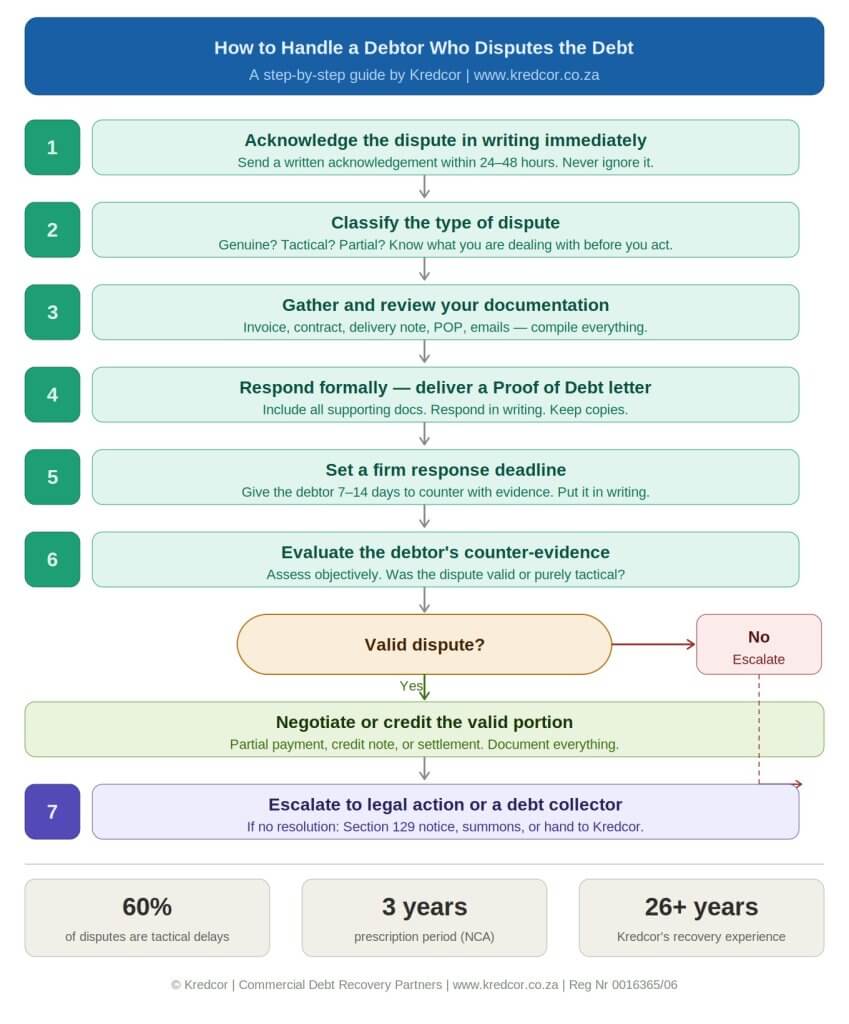

7 Powerful Steps On How To Handle a Debtor Who Disputes the Debt — Without Losing Your Leverage

A debtor disputes your invoice. Your stomach drops. You know the money is owed — you have the contract, the delivery note, the signed proof of delivery. But now the debtor is pushing back, claiming the invoice is incorrect, the goods were faulty, or worse — that they simply never agreed to these terms. What do you do next?

If you are an SME owner, credit manager, financial manager, or CFO in South Africa, this scenario is frustratingly familiar. The good news is that when you handle a debtor who disputes the debt correctly — systematically, calmly, and backed by documentation — you dramatically improve your chances of recovering every cent. In this guide, we walk you through exactly how to do that, step by step.

We also address the five most common mistakes businesses make when a dispute lands on their desk, and we give you a clear, no-fluff framework to protect your cash flow and your business relationships — at the same time.

QUICK ANSWER:

When a debtor disputes the debt, the correct process is to:

(1) acknowledge the dispute in writing,

(2) classify whether the dispute is genuine or tactical,

(3) gather your documentation,

(4) respond with a formal Proof of Debt,

(5) set a firm response deadline,

(6) evaluate their counter-evidence, and

(7) escalate to legal action or a professional debt collector if no resolution is reached.

Every step must be documented.

Table of Contents

- Why Debtors Dispute Debts — and What It Really Means for Your Business

- Step 1: Acknowledge the Dispute in Writing — Immediately

- Step 2: Classify the Type of Dispute

- Step 3: Gather and Review Your Documentation

- Step 4: Respond Formally — The Proof of Debt Letter

- Step 5: Set a Firm Deadline for the Debtor’s Response

- Step 6: Evaluate the Debtor’s Counter-Evidence

- Step 7: Escalate — Legal Action, Mediation, or a Professional Debt Collector

- 5 Troubleshooting Tips for Stubborn Disputes

- The Legal Framework: What South African Law Says

- How to Dispute-Proof Your Credit Agreement

- FAQ: How to Handle a Debtor Who Disputes the Debt

Why Debtors Dispute Debts — and What It Really Means for Your Business

Before you can effectively handle a debtor who disputes the debt, you need to understand why the dispute is happening in the first place. Not every dispute is the same, and treating them all identically is one of the costliest mistakes a credit manager can make.

In our experience at Kredcor — with over 26 years of commercial debt recovery across South Africa — we have found that most debt disputes fall into one of three categories:

- Genuine disputes: The debtor has a legitimate concern — perhaps the goods were defective, the service was not delivered as agreed, or the invoice contains an error. These disputes deserve careful attention and, when valid, a fair resolution.

- Tactical disputes: The debtor knows they owe the money but raises a dispute purely to buy time or delay enforcement. This is, frankly, the most common type. Our team has found that roughly 60% of debt disputes in the B2B space are tactical in nature.

- Partial disputes: The debtor agrees they owe something, but disputes the full amount — perhaps contesting interest charges, penalties, or a specific line item on the invoice.

Understanding which category you are dealing with changes everything about how you respond. Moreover, it determines whether you need to act quickly and firmly, or whether you need to genuinely review your own records before pushing forward.

“A dispute is not a stop sign. It is a negotiation tactic, a genuine concern, or both — and the skilled credit professional knows the difference within the first 48 hours.” — Kredcor’s debt recovery team

Furthermore, from a legal perspective, how you respond to a dispute matters as much as the dispute itself. South African courts look favourably on creditors who can demonstrate that they engaged with the dispute process professionally and in good faith before resorting to litigation.

Step 1: Acknowledge the Dispute in Writing — Immediately

The very first thing you must do when a debtor disputes the debt is acknowledge it — in writing, within 24 to 48 hours. This may sound obvious, but you would be surprised how many businesses ignore a dispute or simply keep sending invoices as if nothing happened.

Why does acknowledgement matter so much? Because it:

- Creates a paper trail from the very beginning of the dispute process.

- Demonstrates that you are engaging in good faith — which carries significant weight if the matter later goes to court.

- Buys you time to gather your documentation without appearing to ignore the debtor.

- Prevents the debtor from later claiming you failed to respond.

Your acknowledgement letter does not need to be long or complicated. However, it must confirm that you have received their dispute, state that you are reviewing the matter, and indicate when they can expect your formal response.

What your acknowledgement letter should include:

- Date and reference number of the disputed invoice

- A clear statement that you have received and noted their dispute

- A commitment to respond within a specific timeframe (typically 5–10 business days)

- A polite but firm reminder that the underlying debt remains payable pending resolution

- Your contact details for further correspondence

Keep a copy of everything. Always send correspondence via email (so you have a time-stamped record) and follow up with a registered letter for significant amounts. This discipline is something our team at Kredcor consistently emphasises when working with credit managers — and it pays off every single time.

Step 2: Classify the Type of Dispute

Once you have acknowledged the dispute, your next priority is to classify it accurately. This classification drives every subsequent decision you make.

Here is a practical framework we use at Kredcor:

Indicators of a genuine dispute:

- The debtor raised the issue promptly after receiving the invoice (not months later when you’ve started collection action).

- They can specify exactly what is wrong — a particular line item, a missing delivery, a quality issue.

- They have supporting documentation — a returns note, a complaint email, a counter-delivery record.

- The debtor has a strong prior payment history with you.

Indicators of a tactical dispute:

- The dispute surfaces only after you have sent a demand letter or handed the account to collections.

- The reason given is vague — “we’re not happy with the service” with no specifics.

- The debtor has a history of late payments or prior disputes that conveniently evaporated after you escalated.

- The disputed amount is exactly the total amount owed — with no partial payment offered.

Classifying the dispute honestly also requires you to review your own records with an open mind. I have seen situations where our clients at Kredcor were convinced a dispute was purely tactical — only to discover on review that an invoice had indeed been duplicated, or that a credit note had never been applied. Your credibility depends on getting this right.

Step 3: Gather and Review Your Documentation

Documentation is the single most powerful tool in your arsenal when you handle a debtor who disputes the debt. Without it, even a completely valid claim becomes difficult to enforce.

At this stage, you need to compile and review every piece of relevant documentation:

- The original signed contract or credit application

- The invoice(s) in dispute — with full line-item detail

- Delivery notes, proof of delivery (POD), or job completion certificates

- Purchase orders from the debtor

- Email correspondence confirming the order, delivery, or service

- Any signed acceptance documents

- Bank proof of payment for any partial payments received

- Your terms and conditions, particularly those relating to disputes, payment terms, and interest

Once you have gathered these documents, review them critically. Ask yourself: If this matter went to court today, would my documentation convincingly support my claim? If the honest answer is “not entirely,” address the gaps before you escalate.

This is also the right moment to check whether the debt is at risk of prescription. Under the Prescription Act 68 of 1969, most commercial debts prescribe after three years from when they became due and payable. If the debt is approaching that mark, you need to interrupt prescription immediately — either by getting the debtor to acknowledge the debt in writing, making a payment, or issuing summons.

For a comprehensive breakdown of how prescription works in South Africa and how to interrupt it, read our detailed guide: The Definitive Guide to Prescription of Debt in South Africa.

Step 4: Respond Formally — The Proof of Debt Letter

After reviewing your documentation, you are ready to issue your formal response. This is often called a Proof of Debt letter or a Verification of Debt response, and it is arguably the most important document in the entire dispute process.

Your Proof of Debt letter should be:

- Professional, factual, and free of emotional language

- Supported by attachments — attach copies of all relevant documentation

- Specific — address each point raised in the debtor’s dispute, point by point

- Clear about the total amount claimed, including any interest that has accrued

- Firm — restate that the debt is valid and remains payable

A note on interest: the In Duplum Rule

When calculating the total amount owed, make sure you understand how the In Duplum Rule applies. This rule limits the amount of interest that can be claimed to a maximum of the outstanding capital amount — in other words, interest cannot exceed the original debt. Exceeding this limit in your claim can undermine your position.

For a detailed explanation of how the In Duplum Rule works and how it affects your collections, see our guide: The In Duplum Rule Explained: How Interest Caps Powerfully Affect Your Collections.

Step 5: Set a Firm Deadline for the Debtor’s Response

Once you have delivered your Proof of Debt, you must set a firm, reasonable deadline for the debtor to respond with their counter-evidence. This is a step many creditors skip — and it costs them dearly.

Without a deadline, the dispute simply drags on indefinitely. The debtor keeps stalling, your cash flow suffers, and the matter grows increasingly difficult to resolve. By contrast, a clear deadline:

- Signals that you are serious and organised.

- Creates a clear timeline that a court will later be able to follow.

- Puts pressure on the debtor to either produce evidence or admit they have none.

- Allows you to plan your next escalation step with confidence.

A reasonable response deadline in South Africa is typically 7 to 14 business days from the date your Proof of Debt letter is delivered. For larger amounts or more complex disputes, 21 days may be appropriate. Whatever deadline you set, stick to it — and document when it passes.

“Setting a deadline is not aggressive. It is professional. A creditor who lets a dispute drift indefinitely loses both leverage and cash flow.” — Kredcor advisory team

Step 6: Evaluate the Debtor’s Counter-Evidence

When the debtor responds with their counter-evidence, evaluate it carefully and objectively. Resist the natural temptation to dismiss it out of hand, especially if you are frustrated by the delay. An honest evaluation protects you legally and commercially.

Ask these questions when assessing the debtor’s response:

- Does their documentation actually support their position, or is it vague and unsupported?

- Is their dispute consistent with what they told you at the outset, or has it evolved and shifted?

- Does their counter-evidence reveal a genuine error on your side that needs to be corrected?

- Have they offered any partial payment — which would typically indicate they accept at least part of the debt?

- Is their response within the deadline you set, or did they ignore it entirely?

If the debtor’s counter-evidence is convincing, then the right commercial decision may be to negotiate a settlement, issue a credit note for a disputed portion, or agree on a revised payment arrangement. Resolving a genuine dispute fairly — even if it costs you something — preserves the business relationship and your reputation in the market.

However, if the counter-evidence is weak, vague, or simply absent, that is a strong signal to escalate without further delay.

Step 7: Escalate — Legal Action, Mediation, or a Professional Debt Collector

If Steps 1 through 6 have not produced a resolution, it is time to escalate. This is not a failure — it is simply the next logical step in a professional debt recovery process.

You have three main escalation options in South Africa:

Option 1: Mediation or alternative dispute resolution

For ongoing business relationships that you want to preserve, mediation through the AFSA (Arbitration Foundation of Southern Africa) or a similar body can be a cost-effective way to resolve the dispute without the expense and time of litigation. Both parties present their case to a neutral mediator, and the process is typically far faster than court proceedings.

Option 2: Legal action through the courts

For clear-cut cases where your documentation is solid and the debtor’s dispute lacks merit, issuing summons through the Magistrate’s Court (for claims up to R400,000) or the High Court (for larger claims) is often the most effective path. Before doing so, you are typically required to issue a Section 129 notice under the National Credit Act — or a Letter of Demand — giving the debtor one final opportunity to resolve the matter.

To understand exactly what a Section 129 notice involves and when it applies, read our guide: Ultimate Guide to the Section 129 Notice: What It Is and Why It Matters.

Option 3: Engage a professional debt collector

For most SMEs and credit managers, handing a disputed account to a professional, registered debt collector is the most practical and cost-effective option. A specialist debt collector brings:

- Deep experience in identifying and countering tactical disputes

- A professional distance that removes emotion from the negotiation

- Legal expertise to navigate the collections process correctly

- Networks and tools for tracing debtors who go quiet

- A higher recovery rate than in-house pursuit in most cases

Kredcor is registered with the Council for Debt Collectors (Reg Nr 0016365/06) and has been recovering commercial debts across South Africa for over 26 years. Our team operates in Gauteng, the Western Cape, KwaZulu-Natal, and across Africa. We understand disputed debt intimately — because we deal with it every single day.

5 Troubleshooting Tips for Stubborn Disputes

Troubleshoot Tip 1: The debtor keeps moving the goalposts

This is a classic sign of a tactical dispute. Every time you address one objection, a new one appears. The solution: send a comprehensive Proof of Debt that addresses every conceivable objection simultaneously, and include a final deadline after which you will proceed to enforcement without further correspondence.

Troubleshoot Tip 2: The debtor claims they never received the goods or services

If you have a signed POD, you are in a strong position — produce it. If you do not have one, this is a valuable lesson for future transactions. In the short term, try to produce any other evidence of delivery: a delivery driver’s record, GPS data, CCTV, or a third-party courier’s confirmation. Digital delivery confirmation emails are also powerful evidence.

Troubleshoot Tip 3: The debtor disputes the interest or penalty charges

Interest and penalty disputes are common, particularly when the original contract did not clearly state the interest rate or penalty terms. Review your original credit agreement carefully. If the terms were clearly disclosed, you are entitled to enforce them — subject to the In Duplum Rule and the National Credit Act. If the terms were not properly disclosed, you may need to recalculate. Going forward, always ensure your credit application clearly sets out all financial charges.

Troubleshoot Tip 4: The debtor claims the debt has prescribed

This is a serious defence that requires careful analysis. Check when the debt became due and payable, and whether anything has happened to interrupt prescription — a partial payment, written acknowledgement, or prior demand. If you are unsure, seek legal advice promptly. Do not assume the debt has not prescribed without checking the facts.

Troubleshoot Tip 5: The debtor has gone silent after raising the dispute

Silence is not resolution. If a debtor raises a dispute and then goes quiet, do not assume the matter is settled. Continue to follow up in writing at regular intervals. After a reasonable period — typically 14 to 21 days — treat the matter as unresolved and proceed to the next escalation step. Document every follow-up attempt.

The Legal Framework: What South African Law Says

When you handle a debtor who disputes the debt in South Africa, several key pieces of legislation and common law principles apply. A basic understanding of these laws strengthens your position significantly.

The National Credit Act (NCA)

The NCA governs credit agreements with natural persons and certain juristic persons below specific asset/turnover thresholds. If the NCA applies, the debtor has specific rights to dispute the debt, and you must follow the prescribed dispute resolution process — including issuing a Section 129 notice before commencing legal proceedings. Failure to follow this process can invalidate your action.

The Prescription Act 68 of 1969

As noted earlier, most commercial debts prescribe after three years. This means the debtor can raise prescription as a complete defence if you have allowed the debt to lapse without taking action or obtaining acknowledgement. Critically, prescription begins to run from the date the debt became due — not from the date of the invoice.

The Consumer Protection Act (CPA)

For disputes involving the quality of goods or services supplied to consumers, the CPA gives the consumer the right to request a repair, replacement, or refund within certain timeframes. As a supplier, you need to understand when this right applies and respond accordingly.

Common law and the law of contract

Beyond legislation, the general principles of South African contract law apply. A valid credit agreement requires offer, acceptance, and consideration. If the debtor can prove that one of these elements is missing, the agreement — and therefore the debt — may be unenforceable. This is why your written contract and credit application are so critical.

For authoritative legal guidance, see the National Credit Regulator (NCR) and the South African Law Reform Commission.

How to Dispute-Proof Your Credit Agreement

The best way to handle a debtor who disputes the debt is to make disputes far harder to raise in the first place. Our team at Kredcor has reviewed hundreds of commercial credit agreements over the years, and the businesses that experience the fewest successful disputes are those that invested in watertight credit documentation upfront.

Here is what your credit agreement should include to minimise future disputes:

- Clear, unambiguous payment terms — amount, due date, and consequence of late payment

- Explicitly stated interest rate and penalty clauses (correctly disclosed under the NCA where applicable)

- A clear description of goods or services provided, linked to a schedule or scope of work

- A dispute resolution clause — specifying how disputes must be raised (in writing, within a specific timeframe) and how they will be resolved

- Confirmation that the debtor has read and understood the terms — ideally with a signed acknowledgement

- Jurisdiction clause specifying the applicable court

- A certificate of balance clause — allowing you to produce a certificate signed by a manager as prima facie proof of the amount owed

- Signed by an authorised signatory — check that the person signing has authority to bind the company

Alongside your credit agreement, always obtain and retain a signed credit application form, completed in full, with the debtor’s company registration details, VAT number, banking details, and the names of directors or signatories. This document becomes critical if the debtor later disputes identity or authority.

When to Call in the Professionals

There comes a point in every stubborn dispute where the smartest commercial decision is to hand the matter to specialists. Continuing to manage a disputed debt in-house — after all the steps above have been exhausted — diverts valuable management time and rarely improves the outcome.

Kredcor works with SME owners, credit managers, and CFOs across South Africa to recover disputed commercial debts professionally and ethically. Whether you need a registered debt collectors in South Africa to manage the recovery process end-to-end, or simply want guidance on how to proceed with a particular dispute, our team is ready to help. We are registered with the Council for Debt Collectors (Reg Nr 0016365/06) and have been doing this for over 26 years.

Further Reading

We publish regular, in-depth articles on debt recovery, credit management, and South African collections law at www.kredcor.co.za/kredcor-articles/. Whether you’re tackling prescription issues, navigating ethical collections, or trying to understand your legal options, you’ll find clear, practical guidance written specifically for South African credit professionals.

FAQ: How to Handle a Debtor Who Disputes the Debt

Q1: What should I do first when a debtor disputes a debt?

The very first step is to acknowledge the dispute in writing — within 24 to 48 hours. Do not ignore it, do not keep sending invoices as if nothing has changed, and do not immediately threaten legal action. Instead, confirm you have received the dispute, state that you are reviewing the matter, and indicate when you will provide a formal response. This creates a professional paper trail from the outset and demonstrates good faith if the matter later goes to court.

Q2: Can a debtor legally refuse to pay while a dispute is pending?

In short: it depends. Under South African law, raising a dispute does not automatically suspend the obligation to pay. However, if the National Credit Act applies and the debtor has followed the correct dispute process, certain protections apply. For standard commercial credit agreements between businesses, the debt generally remains payable during a dispute — unless the dispute directly challenges the validity of the underlying contract or the amount claimed. Legal advice is recommended for complex cases.

Q3: How do I know if a dispute is genuine or tactical?

Look at the timing, specificity, and evidence behind the dispute. A genuine dispute is typically raised promptly, with specific detail, supported by documentation, and by a debtor with a clean payment history. A tactical dispute tends to surface only when collection action begins, uses vague language, lacks supporting evidence, and often involves a debtor with a prior history of payment delays. Our experience at Kredcor suggests that roughly 60% of B2B debt disputes in South Africa are tactical in nature — but every case must be assessed individually.

Q4: At what point should I hand a disputed debt to a debt collector?

You should consider handing the matter to a professional debt collector when: (1) your own attempts to resolve the dispute have failed after a reasonable period, (2) the debtor has provided counter-evidence that you believe is weak or unfounded, (3) the matter is approaching prescription, or (4) managing the dispute in-house is consuming disproportionate management time. A registered debt collector brings specialist experience, legal knowledge, and professional distance that typically produces better outcomes — and frees your team to focus on the business.

The Bottom Line

Knowing how to handle a debtor who disputes the debt is one of the most valuable skills a credit professional or business owner can develop. When you follow a structured, documented process — acknowledging the dispute, classifying it, gathering evidence, responding formally, setting deadlines, evaluating counter-evidence, and escalating when necessary — you protect your cash flow, your legal position, and your business reputation simultaneously.

The key is to act quickly, document everything, and never let a dispute drift without a clear resolution plan.

Kredcor is here to help. Contact us at www.kredcor.co.za for a free, no-obligation discussion about any disputed commercial debt in South Africa.© Kredcor | South Africa’s Commercial Debt Recovery Partners | Reg Nr 0016365