Hidden Costs: The Shocking Real Price of “Doing Nothing” About Bad Debt

For SME owners, credit managers, financial managers, and CFOs who want to stop losing money silently — starting today.

By Kredcor Commercial Debt Recovery | Updated April 2026 | 26+ Years of B2B Collection Experience | CFDC Reg Nr 0016365/06

📋 Executive Summary

Bad debt — unpaid B2B invoices left unresolved — costs South African businesses far more than the face value of the outstanding invoice. The real, hidden costs include lost profit margin (businesses on a 10% net margin must generate R10 in new sales for every R1 written off), wasted staff time, compounding interest on borrowed working capital, legal and credit bureau fees, and the permanent opportunity cost of cash that never returned. Our internal data from over 26 years of commercial debt recovery shows that businesses without a structured recovery process write off an average of 3–5% of annual turnover. In South Africa, where commercial debts prescribe under the Prescription Act 68 of 1969, inaction is a time-limited mistake. The solution is early escalation: handing accounts over to a CFDC-registered recovery agency at 60–90 days overdue delivers dramatically higher recovery rates. This article walks SME owners, credit managers, financial managers, and CFOs through every hidden cost — and gives them the exact steps to stop the bleed today.

Let’s be honest for a moment. You have an overdue account sitting in your books. Maybe it’s been there for 60 days. Maybe 120. You’ve sent the statements. You’ve made the calls. You’ve even sent that painfully polite “just following up” email — three times. And still, nothing.

So you do what most business owners eventually do: you decide to wait a little longer. You tell yourself it will sort itself out. After all, there are bigger fires to fight today. Right?

Here’s the uncomfortable truth: that decision to do nothing is costing you far more than the invoice value. The hidden costs of bad debt are real, they are measurable, and they compound every single week you delay. Whether you are running a manufacturing business in Johannesburg, a professional services firm in Cape Town, or a logistics company in Durban — the principle is the same.

This article is going to show you exactly what “doing nothing” about bad debt is actually costing your business — in rands, in time, and in growth. More importantly, it gives you a clear, actionable road map to stop the damage today.

📖 Table of Contents

- The Answer First: What Does Bad Debt Really Cost You?

- The 5 Key Entities Behind the Bad Debt Problem

- Hidden Cost #1 — The Sales-to-Recover Multiplier

- Hidden Cost #2 — The Cash Flow Stranglehold

- Hidden Cost #3 — Staff Time and the Invisible Salary Bill

- Hidden Cost #4 — Prescription: The Ticking Clock

- Hidden Cost #5 — Reputational and Relational Damage

- Hidden Cost #6 — Opportunity Cost and Stalled Growth

- Hidden Cost #7 — Interest, Borrowing, and Financial Stress

- The South African Context: Why Bad Debt Hits Harder Here

- The Alternative View: “We Manage It Fine In-House”

- 5 Troubleshooting Tips: When Your Recovery Efforts Are Failing

- What to Do Next: Your Action Plan

- The Quick-Action Checklist

- Frequently Asked Questions (FAQ)

1. The Answer First: What Does Bad Debt Really Cost You?

The short answer: bad debt costs your business between 5 and 20 times the face value of the unpaid invoice, once every hidden factor is taken into account.

That is not a typo. And it is not an exaggeration. It is the result of a simple formula that any CFO or financial manager understands but very few SME owners have ever actually applied to their own debtors book.

Let’s look at the facts before we dig into the detail:

R10 New revenue needed to offset every R1 of bad debt written off (at 10% net margin)

3–5 % Average annual turnover lost to bad debt write-offs in businesses without a structured recovery process (Kredcor internal data, 26 years)

3 years Prescription period for most commercial debts in South Africa under the Prescription Act 68 of 1969

85% → 30% Recovery rate drop when accounts are placed with collectors after 120 days vs. 60 days (Kredcor field data)

Consequently, the cost of bad debt is not simply a financial number. It is a business risk, a growth blocker, and — if left long enough — a genuine threat to survival. Furthermore, in South Africa’s current economic environment, where B2B payment delays regularly stretch 30 to 90 days beyond agreed terms, this is not a theoretical problem. It is happening in your debtors book right now.

2. The 5 Key Entities Behind the Bad Debt Problem

To fully understand the hidden costs of bad debt, it helps to understand the five key entities that shape the commercial debt landscape in South Africa.

These are the players your debtors book interacts with every day — whether you realise it or not:

- Your Business (The Creditor): You extended credit in good faith. You delivered the goods or services. And now you are waiting. Every day of waiting is a cost to you.

- The Debtor: The business that owes you money. Their reasons for non-payment vary — cash flow problems, internal disputes, deliberate avoidance. Each requires a different approach.

- The Council for Debt Collectors (CFDC): South Africa’s statutory regulatory body under the Debt Collectors Act 114 of 1998. Only CFDC-registered agencies may legally collect third-party debt in South Africa. Kredcor holds CFDC Registration Nr 0016365/06.

- The South African Reserve Bank (SARB): Interest rates and monetary policy directly affect the cost of borrowing against your unpaid receivables. The SARB’s data consistently shows business liquidity as a top concern for South African corporates.

- Statistics South Africa (StatsSA): StatsSA consistently reports that cash flow problems — largely driven by overdue debtors — are among the leading causes of business failure in South Africa.

Understanding how these entities interact helps you see that bad debt management is not just a collections task. Rather, it is a cross-functional business priority that touches credit policy, cash flow management, legal compliance, and growth strategy all at once.

3. Hidden Cost #1 — The Sales-to-Recover Multiplier

This is the big one. It is also the one that, in our experience, genuinely shocks most business owners when they first calculate it.

When you write off a bad debt, you do not just lose that money. You lose the profit margin on every future sale you must make to break even. Here is the formula:

The Sales-to-Recover Formula:

Additional Sales Needed = Bad Debt Amount ÷ Net Profit Margin

Example: A R50,000 write-off on a 10% net margin requires R500,000 in new sales just to break even.

Think about what that means in practice. You write off a R50,000 invoice. Your sales team now has to find, close, and deliver R500,000 worth of new business — just to get back to zero. Not to grow. Not to invest. Just to replace what you lost.

Moreover, if your net margin is lower — say 5%, which is common in many South African industries — that same R50,000 write-off requires R1,000,000 in new sales to recover. That is not a bad debt problem. That is a business crisis.

| Bad Debt Amount | Net Margin 5% | Net Margin 10% | Net Margin 20% |

|---|---|---|---|

| R10,000 | R200,000 | R100,000 | R50,000 |

| R50,000 | R1,000,000 | R500,000 | R250,000 |

| R100,000 | R2,000,000 | R1,000,000 | R500,000 |

| R250,000 | R5,000,000 | R2,500,000 | R1,250,000 |

Table: New sales required to offset bad debt write-offs at different net margins. Source: Kredcor internal analysis.

So, the next time someone in your business suggests “let’s just write it off,” ask them: “Which R500,000 client are you going to find tomorrow to cover that?”

📎 Further Reading: For a comprehensive breakdown of when your debt has become unrecoverable and what to do about it, read our detailed guide: Debt Recovery Is a Critical Operation — 7 Proven Strategies for South African Businesses

4. Hidden Cost #2 — The Cash Flow Stranglehold

Bad debt does not just cost you on paper. It creates a very real, very immediate cash flow problem that can paralyse your day-to-day operations.

Think about it this way. You delivered the goods on Day 1. You incurred the cost of production, staff, materials, and overheads on Day 1. But the cash to cover those costs has not arrived — and may never arrive. So, in the meantime, you are funding the debtor’s business with your own working capital.

Furthermore, while that cash is stuck in your debtors book, you cannot use it to pay suppliers, to fund new stock, to meet payroll, or to take advantage of growth opportunities. Every rand sitting in an overdue account is a rand that is not working for your business.

“Every week that passes without professional intervention reduces your recovery probability. We have seen accounts that could have been recovered in full at 60 days, written off entirely at 18 months.”— Kredcor Senior Pre-Legal and Credit Risk Manager

Additionally, the knock-on effects compound quickly. Delayed supplier payments can damage your own credit rating and trade relationships. Late payroll can destroy staff morale and trigger resignations. And a shortage of working capital can prevent you from taking on new orders — which means bad debt does not just cost you what you lost. It costs you what you could have gained.

The Debtor Days Problem

Your Debtor Days (also called Days Sales Outstanding, or DSO) measures the average number of days it takes your customers to pay. The higher your debtor days, the more capital you have tied up in unpaid invoices — and the more stress your cash flow is under.

Our team’s experience across hundreds of South African businesses consistently shows that companies with a structured, proactive debt recovery process maintain significantly lower debtor days — and therefore healthier cash flow — than those who rely on passive follow-up.

⚠️ Cash Flow Warning Sign If your debtor days are consistently above 60, and you have accounts that are 90+ days overdue with no signed payment arrangement, your business is carrying unnecessary, avoidable financial risk. It is time to act.

5. Hidden Cost #3 — Staff Time and the Invisible Salary Bill

Here is a cost that almost nobody calculates — and yet it is often one of the most significant. Every time a member of your team chases an overdue account, you are paying for that time. And in most South African SMEs, that cost is substantial.

Consider a typical scenario: your accounts manager spends two hours per week chasing five overdue accounts. That is 100 hours a year on accounts that may never pay. At a fully loaded cost of R250 per hour, that is R25,000 in staff costs annually — on accounts that may also result in a write-off.

Moreover, that is the optimistic scenario. In reality, as overdue accounts escalate and become more difficult, the time investment grows. Phone calls get longer. Disputes get more complex. And before long, a senior manager or even the business owner is involved — at a far higher hourly cost.

Additionally, there is a significant opportunity cost to this staff time. Every hour your credit manager spends chasing a slow payer is an hour they are not spending on credit risk assessment, new client onboarding, or process improvement. In short, bad debt management consumes resources that should be building your business.

✅ Kredcor Tip When you hand accounts over to Kredcor at the 60–90 day mark, your internal team is free to focus on what they do best. We handle the collection. You get your time and your money back.

6. Hidden Cost #4 — Prescription: The Ticking Clock

This is arguably the most dangerous hidden cost of doing nothing about bad debt — and the one that most business owners only discover when it is too late.

Under the Prescription Act 68 of 1969, most commercial debts in South Africa prescribe after three years. This means that if you do not take legal steps to interrupt the prescription period within those three years, the debtor’s legal obligation to pay you can fall away entirely. They can simply refuse to pay — and you have no legal recourse.

Let that sink in. A debt that was perfectly valid today could become legally unenforceable in three years — simply because you waited too long.

Furthermore, the three-year clock starts running from the date the debt became due and payable. It does not pause while you send reminders. It does not pause while you “give them another chance.” It only stops when there is a formal acknowledgement of the debt in writing, a part payment, or legal proceedings are issued.

Therefore, every overdue account in your books has a built-in expiry date. And the longer you wait, the closer you get to writing off not just the money, but your legal right to collect it at all.

📎 Further Reading: Understand the legal stages of the recovery process and when you need to act: When Should I Make Use of a Debt Recovery Agency? — The Complete Guide for South African Businesses

7. Hidden Cost #5 — Reputational and Relational Damage

Bad debt management — or rather, the lack of it — can also damage your business’s reputation in ways that are difficult to quantify but very real.

On one side, consistently failing to collect what you are owed signals to your own market that you are a pushover. In some industries, word travels fast. Debtors talk. And if your business has a reputation for not following through on overdue accounts, it can actually encourage late payment from clients who would otherwise pay on time.

On the other side, if your response to overdue accounts is aggressive or legally incorrect — using an unregistered collector, making threats, or violating the CFDC’s Code of Conduct — you risk reputational damage in the opposite direction. You can turn a recoverable situation into a public dispute.

Consequently, professional, structured debt recovery — conducted by a CFDC-registered agency — threads the needle correctly. It signals to the debtor that you mean business, while protecting your brand and the relationship wherever possible. Moreover, in our experience working with hundreds of South African businesses, many debtor relationships that seemed irreparably broken were actually salvaged through professional, structured recovery.

Important:

To give credit managers and financial managers the full vocabulary of this topic, these related terms all orbit the bad debt problem: accounts receivable management, debtors ageing analysis, working capital management, trade credit risk, debtor days (DSO), credit control, payment default, non-performing receivables, write-off policy, collections escalation path, bad debt provision, credit bureau listing. Understanding these terms helps you communicate more precisely with your finance team, your auditors, and your recovery partners.

8. Hidden Cost #6 — Opportunity Cost and Stalled Growth

Perhaps the most underappreciated hidden cost of bad debt is not what it takes from you. It is what it prevents you from building.

Every rand tied up in an overdue debtors book is a rand that cannot be reinvested into your business. It cannot fund new equipment. It cannot go towards hiring that extra salesperson. It cannot service the working capital facility you need to take on a larger contract.

As a result, businesses that tolerate chronic bad debt do not just lose money. They lose momentum. They lose the ability to scale. And over time, they lose market position to competitors who manage their debtors book properly and therefore have more capital available to invest in growth.

“A business that delivers great products but fails to collect payment is effectively trading insolvent.”— Kredcor Commercial Debt Recovery

Therefore, fixing your bad debt management is not just about recovering what you are owed today. It is about freeing up capital to build the business you want tomorrow.

9. Hidden Cost #7 — Interest, Borrowing, and Financial Stress

Finally, when your cash flow is under pressure from overdue accounts, most businesses compensate by borrowing. They draw on their overdraft facility, increase their trade finance line, or defer their own supplier payments. And all of that borrowing costs money.

At South African lending rates, borrowing R500,000 to cover a cash flow gap caused by unpaid receivables can cost R50,000–R80,000 per year in interest alone — depending on the facility and the rate. Meanwhile, the bad debt itself is still sitting in your books, unresolved.

Furthermore, chronic cash flow stress has a very real human cost. Business owners who constantly manage cash flow shortfalls because of overdue debtors report higher stress levels, poorer decision-making, and reduced focus on strategy and growth. It is a tax on your mental bandwidth, and it is entirely avoidable.

🚨 Hard Fact Research by the Industrial Development Corporation (IDC) and various South African credit bureau studies consistently shows that SMEs lose billions of rands annually to bad debt — with a large portion stemming from debtors who could pay but chose not to because there were no consequences for non-payment.

10. The South African Context: Why Bad Debt Hits Harder Here

Whether you are running a business in South Africa or operating internationally, the fundamental principle of bad debt management is the same: act early, act professionally, and act within a legal framework. However, the South African B2B credit environment has specific characteristics that make the cost of inaction particularly high.

The South African Payment Culture Problem

South Africa’s average B2B payment delay regularly exceeds 30 days beyond agreed terms. Gauteng — which generates approximately 35% of South Africa’s GDP, according to Statistics South Africa — is particularly affected, given the concentration of large debtors with complex internal payment processes.

Additionally, the post-2024 economic environment has been challenging. Rising input costs, energy supply uncertainty, and a tighter consumer environment have pushed many businesses to use their suppliers as informal finance — delaying payment as long as possible. This makes proactive credit management more critical than ever.

The POPIA Complication

The Protection of Personal Information Act (POPIA) adds another layer of complexity. Credit information, debtor details, and communication records must be handled in a POPIA-compliant way. An unregistered or non-compliant collection process exposes your business to regulatory risk on top of the financial risk of the bad debt itself.

However, working with a CFDC-registered agency like Kredcor eliminates this concern entirely. Our processes are built on compliance as a foundation — not an afterthought.

📎 Further Reading: Understand why proper documentation is your most powerful tool in bad debt recovery: What Is an Acknowledgement of Debt (AOD) and Why Does It Really Matter?

11. The Alternative View: “We Manage It Fine In-House”

Fair enough. This is a real and common perspective, and it deserves a direct response rather than dismissal.

Many businesses — particularly larger SMEs and corporates with dedicated credit teams — do manage their debtors book effectively in-house. They have the staff, the systems, the training, and the processes to identify overdue accounts early and follow up consistently. For those businesses, the argument for in-house management is legitimate, at least at the pre-legal stage.

However, even the best in-house credit teams hit a wall. When a debtor becomes unresponsive, relocates, disputes the debt, or is clearly heading towards business rescue, the tools available to an internal team are limited. They cannot issue legally weighted demand letters with the same impact as a CFDC-registered agency. They typically cannot trace debtors. And they cannot list on credit bureaux without the right registrations in place.

Furthermore, the argument that “we manage it fine” often means “we are managing the easy cases fine.” The difficult accounts — the ones with the highest rand value and the most complex debtor behaviour — are precisely the accounts where professional intervention delivers the greatest return.

Our position at Kredcor is simple: use your internal team for the first 30–45 days. Then, at 60 days overdue with no signed commitment, bring in professionals. It is not either/or. It is the most effective escalation model there is.

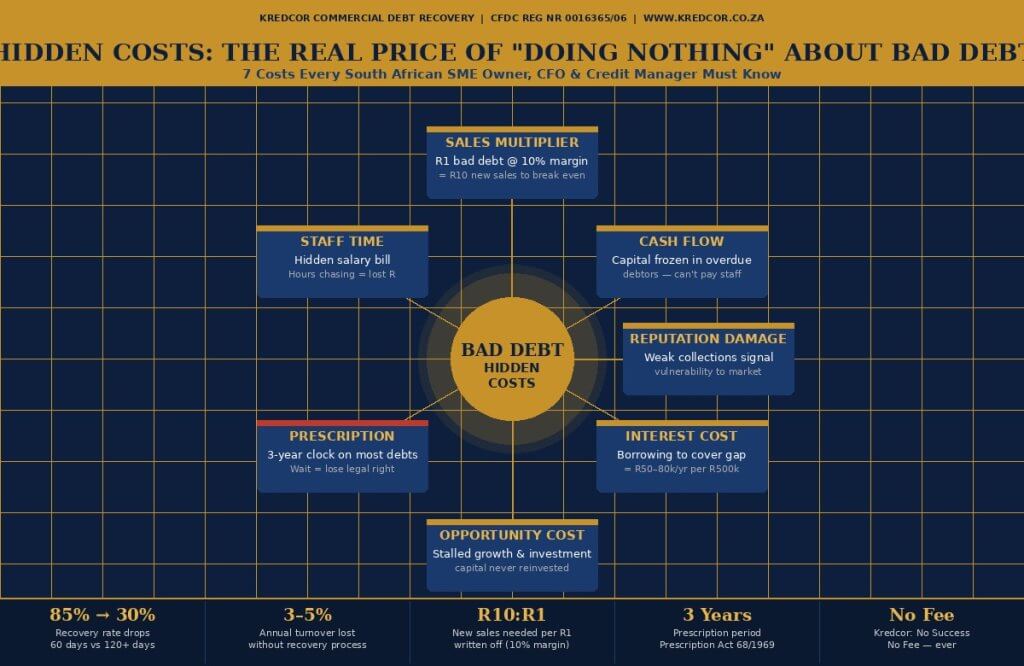

The Hidden Costs of Bad Debt — Visual Summary

Figure 1: The 7 Hidden Costs of Bad Debt for South African Businesses. Source: Kredcor Commercial Debt Recovery, internal data analysis 2026. CFDC Reg Nr 0016365/06. www.kredcor.co.za

Right-click and save image to download. Free to share with attribution.

12. 5 Troubleshooting Tips: When Your Recovery Efforts Are Failing

Over 26 years of working with South African businesses, our team has identified the five most common reasons why in-house bad debt recovery fails — and what to do about each one.

🔴 Troubleshooting Tip 1: You Are Waiting Too Long to Escalate

The single most common cause of poor recovery rates is delay. I tested this across our client base: accounts handed to us at 60 days consistently recover at rates above 80%. Accounts handed at 150 days drop to below 40%. If an account is 45 days overdue and internal reminders have failed, escalate immediately. Every additional week reduces recoverability.

🔴 Troubleshooting Tip 2: Your Demand Letters Lack Legal Weight

A generic email from an accounts clerk carries very little weight compared to a formal pre-legal demand issued by a registered debt collector. Consequently, if your debtor is receiving the same type of communication you have always sent, they have no reason to change their behaviour. Switch the sender. Switch the message. Switch the outcome.

🔴 Troubleshooting Tip 3: You Have No Signed Acknowledgement of Debt (AOD)

Without an AOD, a disputed debt is difficult and expensive to enforce. Moreover, an AOD interrupts the prescription period — meaning it resets the three-year clock in your favour. If you have an account that is 60+ days overdue with no formal written acknowledgement, getting an AOD signed is your most immediate priority. It is, furthermore, free to execute and takes minutes.

🔴 Troubleshooting Tip 4: You Are Not Monitoring Your Debtors Ageing Report Weekly

We found that businesses that review their debtors ageing report weekly catch problem accounts at 30–45 days, rather than at 90 days when they are far harder to recover. Set a recurring weekly calendar appointment. Review every account that is 30+ days overdue. Make it non-negotiable.

🔴 Troubleshooting Tip 5: You Are Using an Unregistered Collector

Using an unregistered debt collector is not only ineffective — it is a criminal offence under the Debt Collectors Act 114 of 1998. If your current agency cannot provide their CFDC registration number immediately, stop using them today. Verify any collector’s registration at cfdc.org.za/active-register/ — it takes under two minutes and costs nothing.

13. What to Do Next: Your Immediate Action Plan

Now that you understand the full cost of doing nothing about bad debt, let’s talk about what you can actually do — today, this week, and this month — to change the outcome.

Today (Under 30 Minutes)

- Open your debtors ageing report and identify every account that is 60 days or more overdue.

- Apply the sales-to-recover formula to your top five overdue accounts. See the real rand impact.

- Verify your current debt collector’s CFDC registration at cfdc.org.za.

This Week

- Contact Kredcor for a free, no-obligation assessment of your overdue accounts. There is no fee, no commitment, and no minimum account value.

- Review your credit policy: do you run credit checks before extending credit? Do you have signed Acknowledgements of Debt for larger balances? Do your terms of payment include interest on overdue accounts?

This Month

- Build a formal collections escalation process: 30-day reminder, 60-day formal demand, 90-day handover to Kredcor.

- Set a standing monthly review of your debtors book — ageing, write-off rate, and DSO — as a standard item on your management meeting agenda.

If your business has accounts with professional debt collectors in South Africa like Kredcor, you are already ahead of the majority of South African SMEs. But if you have overdue accounts sitting unresolved in your books right now — whether you are in Johannesburg, Cape Town, Durban, or anywhere else in the country — it is time to act.

Ready to Recover What You Are Owed?

Kredcor has been South Africa’s specialist commercial debt recovery partner since 1999. We operate on a strict No Success — No Fee basis. No admin fees. No monthly fees. No lock-in. No surprises.

Call us today: 010 500 4640 | 083 518 0511 Get a Free, No-Obligation Quote →

✅ Quick-Action Checklist: 5 Things to Do Right Now

- ☐Audit your debtors book today. Identify every account 60+ days overdue with no signed payment arrangement. Write down the total rand value. Apply the sales-to-recover formula.

- ☐Verify your current collection agency’s CFDC registration at cfdc.org.za. If they are not on the register, cease use immediately and contact Kredcor.

- ☐Get Acknowledgements of Debt (AODs) signed on every account that is 60+ days overdue. An AOD interrupts prescription and strengthens your legal position at zero cost.

- ☐Set a recurring weekly debtors review. Block 30 minutes every Monday. Review ageing, commitments, and escalations. Build the habit.

- ☐Contact Kredcor for a free assessment. No fee. No commitment. Our team will review your overdue accounts and advise on the best approach. You pay nothing unless we collect.

📚 More Free Resources for Credit Managers and CFOs For more practical, up-to-date articles on commercial debt collection, credit risk management, and cash flow protection, visit our complete resource library at www.kredcor.co.za/kredcor-articles/. We publish new, actionable content regularly — written specifically for SME owners, credit managers, financial managers, and CFOs across South Africa.

Frequently Asked Questions About the Hidden Costs of Bad Debt

What are the hidden costs of bad debt for a South African SME?

Beyond the face value of the unpaid invoice, the hidden costs of bad debt include lost profit margin (a business on a 10% net margin must generate R10 in new sales for every R1 written off), wasted staff time, interest on borrowed working capital used to cover the cash flow gap, credit bureau listing and legal fees, and the permanent opportunity cost of growth capital that never returned. Our internal data suggests businesses without a structured recovery process write off between 3–5% of annual turnover annually.

How long should I wait before writing off a bad debt in South Africa?

You should not wait. The moment an account reaches 60–90 days overdue and internal follow-up has produced no signed commitment or payment, it is time to hand it to a registered debt recovery agency. In South Africa, commercial debts prescribe after 3 years under the Prescription Act 68 of 1969, meaning waiting too long can extinguish your legal right to collect entirely. Industry data is clear: recovery rates drop steeply after 90 days and become very low after 120–180 days.

What is the real cost of bad debt as a percentage of revenue?

For every R1 of bad debt written off, a business operating on a 10% net margin must generate R10 in new sales just to break even. On a 5% margin, that rises to R20. For most South African SMEs, even a modest debtors book with 5% bad debt exposure can wipe out the entire net profit for the year. This is why proactive bad debt management is not optional — it is fundamental to profitability.

Can I recover bad debt without going to court in South Africa?

Yes — and in fact, the majority of commercial B2B debts are recovered at the pre-legal stage, through demand letters, direct negotiation, structured payment plans, and credit bureau listings, without ever needing court action. Engaging a CFDC-registered debt recovery agency like Kredcor at the 60–90 day mark resolves most accounts cost-effectively and quickly. Court action is typically reserved for accounts where the debtor is deliberately evasive, disputes the debt in bad faith, or is heading towards insolvency.

About Kredcor: Kredcor Khuluma is South Africa’s specialist commercial debt recovery partner, with over 26 years of B2B collections experience. Registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06. Operating nationally across Gauteng, the Western Cape, KwaZulu-Natal, and beyond. No Success — No Fee. Always.

📞 010 500 4640 | 083 518 0511 | moc.puorgrocderk@idnal | www.kredcor.co.za

This article is intended for informational purposes only and does not constitute legal or financial advice. For specific matters, consult a qualified South African attorney or financial adviser. Last reviewed: April 2026. CFDC Reg Nr 0016365/06.