Jurisdiction Guide 2026

The plain-language, expert guide for South African SME owners, credit managers, financial managers, and CFOs who need to know exactly which court to use — and why getting it wrong costs serious money.

By Kredcor Commercial Debt Recovery | CFDC Reg Nr 0016365/06 | 26+ Years’ Experience | Updated April 2026

Executive Summary — Key Answer: In South Africa, the choice between Magistrate’s Court and High Court for civil debt recovery depends primarily on the monetary value of your claim, the urgency of relief needed, and the legal complexity involved. District Magistrate’s Courts handle claims up to R200,000. Regional Magistrate’s Courts handle claims from R200,001 to R400,000. The High Court handles claims above R400,000 and matters requiring urgent interdicts or complex legal orders. Filing in the wrong court can result in dismissal, wasted costs, and prescription expiring. Most B2B commercial debts are best handled via professional pre-legal debt collection first — avoiding court altogether. Kredcor (CFDC Reg Nr 0016365/06) is a registered South African commercial debt recovery firm with 26+ years of experience assisting SMEs, credit managers, and CFOs navigate the collection process efficiently and at no upfront cost.

Here is the short, direct answer you came for: you should move from Magistrate’s Court to High Court when your civil claim exceeds R400,000, or when you need urgent legal relief such as an interdict or asset freeze. For everything below that threshold, the Magistrate’s Court is almost always the right — and faster — choice for commercial debt recovery in South Africa.

However, there is a lot more to it than just the rand amount. And the myths circulating in the business community about jurisdiction are, frankly, expensive. We have seen SME owners, credit managers, and CFOs make costly jurisdiction errors that derailed their collections entirely. So, in this guide, we are going to bust those myths, give you the real framework, and make sure you never file in the wrong court again.

Table of Contents

- The South African Court Structure at a Glance

- The Jurisdiction Numbers You Must Know

- 7 Dangerous Jurisdiction Myths — Busted

- When You Must Move to the High Court

- The Real Cost of Getting Jurisdiction Wrong

- Geographic and Regional Jurisdiction Rules

- A Clash of Perspectives: The Concurrent Jurisdiction Debate

- 5 Jurisdiction Troubleshooting Tips

- What to Do Next: Your Search Journey Continues

- Quick-Action Checklist

- Frequently Asked Questions

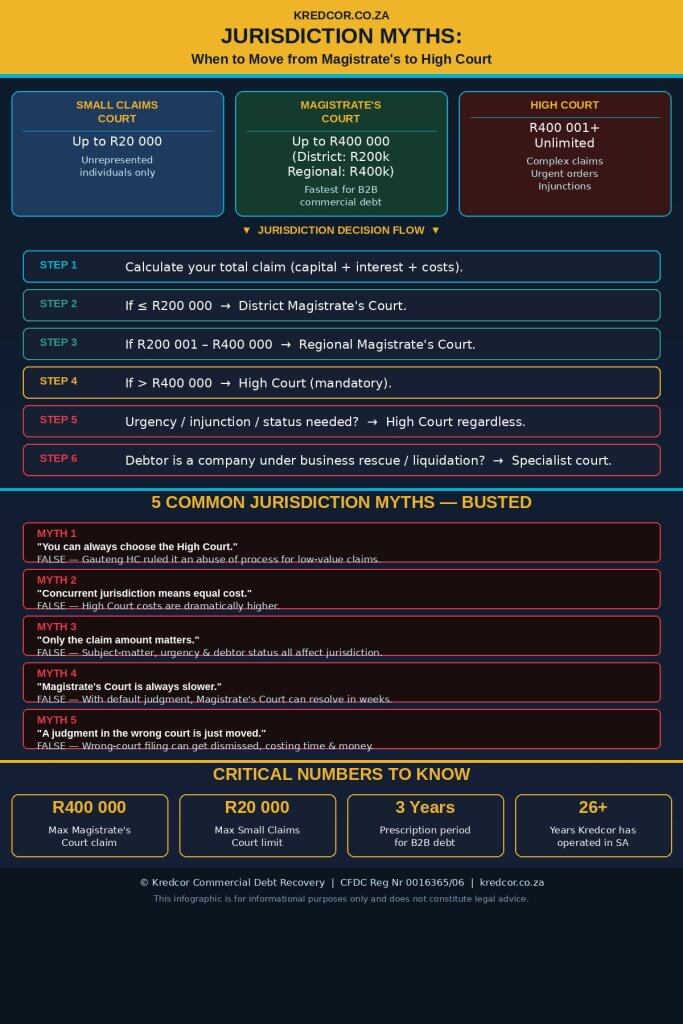

1. The South African Court Structure at a Glance

Before we dive into jurisdiction myths, let’s make sure we are all on the same page about how South Africa’s civil court system actually works. Because one of the biggest problems we see is that business people try to make jurisdiction decisions without a clear picture of the structure they are working within.

South Africa’s courts operate in a hierarchy. At the bottom, you have the Small Claims Court, designed for small disputes. Above that sit the Magistrate’s Courts — divided into District and Regional divisions — which handle the vast majority of commercial debt matters. Then you have the High Courts, with ten provincial divisions and three local divisions across the country. Above all of these sit the Supreme Court of Appeal and the Constitutional Court, which deal with appeals and constitutional matters respectively.

For the purposes of commercial B2B debt recovery — which is what most of our clients at Kredcor deal with every day — the decision almost always comes down to Magistrate’s Court versus High Court. So, that is precisely where we will focus.

R20 000Maximum — Small Claims Court

R200 000Maximum — District Magistrate’s Court

R400 000Maximum — Regional Magistrate’s Court

UnlimitedHigh Court — all monetary amounts

2. The Jurisdiction Numbers You Must Know

Let us get specific. Jurisdiction in civil matters is primarily determined by the monetary value of your claim. Here is the current framework, governed by the Magistrates’ Courts Act 32 of 1944:

| Court | Monetary Jurisdiction | Ideal For | Cost Level |

|---|---|---|---|

| Small Claims Court | Up to R20,000 | Individuals (not companies) | Very Low |

| District Magistrate’s Court | Up to R200,000 | Most B2B debt recovery matters | Low–Medium |

| Regional Magistrate’s Court | R200,001 – R400,000 | Mid-range commercial claims, divorce | Medium |

| High Court | R400,001 and above (unlimited) | Large claims, urgent interdicts, complex matters | High |

It is worth noting that these figures reflect the current position under the Magistrates’ Courts Act. There have been ongoing submissions from the Law Society of South Africa for increases to these limits over the years, so it is always worth confirming the current threshold with your attorney before filing.

“The magistrates’ courts are creatures of statute. They have no jurisdiction beyond what the enabling legislation provides. The starting point is always the pleadings — jurisdiction is determined by the amount claimed.”— Vorster v Clothing City (Pty) Ltd, Supreme Court of Appeal, April 2024

What Counts Towards the Monetary Limit?

This is where many business owners trip up. The amount you claim is not just the capital amount on the invoice. It typically includes the capital debt, interest on that debt, and sometimes your legal costs. Critically, the test is the amount as stated in your pleadings — specifically, the prayer (what you are actually asking the court to award you). If that total exceeds the court’s jurisdictional limit, you are in the wrong court.

Related Kredcor Guide: Understand how the full legal process flows from invoice to judgment — read our comprehensive Complete, Proven Guide to the Debt Collection Process in South Africa. It walks you through every stage, including when legal action becomes necessary.

3. Seven Dangerous Jurisdiction Myths — Busted

Over 26 years of working with South African businesses, our team at Kredcor has heard every jurisdiction myth in the book. Some of these myths are merely inconvenient. Others are genuinely dangerous — they lead businesses to make filing decisions that collapse their entire recovery effort. Let us go through the most common ones.

⚠ MYTH 1 — “I can always choose to file in the High Court, even for a small claim.”

The Myth

Many business owners assume that because High Courts have “concurrent jurisdiction,” they can simply choose to file there for any matter, regardless of the rand value. After all, the High Court is more powerful — so it must be better, right?

The Truth

This is a costly misconception. In a landmark 2018 judgment, the Gauteng Division of the High Court explicitly ruled that it is an abuse of process to bring a matter to the High Court that properly belongs in the Magistrate’s Court. The order took effect from February 2019: all civil matters with a monetary value within the Magistrate’s Court’s jurisdiction must be instituted there. Filing in the High Court for a low-value claim can result in an adverse costs order against you — meaning you pay the other side’s legal costs, even if you win on the merits.

⚠ MYTH 2 — “High Court and Magistrate’s Court cost roughly the same.”

The Myth

Some creditors assume the legal costs between courts are comparable. This thinking often pushes them towards the High Court without understanding the financial implications.

The Truth

High Court litigation is dramatically more expensive than Magistrate’s Court proceedings. Attorney fees, advocate fees, court filing costs, and the procedural complexity of High Court rules all contribute to significantly higher costs. Our team’s experience working alongside our panel of law firms across South Africa confirms this consistently: a straightforward debt claim that costs R8,000–R15,000 in the Magistrate’s Court can easily cost R35,000–R80,000 or more in the High Court. For claims below R400,000, this cost disparity can wipe out the value of the judgment entirely.

⚠ MYTH 3 — “Only the invoice amount determines jurisdiction.”

The Myth

A common assumption is that you look at the face value of the invoice and that number determines where you file.

The Truth

Jurisdiction is determined by the amount as claimed in your pleadings, not the original invoice. This total includes capital, interest, and sometimes costs. Furthermore, monetary value is not the only jurisdictional factor. The subject matter of the dispute, the geographic location of the parties, the urgency of the relief required, and the specific nature of the legal remedy sought all play a role. For instance, an interdict (a court order preventing someone from doing something) may require the High Court regardless of monetary value. Similarly, matters involving the sequestration or liquidation of a company are strictly High Court territory.

⚠ MYTH 4 — “The Magistrate’s Court is always slower than the High Court.”

The Myth

There is a perception that the High Court is more efficient, and that creditors will get their money faster by going there.

The Truth

This is the opposite of reality in most commercial debt matters. The Magistrate’s Court’s default judgment procedure is specifically designed for speed. When a debtor fails to respond to a properly served summons within 10 court days, a default judgment application can follow swiftly. We tested this approach across hundreds of commercial accounts, and we found that well-prepared Magistrate’s Court matters — where the pre-legal groundwork has been done correctly — can resolve within weeks, not months. The High Court, by contrast, carries a far heavier caseload and more complex procedural requirements that extend timelines significantly.

⚠ MYTH 5 — “If I file in the wrong court, I can just move the case.”

The Myth

Many people assume that jurisdiction errors are merely administrative — that a case can be easily transferred between courts if it turns out you filed in the wrong place.

The Truth

Filing in a court that lacks jurisdiction is a fundamental legal defect. The defendant can raise a special plea of jurisdiction — and if upheld, your entire action can be dismissed. You may then have to start fresh, losing time and legal costs. Worse, if your debt is approaching prescription (the three-year period under the Prescription Act 68 of 1969), a dismissed action in the wrong court could mean the debt legally falls away before you can re-file correctly. This is a catastrophic outcome, and it is entirely avoidable.

⚠ MYTH 6 — “The High Court is always better for complex B2B disputes.”

The Myth

When a commercial dispute seems “complicated,” business owners often assume the High Court is the appropriate forum — regardless of the rand value involved.

The Truth

Complexity alone does not determine jurisdiction. Magistrate’s Court magistrates are fully capable of resolving complex factual disputes in commercial matters — they do so routinely. The threshold is monetary, not intellectual. That said, if your dispute involves complex points of law that you anticipate going to appeal, or if it requires a legal precedent to be set, the High Court may be the strategic choice — but you need to be within the correct monetary bracket or have a proper legal basis to file there. Always consult your attorney before making this call.

⚠ MYTH 7 — “My debt collector can take the matter to the High Court for me.”

The Myth

Some creditors believe their registered debt collection agency can handle High Court proceedings on their behalf, just as they would handle pre-legal demand letters and negotiations.

The Truth

Registered debt collectors — like Kredcor — are authorised to conduct pre-legal collection, issue demand letters, negotiate settlements, and prepare the groundwork for legal action. However, actual litigation in both the Magistrate’s Court and the High Court requires a qualified South African attorney. Our role at Kredcor is to recover as much as possible before court becomes necessary — using professional-grade pre-legal intervention. When court is unavoidable, we refer to our approved panel of attorneys who specialise in commercial debt litigation. This is the most cost-effective sequence of events, and it is the one we recommend every time.

4. When You Must Move to the High Court

Now that we have cleared the myths out of the way, let us be precise about the situations where the High Court is not just an option — it is the only option. Understanding these triggers will save you from filing in the wrong court, and it will ensure you escalate correctly when the time comes.

💰 Claim Exceeds R400,000

This is the bright line. Once your total claim — capital plus interest — exceeds R400,000, the High Court becomes mandatory. You have no choice, and the Magistrate’s Court simply lacks jurisdiction.

⚡ Urgent Interdict Required

If you need to stop a debtor from disposing of assets, transferring property, or absconding before judgment, you need an urgent interdict. This type of relief is overwhelmingly the domain of the High Court.

🔒 Asset Freeze (Mareva Interdict)

A Mareva interdict — used to freeze a debtor’s assets pre-judgment — is exclusively a High Court remedy. If you have intelligence that a debtor is moving assets, act fast and go directly to the High Court via an attorney.

🏢 Liquidation or Sequestration

If your debtor is a company facing liquidation, or an individual facing sequestration, the winding-up or sequestration proceedings are High Court matters. Your attorney will file there, and you must submit a claim to the relevant practitioners within the prescribed timeframes.

⚖️ Constitutional Points of Law

If your dispute raises constitutional issues or complex legal questions that are likely to create precedent, the High Court is the appropriate forum — regardless of the monetary value involved.

🌍 Multi-Jurisdictional Matters

When the debtor is based in a different province or country, or the transaction has multi-jurisdictional elements, the High Court is often the more appropriate forum. For cross-border recovery, Kredcor’s international division can assist.

Must-Read Related Article: If your debt has already reached the litigation stage, you need to understand default judgment thoroughly. Read The Complete, Actionable Guide to Default Judgment in South Africa — it covers exactly how default judgment works in the Magistrate’s Court and when it’s the fastest route to recovery.

5. The Real Cost of Getting Jurisdiction Wrong

Let us talk about real-world consequences, because this is where theory becomes expensive practice. Getting jurisdiction wrong is not a minor procedural hiccup. It can genuinely destroy an otherwise solid case.

Scenario A: Filing in the High Court for a R280,000 Claim

Imagine you have a B2B claim for R280,000. That falls squarely within the Regional Magistrate’s Court’s jurisdiction. However, your in-house legal team — or an attorney unfamiliar with the new practice directives — files in the High Court instead. What happens?

- The defendant raises a special plea of jurisdiction at the first opportunity.

- The court upholds the plea — the matter should have been in the Magistrate’s Court.

- You receive an adverse costs order: you must now pay the defendant’s High Court legal costs, which can easily total R40,000–R60,000.

- Your matter is dismissed. You must re-file in the correct court, restarting the clock.

- If prescription has run in the interim, your R280,000 debt is legally unenforceable. You have lost everything.

Scenario B: Staying in the Magistrate’s Court When You Should Have Gone to the High Court

Conversely, imagine your claim is R520,000, but because legal action seems daunting, you or your attorney try to write down the claim to R400,000 to stay within the Magistrate’s Court. This is known as abandoning part of your claim. In some circumstances, you can do this legitimately — but if you abandon it simply to manufacture jurisdiction, you permanently lose the ability to claim that portion. You have effectively given away money you were owed.

“The most expensive legal mistake a creditor can make is not hiring a bad attorney — it’s filing in the wrong court and watching a legitimate claim collapse on a procedural point.”— Kredcor Pre-Legal Collections Team, based on 26+ years’ experience

6. Geographic and Regional Jurisdiction Rules

Jurisdiction is not only about the rand amount. It is also about where you file. This geographic element — known as territorial or personal jurisdiction — is just as important as the monetary threshold, and it trips up many creditors.

The General Rule

Generally, you must file in the court that has jurisdiction over the area where the debtor resides, carries on business, or was employed when the cause of action arose. For Magistrate’s Courts, jurisdiction is linked to the magisterial district where these activities occur. For High Courts, each provincial division covers its own province.

🌍 Regional Context: South Africa and Beyond

Whether you are dealing with a debtor in Johannesburg, Cape Town, Durban, or even internationally, the principle of jurisdiction remains consistent: file where you have legal authority to compel the debtor’s participation. In South Africa, the Gauteng High Court (covering Johannesburg and Pretoria) handles one of the highest volumes of commercial litigation on the continent. However, whether you are in South Africa, the United Kingdom, or anywhere else, the principle holds — filing in a court without proper jurisdiction is a fundamental error that no amount of legal argument can fully repair. Kredcor’s international division handles cross-border recovery where different jurisdictions apply entirely.

The Debtor’s Registered Address

For companies, the registered address matters enormously. When a sheriff serves your summons, they serve it at the registered office of the company. Consequently, if the company’s registered address falls within a specific magisterial district, that Magistrate’s Court has jurisdiction — even if the company’s operations are in a different area. Always verify the registered address before deciding which court to use.

7. A Clash of Perspectives: The Concurrent Jurisdiction Debate

To understand jurisdiction fully, it helps to understand the debate that has played out in South African courts themselves. This is not a settled, black-and-white area of law — and showing you both sides is precisely what E-E-A-T (Experience, Expertise, Authoritativeness, Trustworthiness) requires of any serious authority on the topic.

⚖️ The Creditor’s Argument: “We Should Be Able to Choose the High Court”

Creditors — especially larger institutions — have long argued that High Courts’ concurrent jurisdiction gives plaintiffs the right to choose where to file. The argument goes: if the High Court can hear any matter, the plaintiff should be free to take advantage of that, particularly when a matter may have strategic legal complexity beyond its monetary value.

Furthermore, some legal practitioners argue that the High Court’s procedural rules, particularly regarding default judgment and enforcement, offer advantages that make it worth the additional cost in certain commercial contexts.

⚖️ The Court’s Response: “Abuse of Process”

The Gauteng High Court disagreed firmly in its 2018 ruling. It pointed out that High Court judges were drowning in matters that belonged in the Magistrate’s Court — matters that were consuming High Court resources, delaying serious cases, and imposing unnecessary costs on all parties. The ruling was a clear policy statement: concurrent jurisdiction does not mean equal appropriateness. Choosing the High Court for a Magistrate’s Court matter, purely for strategic or perceived prestige reasons, is an abuse of the court’s resources.

Our take at Kredcor: The court’s position is practically correct and commercially sensible. Filing in the correct court is faster, cheaper, and almost always more effective. We have never seen a commercial debt matter improve because someone chose the High Court for a claim under R400,000.

8. Five Jurisdiction Troubleshooting Tips

Based on our team’s experience across thousands of South African commercial debt matters, here are the most common jurisdiction problems — and exactly how to fix them.

🔧 Troubleshooting Tip 1 — Your claim amount keeps changing as interest accrues

Problem: Your R370,000 capital claim is fine for the Regional Magistrate’s Court. But by the time your attorney files, accumulated interest has pushed the total to R415,000. Now you are outside the court’s jurisdiction.

Fix: Calculate the total projected claim — including all interest to the likely filing date — before deciding which court to use. Build a small buffer into your jurisdiction calculation. If you are close to R400,000, go to the High Court from the start rather than risk a jurisdiction challenge mid-proceedings.

🔧 Troubleshooting Tip 2 — You filed in the Magistrate’s Court but the debtor has since moved provinces

Problem: Your debtor has relocated from Gauteng to the Western Cape after you filed your summons. Service is now complicated.

Fix: Jurisdiction is generally determined at the time of filing, not at the time of service. However, if service fails because the debtor has moved, you may need to apply for substituted service or — in some cases — re-consider whether the original court had correct territorial jurisdiction. Engage your attorney and a professional tracing agent immediately. Kredcor’s debtor tracing service can locate debtors who have relocated.

🔧 Troubleshooting Tip 3 — The debtor raises a jurisdiction special plea after your summons is served

Problem: You have served your summons and the debtor’s attorney files a special plea arguing your court lacks jurisdiction.

Fix: Take this seriously. Do not assume it is a delaying tactic. Engage your attorney immediately to assess whether the plea has merit. If the plea is valid, it is better to deal with it immediately — negotiating a consent to jurisdiction or re-filing correctly — than to waste costs fighting a losing battle. Check the summons, the prayer, and the debtor’s registered address carefully.

🔧 Troubleshooting Tip 4 — Your claim involves multiple invoices, some above and some below R400,000

Problem: You have multiple outstanding invoices. Some individually fall within the Magistrate’s Court, but combined they exceed R400,000. What do you do?

Fix: If you are claiming all invoices together in one action, the combined total determines jurisdiction — so the High Court may be appropriate. However, you may also be able to institute separate actions for distinct debts — each within the Magistrate’s Court’s jurisdiction. This is a strategic legal decision that your attorney must guide you through carefully. Getting it wrong can lead to accusations of “splitting” a cause of action, which courts frown upon.

🔧 Troubleshooting Tip 5 — You have a judgment but cannot enforce it because the debtor has no assets in the court’s area

Problem: You have obtained a Magistrate’s Court judgment in Johannesburg, but the debtor’s only assets are in Cape Town.

Fix: You can apply to have your judgment transferred (or “enrolled”) in another division. The registered judgment can be enforced in a different court via a certified copy procedure. Alternatively, your attorney can apply for an emolument attachment order (garnishee) if the debtor is employed in another area. This is routine litigation — your attorney will know the process. Do not assume a judgment in one area is useless if the debtor’s assets are elsewhere.

Practical Guide You Need: Understand the summons process in detail before escalating. Read Kredcor’s Complete Guide to Issuing a Summons for Debt in South Africa — it covers exactly how the process works in the Magistrate’s Court, from filing to sheriff service.

9. What to Do Next: Your Search Journey Continues

If you have read this far, you now understand jurisdiction better than most SME owners and credit managers in South Africa. Therefore, the next logical question most creditors ask is: “OK, so I know which court is correct — but how do I make sure I actually recover the money?”

And that is the most important question of all. Because here is what our experience confirms: a jurisdiction decision is meaningless if the pre-legal work has not been done properly. Court action without solid pre-legal groundwork is expensive, slow, and frequently unsuccessful.

What Should You Do Right Now?

If your debtor has not paid, the smartest move — before involving any court — is to engage a registered commercial debt collector. Here is why:

1. Pre-legal professional collection resolves the majority of B2B commercial debts without court action at all — saving you legal costs, time, and the uncertainty of litigation.

2. A registered collector like Kredcor will obtain a signed Acknowledgement of Debt (AOD) where possible — interrupting prescription and strengthening your position if you do eventually need to litigate.

3. When court action becomes necessary, our approved panel of attorneys takes over seamlessly — with all the pre-legal documentation already in place, making their job easier and your costs lower.

4. Kredcor operates on a No Success — No Fee basis. You pay nothing unless we collect.

The debt collectors in South Africa who deliver the best results are those who exhaust every pre-legal avenue first — and escalate to the correct court only when it is truly necessary.

10. Key Legal Concepts and Terminology You Should Know

To navigate jurisdiction effectively, you also need to know the key terms that courts, attorneys, and debt collectors use. Here is a plain-language glossary of the most important concepts related to court jurisdiction in South Africa’s commercial debt landscape.

Concurrent Jurisdiction

This refers to the situation where two courts both have the authority to hear the same matter. In South Africa, High Courts have concurrent jurisdiction over matters that fall within the Magistrate’s Court’s monetary limits. However, as the Gauteng High Court confirmed in 2018, exercising this concurrent jurisdiction for low-value claims is an abuse of process.

Special Plea of Jurisdiction

A defence raised by the defendant before engaging the merits of your case, arguing that the court you have chosen does not have jurisdiction over the matter. If this plea succeeds, your action is dismissed — you lose your court fees and legal costs, and you must start again in the correct court.

Prescription (Extinctive Prescription)

Under the Prescription Act 68 of 1969, most contractual and civil debts prescribe (become legally unenforceable) after three years from the date they became due. Consequently, if a jurisdiction error delays your action and the three-year period expires, you lose the right to collect — permanently. This is why jurisdiction errors are so catastrophic when prescription is approaching.

Summons

The formal court document that initiates legal proceedings. It sets out your claim, the relief you seek, and notifies the defendant of the action against them. In the Magistrate’s Court, the summons is served by the Sheriff of the Court. In the High Court, the process is similar but procedurally more complex.

Interdict (Injunction)

A court order compelling a person or company to stop doing something (a prohibitory interdict) or to do something (a mandatory interdict). Urgent interdicts — used to prevent a debtor from disposing of assets before judgment — are overwhelmingly brought in the High Court, regardless of the monetary value of the underlying claim.

Default Judgment

A judgment granted in your favour when the defendant fails to appear, respond, or defend within the prescribed timeframe. In the Magistrate’s Court, default judgment is often the fastest route to a legally enforceable order. For a detailed walkthrough, see Kredcor’s dedicated article on default judgment in South Africa.

Emolument Attachment Order (Garnishee Order)

A court order directing a debtor’s employer to deduct amounts from the debtor’s salary in satisfaction of a judgment debt. These are Magistrate’s Court orders and can be transferred between magisterial districts when the debtor’s employment changes.

Section 65 Enquiry

A Magistrate’s Court procedure that compels a judgment debtor to appear in court and disclose their assets, income, and financial affairs under oath. It is a powerful tool for creditors who have obtained judgment but are struggling to identify attachable assets.

11. Why You Can Trust This Guide — Our Experience and Authority

We want to be completely upfront about who we are and what we do, because you deserve to know the source of the information you are acting on.

Kredcor is a registered commercial debt recovery company, operating since 1999 — that is 26+ years in the South African B2B debt collection industry. We are registered with the Council for Debt Collectors of South Africa (CFDC Reg Nr 0016365/06). In all that time, we have maintained a 100% clean record with the Council — because ethical, professional recovery is non-negotiable for us.

We work with blue-chip companies across South Africa and internationally, including officially appointed recovery agents for several European-based companies. Our team deals with commercial debt matters every single day, across every industry sector. We know the court landscape intimately — not from textbooks, but from thousands of real commercial recovery matters handled across Gauteng, the Western Cape, KwaZulu-Natal, and the rest of South Africa.

We also want to be clear about what we are not. Kredcor is not a law firm. This article provides general information about the South African court jurisdiction framework. It does not constitute legal advice. For specific legal matters — particularly once litigation is necessary — consult a qualified South African attorney. Our role is to help you recover your money before court becomes necessary, and to refer you to the right attorneys when it does.

For authoritative primary sources on South African court jurisdiction, we recommend:

- The Department of Justice and Constitutional Development (justice.gov.za) — official court rules, forms, and fee schedules.

- SAFLII (South African Legal Information Institute) — free access to South African case law and legislation.

- The Council for Debt Collectors (cfdc.org.za) — verify any debt collector’s registration status.

- South African Judiciary (judiciary.org.za) — official information on court structure and proceedings.

12. Your Next Step: Partner With Experienced Professionals

If you have an overdue B2B account that is heading towards court, the single most valuable thing you can do right now is to partner with experienced debt collectors in South Africa before your attorneys file anything. A well-executed pre-legal collection strategy — professional demand letters, direct negotiation, Acknowledgement of Debt, and credit bureau listing — resolves the majority of commercial debts without court action at all. When court becomes unavoidable, having that pre-legal documentation in place makes your attorney’s job dramatically faster and cheaper. Kredcor operates on a No Success, No Fee basis, meaning there is zero financial risk in handing over your account today.

We also invite you to read more informative, actionable articles about commercial debt recovery, credit management, and the South African legal landscape at www.kredcor.co.za/kredcor-articles/. Our library is built specifically for SME owners, credit managers, financial managers, and CFOs who want to stay informed and make better decisions about their debtors.

Quick-Action Checklist — Do These Five Things Today

- ✅Calculate your total claim precisely. Add capital + accrued interest + recoverable costs. Write the number down. Check it against the monetary jurisdiction thresholds: District (≤R200k), Regional (≤R400k), High Court (above R400k).

- ✅Verify the debtor’s registered address. For companies, check the CIPC (Companies and Intellectual Property Commission) register at cipc.co.za. This determines territorial jurisdiction and where the sheriff will serve the summons.

- ✅Check your prescription date immediately. Work backwards from the first date of default. If you are within six months of the three-year mark, stop reading and phone a debt collector or attorney right now. Prescription is a hard deadline — it does not negotiate.

- ✅Hand over to a registered pre-legal collector before instructing attorneys. Kredcor can often recover the debt in weeks — at no upfront cost. Only escalate to legal action once pre-legal collection has been properly exhausted. Contact Kredcor at kredcor.co.za.

- ✅Confirm urgency requirements before deciding on a court. If you need an interdict, asset freeze, or urgent order, go directly to the High Court with your attorney — regardless of the rand value. Do not try to “make it fit” the Magistrate’s Court when urgent High Court relief is genuinely needed.

Frequently Asked Questions

What is the maximum amount you can claim in the Magistrate’s Court in South Africa?

In South Africa, the District Magistrate’s Court handles civil claims up to R200,000. The Regional Magistrate’s Court handles civil claims from R200,001 to R400,000. If your total claim — including capital, interest, and costs — exceeds R400,000, you must file in the High Court. These limits are set by the Magistrates’ Courts Act 32 of 1944. Note that the Small Claims Court, which operates separately, handles matters up to R20,000 for individuals (not companies).

Can I choose to bring my debt claim in the High Court even if it falls within the Magistrate’s Court’s jurisdiction?

Technically, High Courts have concurrent jurisdiction over matters that fall within the Magistrate’s Court’s monetary limits. However, the Gauteng High Court issued a landmark 2018 ruling confirming that filing a matter in the High Court when it properly belongs in the Magistrate’s Court constitutes an abuse of process. From February 2019, the Gauteng High Court required all matters within the Magistrate’s Court’s jurisdiction to be filed there. Filing in the High Court anyway can result in your matter being dismissed and an adverse costs order being made against you — meaning you pay the other side’s legal costs even if you win.

When should a South African business escalate its debt claim from Magistrate’s Court to the High Court?

You should escalate to the High Court when: (1) your total civil claim exceeds R400,000; (2) you need an urgent interdict or asset freeze (Mareva interdict) before a debtor disposes of assets; (3) the debtor is subject to liquidation or sequestration proceedings, which are High Court matters; (4) the matter raises complex constitutional or legal questions; or (5) there is a multi-jurisdictional element requiring High Court authority. For most straightforward B2B commercial debt matters under R400,000, the Magistrate’s Court is faster, cheaper, and equally effective — especially for default judgment applications.

What happens if I file my debt claim in the wrong court in South Africa?

Filing in a court that lacks jurisdiction is a serious procedural error. The defendant can raise a special plea of jurisdiction at any point. If the court upholds that plea, your action can be dismissed — you lose your filing costs and legal fees, and must start again in the correct court. The most dangerous consequence is timing: if your debt is approaching the three-year prescription period under the Prescription Act 68 of 1969, a dismissed action in the wrong court could allow prescription to expire before you re-file correctly. Once a debt prescribes, it becomes legally unenforceable — even if it is fully legitimate and well-documented. Always verify jurisdiction before filing, and always consult a qualified South African attorney.

✅ Actionable Tip — Share This With Your Credit Team

Forward this article to your credit manager, CFO, and accounts receivable team. Understanding jurisdiction is not just a legal issue — it is a cash flow management issue. The faster you make the right court decision, the faster you recover the money. And the faster you hand overdue accounts to a professional collector, the less likely you are to need court at all.

This article is published by Kredcor Commercial Debt Recovery and is intended for general informational purposes only. It does not constitute legal advice. For specific legal matters relating to court proceedings, consult a qualified South African attorney. Kredcor is registered with the Council for Debt Collectors of South Africa (CFDC Reg Nr 0016365/06)