unclear Definition of “Successful Collection”

Does a partial payment count as a successful collection? What if the debtor pays directly into your account? What if a payment plan is arranged but the debtor subsequently defaults? These definitions matter enormously, because they determine when the collector’s commission kicks in. Always insist on clear, written definitions of what constitutes a “collection” for commission purposes.

Trap 6: Commission Percentages That Escalate Without Warning

Some agreements include tiered commission structures that increase if the debt ages further or moves to legal stage. That’s not inherently wrong — legal collections are more expensive. But when these escalations aren’t clearly explained upfront, you can find yourself paying a 35% commission on a recovery that you expected to cost you 15%.

Trap 7: No Proper Reporting or Feedback Mechanism

You hand over ten accounts, and then you hear nothing for three months. When you eventually make contact, the collector tells you they couldn’t reach the debtors. This isn’t a trap in the contractual sense, but it is a practical trap — because in the meantime, your debts have aged further and your chances of recovery have dropped. Always insist on regular, written progress reports from day one.

Importantly, none of these traps exist at Kredcor. Our no collection no fee promise is exactly that — no hidden costs, no administration fees, no monthly fees, no handover fees. All external actions are pre-approved by you. You get a dedicated Relationship Manager, not a call centre. And you get written feedback regularly. But more on that shortly.

4. What Legitimate No Collection No Fee Debt Collectors Look Like

So, now that you know what to watch out for, let’s flip the coin. What should a genuinely trustworthy no collection no fee debt collector look like? Here’s the checklist our team has developed over 26 years in commercial debt recovery:

- Registered with the Council for Debt Collectors of South Africa. This is not optional. In South Africa, debt collectors must be registered under the Debt Collectors Act 114 of 1998. Ask for their registration number and verify it on the Council for Debt Collectors website.

- Members of a recognised industry association such as ADRA (Association of Debt Recovery Agents).

- Complete fee transparency upfront. A written, itemised fee schedule, including what happens if the matter goes legal, before you sign anything.

- No minimum contract period or penalties for withdrawing accounts. Open-ended agreements are the gold standard.

- A dedicated account manager, not a revolving door of call centre agents who have no context on your specific debtors.

- Regular written progress reports — monthly at minimum, with the ability to contact your manager at any time.

- An audited trust account for handling collected funds. This protects your money.

- Prior approval required for all external costs. No surprises on your invoice.

- Proven track record with blue-chip clients, verifiable testimonials, and a clean disciplinary record.

- POPIA compliant — they handle debtor data within the bounds of the Protection of Personal Information Act.

If you want a deeper dive into choosing the right partner, we strongly recommend reading our guide on how to choose the best debt collector in South Africa for your business — it covers every evaluation criterion in detail.

5. How to Evaluate a Contingency Fee Agreement — Before You Sign

Let’s get practical. You have a draft agreement in front of you from a debt collector who has promised you a no collection no fee service. Here is exactly what to look for before you put pen to paper.

Check the Commission Structure

What percentage do they charge, and does it vary by the age of the debt, the amount, or the stage of collection? Typical contingency rates in South Africa range from 10% to 25% for pre-legal collections, and may be higher for legal-stage accounts. Understand every tier before you sign.

Identify Every Possible Cost Item

Ask explicitly: “Can you please list every possible cost I could incur, even if money is not recovered?” A good collector will answer this question fully and in writing. Look specifically for tracing fees, credit bureau listing fees, postage/courier fees, court costs, sheriff fees, and attorney costs.

Read the Exit Clause

How do you exit the agreement if you’re unhappy? Is there a notice period? Are there penalties? Do they claim commission on accounts you withdraw? This clause tells you a great deal about how confident the collector is in their own service.

Check What Happens on Direct Payments

If your debtor pays you directly after the account has been handed to the collector, what are the commission implications? This needs to be crystal clear before you sign.

Verify the Trust Account

Ask: “Do you pay collected funds into an audited trust account?” and “How quickly will you remit my share of collections to my account?” Monthly remittances are standard. More frequent is better for your cash flow.

Additionally, if you’re weighing up whether to use a debt collector or an attorney, our article on how to choose between an attorney and a debt collector in South Africa will give you a clear, practical framework for that decision.

6. Our Team’s Experience: What We’ve Seen in Practice

I want to share something real with you here, because this isn’t just theory for us. We tested multiple approaches to contingency collection over the years, and the patterns we’ve observed are consistent.

We found that the businesses who suffer most from hidden-cost collection agreements are typically those who were so relieved to hear “no collection no fee” that they didn’t ask the follow-up questions. They signed quickly, handed over their accounts, and then received an invoice for R4,500 in “tracing and administration fees” three months later — with nothing collected.

Conversely, our team’s experience shows clearly that businesses who ask the five questions we listed in the previous section — before signing — almost never encounter surprise costs. The act of asking those questions also filters out the less reputable operators, who often become evasive or vague when pressed for written clarification.

One of the most revealing questions, in our experience, is this: “Can I withdraw an account at any time, with no penalty?” A collector who hesitates, adds conditions, or immediately redirects the conversation is showing you something important about how they operate.

We also found, consistently, that the businesses with the lowest debtor-day ratios and the healthiest cash flows are those who have a structured relationship with their debt collector — regular feedback calls, monthly reports reviewed by the credit manager, and a clear escalation protocol. No collection no fee works best when it’s part of a broader credit risk management strategy, not a last resort after all else has failed.

For a full breakdown of how the collection process works from invoice to judgement, read our comprehensive guide to the debt collection process in South Africa.

7. Five Troubleshooting Tips When Your No Collection No Fee Deal Goes Wrong

Even with the best intentions and a solid agreement, things can occasionally go sideways. Here are five concrete troubleshooting tips to navigate those situations:

Troubleshooting Tip 1: You’ve Received an Unexpected Invoice

First, don’t panic and don’t pay immediately. Pull out your written agreement and compare the invoice line by line against the fee schedule. If the cost was not disclosed in writing before the work was done, you are within your rights to dispute it. Request written documentation showing the specific clause that authorises each charge. If the collector cannot provide this, escalate your dispute to the Council for Debt Collectors.

Troubleshooting Tip 2: You Haven’t Received Any Feedback in Weeks

Send a formal written request (email is fine) asking for a full status update on all outstanding accounts, by a specific date. This creates a documented paper trail. If no response is forthcoming within five business days, escalate to senior management at the collection firm. If that also fails, consider lodging a formal complaint with ADRA.

Troubleshooting Tip 3: You Suspect the Collector Has Received Payment But Hasn’t Remitted to You

This is the most serious scenario. First, contact your debtor directly to establish whether they have made a payment. If they confirm they have, demand immediate written confirmation from the collector of receipt and an immediate remittance. In South Africa, misappropriation of trust account funds is a criminal offence. Report it to the Council for Debt Collectors without delay.

Troubleshooting Tip 4: The Collector Is Damaging Your Relationship With Your Client

If your debtor (who may be a valued ongoing client) complains that they’re being harassed or treated aggressively, this is a serious issue. Debt collectors are bound by the Code of Conduct under the Debt Collectors Act and may not use threatening, abusive, or misleading conduct. Raise this immediately with the collector and request a call log or copy of all communication sent to the debtor. If the behaviour is confirmed, report it to the Council for Debt Collectors.

Troubleshooting Tip 5: You Want to Withdraw an Account But the Collector Is Resisting

Refer again to your written agreement’s exit clause. If you have an open-ended agreement (as Kredcor operates), you can withdraw at any time, provided the terms are followed. If the agreement has a lock-in period, check the conditions carefully. Where there is a genuine dispute about your right to withdraw, seek independent legal advice. Never let a collection firm hold your accounts hostage.

💡 Pro Tip: Always maintain your own internal records of every account handed to a debt collector — date submitted, amount, debtor details, and any correspondence. These records are your safety net if a dispute arises.

8. No Collection No Fee vs. Other Fee Models: A Straight Comparison

To give you complete context, let’s compare the three main fee models used by debt collectors in South Africa:

| Fee Model | How It Works | Best For | Watch Out For |

|---|---|---|---|

| No Collection No Fee (Contingency) | Commission only on successful recovery | Most SMEs; all B2B creditors | Hidden external costs; unclear definitions |

| Flat Monthly Retainer | Fixed monthly fee regardless of results | Very high volume creditors | Ongoing costs even with zero recoveries |

| Per-Account Fee | Fixed fee per account submitted | Large debtors with predictable outcomes | High cost if recovery rate is poor |

For the overwhelming majority of South African SMEs, credit managers, and CFOs, the no collection no fee model offers the best risk-adjusted outcome. The key, as we’ve stressed throughout this article, is ensuring the model is genuinely transparent and genuinely contingency-based.

9. The South African Legal Framework That Governs Contingency Collections

Understanding the legal context gives you additional protection.

Here are the key legal instruments that apply to no collection no fee debt collectors operating in South Africa:

- Debt Collectors Act 114 of 1998: Requires all debt collectors to be registered with the Council for Debt Collectors. Sets out the Code of Conduct that all registered collectors must follow. Violations can result in suspension or deregistration.

- National Credit Act 34 of 2005: Primarily governs consumer credit, but some provisions affect B2B collections, particularly where personal guarantees are involved.

- Protection of Personal Information Act (POPIA): Governs how debtor data may be collected, processed, and stored. All creditors and collectors must comply.

- Prescription Act 68 of 1969: Debts in South Africa generally prescribe after three years if not acknowledged or pursued. Knowing this protects you from handing over prescribed debts — and paying commission on an unrecoverable account.

- Companies Act 71 of 2008 and the Insolvency Act: Relevant when a debtor becomes insolvent or enters business rescue proceedings.

Additionally, the Association of Debt Recovery Agents (ADRA) provides an additional layer of self-regulation for member firms. Choosing an ADRA member gives you additional recourse if things go wrong.

10. Actionable Checklist: 10 Questions to Ask Every Debt Collector Before You Sign

Print this out. Use it. It will save you money, time, and frustration.

- Are you registered with the Council for Debt Collectors? (Ask for the registration number.)

- What is your exact commission structure, at every stage of collections?

- What costs could I incur even if nothing is collected? Please provide this in writing.

- Will you get my prior written approval before incurring any external costs?

- Where will collected funds be held before being remitted to me? Is it an audited trust account?

- How frequently will you remit my collections to my bank account?

- Who will be my dedicated account manager? Will I always deal with the same person?

- How often will I receive written progress reports?

- Can I withdraw accounts at any time? Are there any penalties or commission implications?

- Do you have a minimum contract period? If so, what are the exit terms?

Kredcor’s answers to these questions: Yes, registered (Nr 0016365/06). Commission only on successful recoveries. Zero hidden costs — no admin, monthly, or handover fees. All external actions pre-approved by you. Audited trust account or directly into your account. Dedicated Senior Relationship Manager assigned. Monthly written reports. Open-ended agreement — no lock-in, no exit penalties. Over 26 years’ clean record with the Council for Debt Collectors.

11. Choosing the Right No Collection No Fee Partner in South Africa

The difference between a no collection no fee arrangement that works brilliantly and one that costs you more than it recovers comes down entirely to choosing the right partner. South Africa has hundreds of registered debt collectors. Some are exceptional. Others are not. The good news is that once you apply the due diligence framework we’ve laid out in this article, the right choice becomes much clearer.

At Kredcor, we’ve built our entire business model around the purest interpretation of no collection no fee: if we don’t collect, you don’t pay. Full stop. No tracing fee surprises. No monthly management fees. No contractual lock-in. We earn our worth by recovering your money, and we’ve been doing exactly that for over 26 years across Gauteng, the Western Cape, KwaZulu-Natal, the rest of Africa, and internationally. We are specialists in commercial and corporate debt recovery — B2B is our entire focus, not an afterthought.

Whether you’re dealing with a single stubborn debtor or a portfolio of overdue accounts, you deserve a partner who is transparent, ethical, registered, and results-driven. For a full overview of what to look for and expect from professional debt collectors in South Africa, we’ve created a comprehensive resource that covers everything from registration requirements to recovery timelines — it’s essential reading for any credit professional.

12. Keep Learning: More Resources to Help You Recover What’s Yours

Managing commercial credit risk, chasing overdue debtors, and navigating the South African collection landscape is genuinely complex. But it becomes significantly easier when you’re armed with the right knowledge. That’s why we publish in-depth, actionable articles every week — specifically for SME owners, credit managers, financial managers, and CFOs who want to do their jobs faster, smarter, and with greater confidence. From prescription of debt to emolument attachment orders, from POPIA compliance to the in duplum rule, our growing library covers the full landscape of B2B collections in South Africa. We invite you to explore all our free articles at kredcor.co.za/kredcor-articles/ — and bookmark it as your go-to resource for commercial credit management in South Africa.

Frequently Asked Questions About No Collection No Fee

Q: What does no collection no fee mean in South Africa?

A: No collection no fee means your debt collector only earns a commission when they successfully recover money from your debtor. If they collect nothing, you owe them no commission. However, be aware that some agencies still charge separate fees for tracing, legal action, or administration even when zero money is recovered. Always ask for a written, itemised list of all possible costs before you sign any agreement. A genuinely transparent no collection no fee arrangement has no hidden costs of any kind.

Q: What percentage does a no collection no fee debt collector charge in South Africa?

A: Contingency (no collection no fee) debt collectors in South Africa typically charge between 10% and 25% of the recovered amount for pre-legal collections, depending on the age, size, and complexity of the debt. Accounts that escalate to legal stage may attract higher commissions, reflecting the additional cost and complexity of court action. Always request the complete, tiered commission schedule in writing before submitting your first account.

Q: Are there hidden costs in a no collection no fee agreement?

A: There can be, yes — and this is one of the most important things to watch out for. While the collection commission is contingency-based, some agencies charge separately for tracing debtors, issuing letters of demand, credit bureau listings, or legal action. These costs may be charged even when no money is recovered. Therefore, always ask specifically: “What costs could I incur even if nothing is collected?” Get the full answer in writing. At Kredcor, the answer is simple: there are no administrative, monthly, or handover fees, and all external actions require your prior approval.

Q: Is no collection no fee better than paying a flat fee for debt collection?

A: For the vast majority of South African SMEs, the no collection no fee model is the better choice. It aligns the collector’s financial incentives with yours — they only earn when you earn. A flat-fee model means you pay regardless of results, which is costly if recovery rates are poor. That said, the no collection no fee model only delivers its full benefit when the commission structure is completely transparent and all potential costs are disclosed and agreed upfront. A clear, written agreement is non-negotiable.

About Kredcor

Kredcor is a specialist commercial debt recovery firm operating across South Africa and internationally. Registered with the Council for Debt Collectors (Reg Nr 0016365/06), Kredcor has maintained a 100% clean disciplinary record over 26+ years of operation. Kredcor operates exclusively on a no collection no fee basis — no hidden costs, no contractual obligations, no up-front payments. Contact Kredcor at 010 500 4640 or visit www.kredcor.co.za