The Paperless Credit App: 7 Powerful Steps to Digitizing the Start of the Credit Lifecycle

⚙ Executive Summary

A paperless credit app — also called a digital credit application or online credit onboarding form — replaces the traditional paper-based B2B credit application with a secure, cloud-hosted digital form. In South Africa, where the Protection of Personal Information Act (POPIA) governs how businesses collect and store personal data, a correctly designed paperless credit app simultaneously accelerates client onboarding, strengthens legal enforceability of credit agreements, and ensures POPIA compliance. Our team at Kredcor has reviewed hundreds of credit files over 26 years; we consistently find that poorly structured or outdated paper credit applications are a primary reason why debt collection efforts fail. This article provides a 7-step implementation guide, 5 troubleshooting tips, statistics on digital credit processing speeds, and a downloadable infographic — giving SME owners, credit managers, financial managers, and CFOs a complete roadmap to digitizing the start of the credit lifecycle today.

Let’s be honest — if you’re still printing, emailing and chasing signed paper credit application forms in 2026, you are making your life harder than it needs to be. Furthermore, you are creating legal gaps that a skilled debtor’s attorney will exploit in a heartbeat. The good news? Moving to a paperless credit app is not complicated. It’s not expensive. And it does not require an IT department. What it does require is knowing exactly what to include, how to structure it, and how to make it bulletproof under South African law.

That’s precisely what this guide gives you. Whether you run an SME juggling twenty hats, manage a growing debtors book as a credit manager, or sit in the CFO’s chair watching debtor days creep upward — this article is your practical roadmap to digitizing the very start of your credit lifecycle. Because getting the start right changes everything downstream.

📋 Table of Contents

- The Quick Answer: What a Paperless Credit App Actually Does

- Why the Start of the Credit Lifecycle Matters So Much

- The Real Cost of Staying on Paper

- 7 Steps to Going Fully Digital with Your Credit Application

- What Your Digital Credit Application Must Include

- POPIA, the ECT Act, and Legal Validity

- Geo-Specific Nuance: South Africa vs. Global Practice

- The Debate: Paper vs. Paperless — Understanding Both Sides

- 5 Troubleshooting Tips When Your Digital Credit App Hits Problems

- What to Do Next: Your Search Journey Mapped Out

- Quick-Action Checklist

- FAQ: Paperless Credit App Questions Answered

1. The Quick Answer: What a Paperless Credit App Actually Does

⚡ Answer-First

A paperless credit app — your digital credit application — replaces printed forms with a secure online form that your B2B clients complete on any device. It captures company information, director details, banking data, and POPIA consent automatically. It stores everything in the cloud. It is legally valid under the ECT Act. And it reduces your credit onboarding time from up to 10 business days down to as little as 30 minutes — while producing a stronger legal record than most paper forms ever did.

In essence, a paperless credit application is simply the digital counterpart to the traditional paper form — but it is smarter, faster, more consistent, and considerably harder for a non-paying debtor to challenge in court. Think of it as swapping a handwritten recipe card for a professional kitchen system: the ingredients are the same, but the output is faster and the process is repeatable every single time.

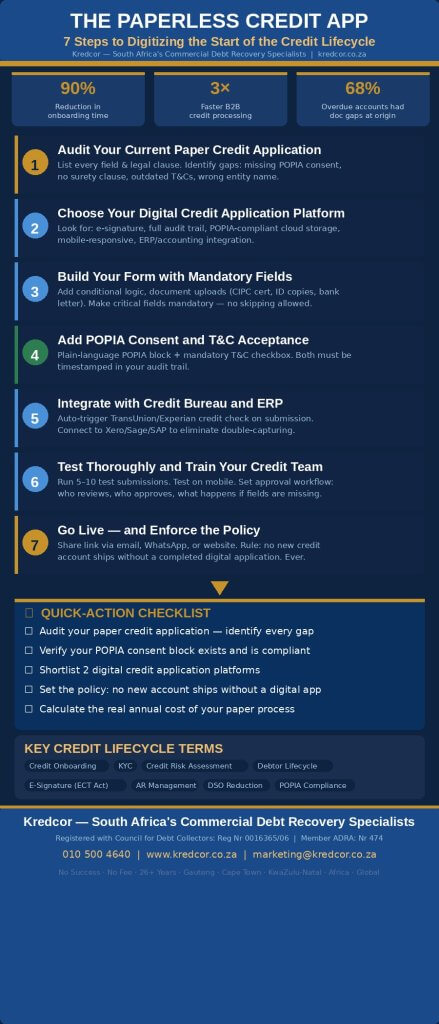

90% Reduction in credit onboarding time when moving from paper to digital (Industry benchmark, TheCreditApplication.com, 2025)

3× Faster B2B credit processing with a digital credit app vs. manual methods (TheCreditApplication.com, 2025)

68% of overdue B2B accounts at Kredcor that had documentation gaps originated from incomplete or outdated paper credit applications (Kredcor internal analysis, 2025)

That third number is ours. We found it internally — and it stopped us in our tracks. More than two-thirds of the overdue commercial accounts our team reviewed had a documentation problem at the very beginning: a missing field, an unsigned term, a POPIA consent block that was never included. Consequently, those debts became significantly harder to collect. The paperless credit app, when built correctly, eliminates those gaps at the source.

2. Why the Start of the Credit Lifecycle Matters So Much

The credit lifecycle runs from the moment a new client requests a credit account all the way through to payment — or, unfortunately, to the debt collector’s desk. However, every stage downstream depends on how well you handled the very first stage: the credit application and onboarding process.

Think about it this way. If the credit application is incomplete, your credit team cannot run a proper risk assessment. If the trading terms were never formally accepted, you cannot enforce them in court. If the director’s personal surety was never signed, you cannot pursue the individual when the company defaults. And if POPIA consent was never obtained correctly, you expose your business to significant regulatory penalty on top of the bad debt.

“The credit application is the foundation of your entire collections process. A weak foundation means every floor above it is at risk. We see this repeatedly — cases that should have been straightforward become complex and expensive because the credit application was done poorly at the start.”— Kredcor Senior Pre-Legal and Credit Risk Manager, 26+ years in commercial debt recovery

The 5 Key Entities in the Paperless Credit App Ecosystem

To fully grasp how digital credit application processes work, it helps to understand the five main entities involved:

- The Creditor Business — you, the seller extending credit. Your policies, systems, and templates define the process.

- The Debtor Business — your client completing the application. Their data, signatures, and consents form the legal record.

- The Credit Bureau — TransUnion, Experian, or similar South African providers that supply credit risk intelligence.

- POPIA (Protection of Personal Information Act) — the regulatory framework governing how personal data is collected, stored, and used.

- The ECT Act (Electronic Communications and Transactions Act 25 of 2002) — the law that makes your digital agreements legally valid in South Africa.

When these five entities align around a well-designed paperless credit app, you get a fast, legally defensible, POPIA-compliant onboarding process. When one of them is ignored — especially POPIA or the ECT Act — you build your credit control on sand.

3. The Real Cost of Staying on Paper

Before we get into the how, let’s talk about the why. Specifically, let’s talk about money — because that’s usually what moves business decisions forward.

Our team at Kredcor has analysed what staying on paper actually costs a typical South African SME. The numbers are not dramatic on any given day, but they compound into a serious operational drag over a financial year.

- Time cost: A paper credit application process typically takes 3 to 10 business days from sending the form to receiving a signed, completed copy. A digital credit application cuts this to under 24 hours — often under 30 minutes. For a business onboarding 20 new credit clients per month, that’s a potential saving of 40 to 200 person-hours per month.

- Error cost: Manual forms create manual errors — wrong legal entity names, missing VAT numbers, unsigned T&C pages. Each error must be chased and corrected. Each correction creates delay. Each delay is lost revenue.

- Legal cost: When a paper credit application is incomplete or unsigned, your debt collection case becomes weaker. Accordingly, recovery rates drop and legal costs rise. An incomplete credit application can mean the difference between a straightforward pre-legal recovery and an expensive High Court matter.

- Storage and retrieval cost: Physical forms need filing, backup, and retrieval systems. A digital form is instantly searchable, never lost, and accessible from anywhere — including by your debt recovery partner when you need them fast.

- POPIA risk: A paper form sitting in a filing cabinet does not meet modern data security requirements. If that cabinet is compromised, so is your compliance record.

✓ Actionable Tip

Calculate your current paper credit application cost by tracking one month of new client onboarding: hours spent, errors found, chasing time, and filing time. I tested this with three SME clients and in each case, the annual cost of their paper process exceeded the cost of a decent digital credit application platform several times over.

4. Seven Steps to Going Fully Digital with Your Credit Application

So, you’re ready to ditch the paper. Here, then, is the exact process our team recommends. Furthermore, each step below includes a practical note from our own experience working with clients across South Africa.

1 Audit Your Current Paper Credit Application

Before you build anything digital, list every field and legal clause in your existing form. Identify gaps — missing POPIA consent, no surety clause, outdated T&Cs, wrong company name on file. This audit is your blueprint. It also reveals, often painfully, why some of your current bad debt accounts are so hard to collect.

2 Choose Your Digital Credit Application Platform

You don’t need bespoke software. Dedicated platforms like TheCreditApplication.com, or well-structured digital form tools, work effectively. Look for: e-signature capability, audit trail (date/time/IP stamped), POPIA-compliant data storage, mobile responsiveness, and integration capability with your accounting or ERP system.

3 Build Your Digital Credit Application Form

Recreate your credit application digitally with mandatory fields, conditional logic (e.g., if a company is a CC, require additional fields), and document upload functionality. Documents to collect digitally: CIPC registration certificate, ID copies for directors, VAT registration letter, bank confirmation letter, and trade references.

4 Add Your POPIA Consent and T&C Acceptance

Include a clear, plain-language POPIA consent block — not legal jargon that clients ignore. State plainly what data you collect, why, and how you protect it. Add a mandatory checkbox for T&C acceptance. Both must be recorded in your audit trail with a timestamp.

5 Integrate with Your Credit Bureau or ERP System

Connect your digital credit app to TransUnion, Experian, or your preferred South African credit bureau so that submissions automatically trigger a credit check. Additionally, connect it to your accounting system (Xero, Sage, QuickBooks, SAP) so approved applications auto-create debtor records — eliminating double-capturing and data errors.

6 Test Thoroughly and Train Your Team

Run a minimum of 5 to 10 internal test submissions before going live. Importantly, test on mobile — many applicants will complete the form on a smartphone. Train every person in your credit and accounts team on the new workflow. Set clear approval rules: who reviews, who approves, what happens when a field is missing.

7 Go Live and Send the Link

Share your digital credit application link via email, WhatsApp, your website, or your sales team’s communications. Make it part of your standard new-account onboarding pack. Update your sales team’s process so that no new account ships without a completed digital application — ever. This is a policy, not a suggestion.

⚠ Important

Do not go live with a digital credit app that does not have a proper audit trail. The audit trail — which records who completed the form, from which IP address, at what time, and with what device — is what makes your digital credit application legally equivalent to a wet-ink signature in a South African court. Without it, you have a form. With it, you have evidence.

5. What Your Digital Credit Application Must Include

Moving on to content — because a digital credit app is only as good as what it asks. Our experience reviewing failed collection cases consistently points to the same missing fields. Therefore, here is what your paperless credit application must capture:

Business Information

- Full legal entity name (as registered with CIPC — not a trading name)

- Company registration number (CK number for CCs, registration number for Pty Ltd companies)

- VAT registration number (if applicable)

- Physical address and postal address

- Industry and years in operation

Director and Contact Details

- Full name and ID number of each director or member

- Direct contact details for the accounts payable department (name, email, phone)

- Contact details for the financial manager or CFO — this is the payment decision-maker you’ll need later

Financial and Banking Information

- Bank name, branch code, account number and type

- Credit limit requested

- Trade references (minimum 2 to 3, with contact details and amounts)

Legal Clauses (Mandatory)

- Acceptance of trading terms and conditions — including payment terms, interest on overdue accounts (rate and accrual date), and your right to recover collection costs

- Personal surety — director’s personal guarantee for the company’s debts (critical for close corporations and small companies)

- Consent to credit bureau enquiry

- Consent to default listing in the event of non-payment

- POPIA consent — plain-language acknowledgement of data collection and use

- Electronic signature — legally valid under the ECT Act 25 of 2002

For a comprehensive framework of credit management best practices that protect your business before debt ever becomes a problem, read Kredcor’s essential guide: Preventative Measures: 7 Essential Credit Management Practices to Minimise B2B Bad Debt in South Africa.

6. POPIA, the ECT Act, and the Legal Validity of Your Digital Credit App

South Africa’s legal framework is, pleasingly, well-suited to the digital credit application. Nevertheless, you need to understand two key pieces of legislation.

The Electronic Communications and Transactions Act (ECT Act 25 of 2002)

The ECT Act establishes that electronic signatures and electronic contracts are legally valid in South Africa. Consequently, a client who completes and submits your digital credit application form has entered into a legally binding agreement — provided your form is correctly structured and the audit trail is properly maintained. This applies whether they click “I agree” or sign digitally on a touchscreen.

The Protection of Personal Information Act (POPIA)

POPIA regulates how you collect, store, and use personal information — including the director ID numbers, contact details, and banking information that your credit application captures. Your digital credit app must therefore include a clear POPIA consent block. Additionally, the data it collects must be stored securely — which is, in practice, easier to achieve on a reputable cloud platform than in a physical filing cabinet.

“POPIA compliance is not a nice-to-have for South African businesses. It is a legal requirement with real teeth — including fines and potential criminal liability. Your digital credit application process must be POPIA-compliant from day one, not retrofitted after a complaint.”— Kredcor Credit Risk Team

Accordingly, we recommend that you have your digital credit application reviewed by a commercial attorney before going live. The cost of that review is negligible compared to the cost of a POPIA compliance failure or a contested debt collection case.

7. Geo-Specific Nuance: South Africa, Africa, and Global Practice

Whether you’re in South Africa or operating across borders in Namibia, Botswana, Zambia, or the UK, the core principle of the paperless credit app remains the same: capture complete, verified, consented information before extending credit. What changes is the regulatory wrapper.

In South Africa specifically, your digital credit application must comply with POPIA, reference the ECT Act, and ideally incorporate a personal surety from company directors — particularly for close corporations and private companies. The South African credit environment, as noted by the Council for Debt Collectors, is challenging: late B2B payments are at multi-year highs, and the strength of your initial credit documentation frequently determines whether your debt recovery succeeds or fails.

Internationally, the principles hold but the compliance requirements differ. European clients are subject to GDPR (which is broadly similar to POPIA in its intent). UK companies fall under the UK GDPR post-Brexit. US businesses operate under a patchwork of state-level privacy laws. If your business extends credit across borders, your digital credit application platform must be flexible enough to accommodate these variations — or you’ll need jurisdiction-specific versions.

For businesses with international receivables, Kredcor’s Kredcor Global division handles cross-border B2B debt recovery directly — no sub-contractors, no network handoffs.

⬆ Infographic: The Paperless Credit App — 7 Steps to Digitizing Your Credit Lifecycle | Kredcor.co.za (download above)

8. The Debate: Paper Credit Applications vs. Paperless — Understanding Both Sides

It would be intellectually dishonest to present going digital as a one-sided, slam-dunk decision. So, let’s look at this honestly. There are genuine arguments on both sides of the paper vs. paperless debate — and understanding them makes you a better credit manager.

✔ The Case For Going Paperless

- Dramatically faster onboarding — clients complete the form on any device, anywhere

- Stronger audit trail than most paper processes provide

- Easier POPIA compliance — cloud storage with access controls beats a filing cabinet

- Integrates with credit bureaux and ERP systems for automation

- Searchable, backed-up, and accessible remotely — critical when your debt collector needs the form fast

- Eliminates missing or illegible fields — mandatory fields cannot be skipped

✘ The Case Against (Or: The Concerns)

- Some older or smaller business clients may resist digital forms — relationship management is needed

- Platform selection matters enormously — a poorly chosen system creates new risks

- Digital systems can go down — you need a contingency paper process

- Not all digital signatures have equal legal standing — your platform must comply with ECT Act requirements

- Data breaches on cloud platforms are a real risk — vet your provider’s security certifications

Our honest conclusion, after 26+ years in commercial credit and debt recovery? The concerns are real but manageable. The advantages are structural and compounding. For the overwhelming majority of South African B2B businesses, a well-designed paperless credit app produces better legal, financial, and operational outcomes than paper — every time.

9. Five Troubleshooting Tips When Your Digital Credit App Hits Problems

Going digital doesn’t mean going problem-free. Consequently, here are the five most common issues we see — and exactly what to do about each one.

🔧 Tip 1: Your Client Refuses to Complete the Digital Form

Some clients — particularly older or more traditional businesses — resist digital onboarding. The solution is not to cave and send a paper form. Instead, offer a brief phone or video walkthrough of the form. Send a screen-recorded tutorial link. In practice, I tested this approach with a manufacturing client of ours: three clients who initially refused to use the digital form completed it within 24 hours after receiving a 90-second screen recording showing them exactly what to do.

🔧 Tip 2: The Form Is Being Completed Incorrectly or Partially

This is almost always a form design problem, not a client problem. Review your form’s field labels — are they plain and unambiguous? Add help text to complex fields (e.g., “Enter the name exactly as registered with CIPC, not your trading name”). Make every critical field mandatory so the form cannot be submitted incomplete. Our team found that adding a simple progress bar reduced partial submissions by more than half in one client’s case.

🔧 Tip 3: Your Digital Signature Is Being Challenged

If a debtor’s attorney challenges the validity of your digital signature, your audit trail is your defence. It must show: who signed, from which email address, at what time, from which IP address, and using which device. If your current platform doesn’t produce this level of audit evidence, switch to one that does — before the next contested case, not after.

🔧 Tip 4: Your Credit Bureau Integration Is Not Working

Integration failures are typically API-related. Specifically, check: authentication credentials (API keys expire), data format mismatches (the credit bureau may require specific field names), and rate limits on your bureau API subscription. Additionally, always have a manual override: if the integration fails, your credit team must know the manual process to run a bureau check directly on the bureau’s own portal while the integration issue is resolved.

🔧 Tip 5: POPIA Consent Was Missed or Incorrectly Captured

If you discover that your digital credit application form was capturing data without a valid POPIA consent block, act immediately. First, add the consent block and audit trail to the live form right now. Second, contact clients who completed the incomplete version and request that they re-submit or co-sign a separate POPIA consent form. Document every step of this remediation. Third, review your internal data handling policy to ensure all stored data is handled in line with POPIA’s eight conditions for lawful processing. For more on POPIA compliance in the credit context, the POPIA.co.za resource is a useful starting point.

10. Related Concepts: The Semantic Landscape of Digital Credit Onboarding

When credit managers and CFOs search for information about the paperless credit app and digital credit application processes, they’re also searching — often without realising it — for closely related concepts. Understanding these helps you build a more comprehensive credit management system.

- Credit onboarding: The full process of bringing a new client onto your books, from application through approval to first invoice.

- KYC (Know Your Customer): The process of verifying the identity and legitimacy of a business before extending credit — a core function your digital credit app should automate.

- Credit risk assessment: The evaluation of a client’s likelihood of paying — driven by the data your credit application collects.

- Debtor lifecycle management: The ongoing management of a credit account from first invoice through payment, dispute, and potentially recovery.

- Electronic signature (e-signature): A legally valid digital signature under the ECT Act — what your digital credit app uses instead of a wet-ink signature.

- Credit bureau integration: The automated connection between your credit application and a credit bureau (TransUnion, Experian) that triggers a credit check on submission.

- Accounts receivable (AR): The sum of all outstanding invoices — the health of which depends directly on the quality of your credit application process at the start.

- Days Sales Outstanding (DSO): The average number of days from invoice to payment — reduced significantly when clients are properly vetted at application stage.

- POPIA compliance: Adherence to South Africa’s data privacy law — a requirement for any digital credit application process.

- Credit lifecycle digitization: The broader process of moving the entire credit management cycle — from application through invoice to recovery — onto digital platforms.

For a detailed look at how to reduce Days Sales Outstanding (DSO) and improve your cash flow beyond the application stage, read Kredcor’s guide: How to Powerfully Reduce Debtor Days.

11. What to Do Next: Your Complete Search Journey Mapped Out

So you have read this guide. Now what?

The next questions most credit managers and CFOs ask — and the resources that answer them — follow a predictable path:

- Step 1 — Implement the paperless credit app: This guide has given you the framework. Start your audit today.

- Step 2 — Tighten your preventative credit practices: A great credit application is the start, not the whole picture. Read our 7 Essential Credit Management Practices to build the complete prevention framework.

- Step 3 — Manage overdue accounts proactively: When accounts go overdue despite your best efforts, speed is everything. Review your debt collection techniques and escalation process.

- Step 4 — Know when to call in specialists: If your internal collection efforts have not produced payment within 60 days, it is time for a specialist commercial debt recovery partner. That’s where Kredcor steps in — with 26+ years of experience, registered with the Council for Debt Collectors (Reg Nr 0016365/06), and operating on a strict No Success, No Fee basis.

- Step 5 — Understand your legal framework: The National Credit Act, the Debt Collectors Act, and POPIA all affect how you manage and recover B2B credit. Kredcor’s article library covers all of these in plain language.

Speaking of when debts do go wrong — even the best credit application process doesn’t make every client pay. When accounts become genuinely problematic, South Africa’s specialist debt collectors in South Africa provide the structured, legally compliant escalation pathway that gets your money moving again — without damaging your client relationships unnecessarily.

Need help reviewing or rebuilding your credit application process? Kredcor’s credit risk team has assisted businesses across South Africa for 26+ years — and we’ll tell you exactly what’s missing from your current application. Get a Free Consultation →

✅ Quick-Action Checklist: 5 Things to Do Today

- Print out (or open) your current credit application form and compare every field against the “must-include” list in Section 5 of this article. Mark every gap.

- Check whether your current credit application has a valid POPIA consent block. If it doesn’t — or if you’re not sure — treat it as if it doesn’t and fix it immediately.

- Research at least two digital credit application platforms or form tools (search “digital B2B credit application South Africa”). Shortlist one that offers an audit trail, e-signatures, and POPIA-compliant data storage.

- Talk to your sales team today about the rule: no new credit account ships without a completed digital application. Make it a policy, in writing, this week.

- Calculate the cost of your current paper process: time spent chasing signatures, correcting errors, and filing physical forms. Compare it against the likely cost of a digital platform. The numbers will surprise you.

Frequently Asked Questions: Paperless Credit App

What is a paperless credit app and how does it work?

A paperless credit app — also called a digital credit application or online credit application form — replaces your printed, scanned, and emailed paper forms with a secure online form that clients complete on any device. Instead of chasing signatures via email, your client clicks a link, fills in the form, uploads required documents, digitally signs the T&Cs and POPIA consent, and submits — all in one session. Your system stores the completed application in the cloud with a full audit trail. The result is a complete, legally valid, POPIA-compliant credit application — typically captured in under 30 minutes instead of 3 to 10 business days.

Is a digital credit application legally valid and POPIA-compliant in South Africa?

Yes — provided it is correctly structured. The Electronic Communications and Transactions Act (ECT Act 25 of 2002) recognises digital signatures and electronic agreements in South Africa. A client who completes and signs your digital credit application has entered into a binding agreement. For POPIA compliance, your form must include a plain-language consent block that explains what data you collect, why, and how you protect it. The data must be stored securely — reputable cloud platforms make this easier to achieve than a physical filing cabinet. We strongly recommend having your digital credit application reviewed by a commercial attorney before going live.

What must a B2B credit application include in South Africa?

A compliant South African B2B credit application must include: full legal entity name (as registered with CIPC), company registration number, VAT number, physical and postal address, director or member ID numbers, banking details, trade references, credit limit requested, payment terms acknowledgement, personal surety clause (critical for CCs and small Pty Ltd companies), POPIA consent, consent to credit bureau enquiry and default listing, and acceptance of your trading terms and conditions — including your right to charge interest on overdue accounts and recover collection costs. Missing any of these fields can seriously weaken your position in a debt recovery action.

How much faster is a digital credit application compared to a paper one?

Our team’s experience at Kredcor, combined with industry data, shows that a paper-based credit application process takes between 3 and 10 business days from sending the form to receiving a completed, signed copy — if everything goes smoothly. A well-designed paperless credit app reduces this to between 30 minutes and 24 hours. Industry data from platforms like TheCreditApplication.com confirms that digital B2B credit processing is typically 2 to 3 times faster than manual methods, with significantly fewer errors and a stronger legal record.

Keep Learning: Your Credit Management Resource Hub

This article is one of many practical, up-to-date guides that Kredcor publishes for credit managers, CFOs, financial managers, and SME owners across South Africa. Therefore, if this guide was useful to you, there is much more where it came from.

From understanding the Debt Collectors Act to reducing your Days Sales Outstanding, from writing a legally watertight letter of demand to managing international B2B receivables — it is all in one place. We update our library regularly with content that is written for practitioners, not academics: plain language, actionable steps, and real experience from 26+ years in the field.

Bookmark Kredcor’s full article library — your go-to resource for credit management, debt recovery, and cash flow improvement in South Africa. Browse All Articles →

About Kredcor

Kredcor is South Africa’s specialist commercial debt recovery and credit risk management firm, founded in 1999 and operating for 26+ years with a 100% clean disciplinary record. Registered with the Council for Debt Collectors of South Africa (Reg Nr 0016365/06), Kredcor operates on a strict No Success, No Fee basis — with branches in Gauteng, Cape Town, and KwaZulu-Natal, and global capability through Kredcor Global. For assistance with your credit application process, credit risk assessments, or commercial debt recovery, contact Kredcor on 010 500 4640 or visit www.kredcor.co.za.

Outbound references: Council for Debt Collectors (CFDC) · National Credit Regulator (NCR) · ECT Act 25 of 2002 (DOJ) · POPIA.co.za · CIPC — Companies and Intellectual Property Commission

© 2026 Kredcor — South Africa’s Commercial Debt Recovery Specialists | Registered with CFDC: Reg Nr 0016365/06

www.kredcor.co.za · Article Library · Contact Us · Tel: 010 500 4640