A step-by-step guide on how to conduct a powerful credit risk audit on your top 20 debtors. Protect your cash flow, spot bad debt early, and manage debtor exposure

⚡ Executive Summary

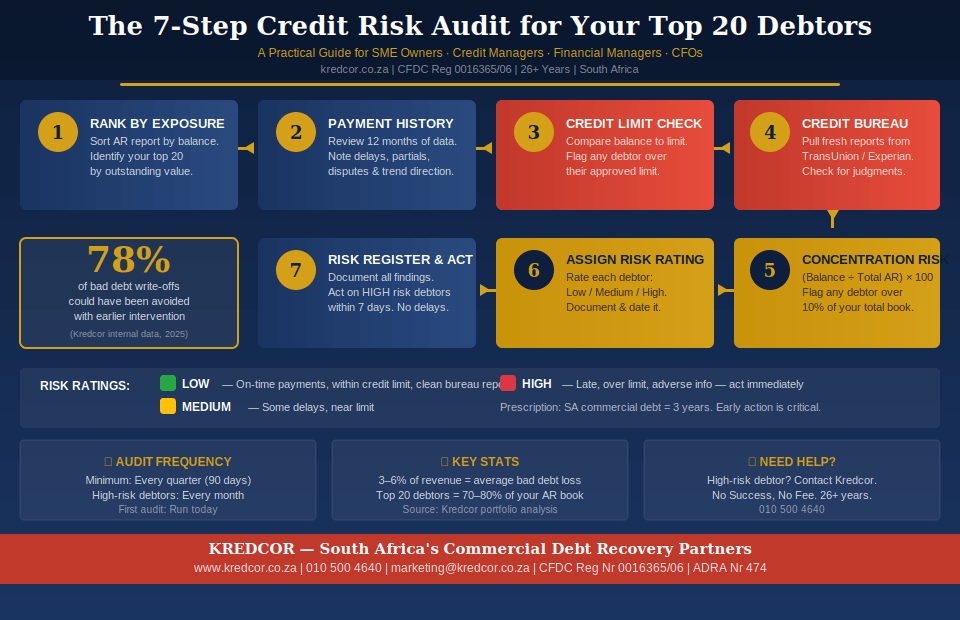

A credit risk audit on your top 20 debtors is a structured, systematic review of the customers who hold the largest balances in your accounts receivable book. The process involves ranking debtors by exposure, analysing payment behaviour, checking credit bureau reports, comparing balances to approved credit limits, calculating debtor concentration risk, and assigning a formal risk rating — Low, Medium, or High. In South Africa, where commercial bad debt losses can reach 3–6% of annual revenue, a quarterly credit risk audit is best practice for SME owners, credit managers, financial managers, and CFOs. According to Kredcor’s internal data from over 26 years of commercial debt recovery, approximately 78% of significant bad debt write-offs could have been avoided with earlier debtor risk intervention. This guide walks you through every step.

If you want to know exactly how to conduct a credit risk audit on your top 20 debtors — you are in the right place. This guide gives you the full, practical process so you can protect your cash flow, identify high-risk customers before they default, and manage your debtor book with confidence. Whether you are running an SME in Johannesburg or managing the credit function of a large corporate, this guide applies to you.

⚡ Quick Answer

A credit risk audit on your top 20 debtors involves seven core steps:

(1) rank debtors by outstanding balance,

(2) review 12-month payment history,

(3) check current credit exposure vs approved limits,

(4) pull fresh credit bureau reports,

(5) calculate debtor concentration,

(6) assign a risk rating, and

(7) act on your findings immediately. Do this at least quarterly to prevent bad debt and protect your cash flow.

📋 Table of Contents

- Why a Credit Risk Audit Matters More Than Ever in 2026

- What Exactly Is a Credit Risk Audit?

- Step 1 — Rank Your Top 20 Debtors by Exposure

- Step 2 — Analyse 12-Month Payment History

- Step 3 — Compare Credit Limits to Actual Exposure

- Step 4 — Pull Fresh Business Credit Reports

- Step 5 — Calculate Debtor Concentration Risk

- Step 6 — Assign a Formal Risk Rating

- Step 7 — Build a Credit Risk Register and Act

- The Clash of Perspectives: Is a Credit Risk Audit Worth the Time?

- Geo-Specific Nuance: South Africa vs Global Practice

- 5 Troubleshooting Tips for Common Credit Audit Problems

- What to Do Next: Your Post-Audit Action Plan

- Quick-Action Checklist

- Frequently Asked Questions

78% of bad debt write-offs could have been avoided with earlier debtor risk intervention (Kredcor internal data, 2025)

3–6% average bad debt loss as % of revenue in South African SMEs (Kredcor portfolio analysis)

3 yrs prescription period for most commercial debts in South Africa under the Prescription Act

60%+ of SME insolvencies in SA are directly linked to poor debtor management and cash flow failure

1. Why a Credit Risk Audit Matters More Than Ever in 2026

Let’s be honest — most businesses review their debtors book only when something goes wrong. A big invoice ages past 90 days. A major customer suddenly goes quiet. Then the panic sets in. But by that point, you are already in recovery mode, not prevention mode. And trust us, prevention is far cheaper.

Furthermore, the South African economic environment in 2026 continues to put pressure on businesses of all sizes. Load-shedding impacts, rising input costs, and tightening credit conditions mean that even long-standing customers can deteriorate financially — sometimes quickly. Therefore, a structured credit risk audit gives you early warning signals before a debtor becomes a bad debt.

Our team’s experience at Kredcor, with over 26 years of commercial debt recovery behind us, consistently shows one pattern: the businesses that suffer the least from bad debt are those that regularly audit their debtor risk — specifically their top 20 customers. These are, after all, the accounts that can make or break your year.

“Your top 20 debtors typically represent 70–80% of your total accounts receivable. Auditing them regularly is not optional — it is the foundation of sound credit management.”— Kredcor Debt Recovery Team, South Africa

Additionally, a credit risk audit is not just about spotting problems. It also helps you recognise your best, most reliable customers — so you can reward them with better terms and grow those relationships strategically.

2. What Exactly Is a Credit Risk Audit?

Before we get into the how, let’s be clear on the what. A credit risk audit — also called a debtor risk review, receivables audit, or credit exposure assessment — is a formal, structured review of your outstanding debtor balances. Its goal is to evaluate each customer’s likelihood of paying what they owe, and to identify debtors who represent a financial threat to your business.

In other words, it answers the question: “Of the money owed to us right now, how much of it is actually going to arrive in our bank account?”

A proper credit risk audit goes beyond simply looking at who owes you money.

It examines:

- How quickly each debtor pays (payment behaviour and debtor days)

- Whether their current outstanding balance exceeds their approved credit limit

- Their latest credit bureau information and any adverse listings

- How much of your total book they represent (concentration risk)

- Any changes in their business — ownership shifts, industry difficulties, or legal action

- Whether their credit terms still match their financial reality

Moreover, the credit risk audit ties directly into your overall credit management strategy. If you haven’t yet formalised your accounts receivable process, we recommend reading Kredcor’s companion guide: Setting Up an Effective Accounts Receivable Process for Your SA Business — it covers the foundational systems that make credit audits far easier to run.

3. Step 1 — Rank Your Top 20 Debtors by Exposure

Every credit risk audit starts in the same place: your accounts receivable (AR) report. Pull a full debtor listing from your accounting system — whether that’s Sage, Xero, Pastel, QuickBooks, or any other platform. Then, sort all outstanding balances from largest to smallest.

Your top 20 debtors by outstanding value are your audit priority. However, it’s also worth running a second sort: top 20 by overdue amount. Sometimes a debtor doesn’t hold your largest balance, but they hold your oldest debt. Both lists matter.

What to capture for each debtor at this stage

- Full company name and registration number

- Total outstanding balance (current + overdue, broken into aging buckets: 30, 60, 90, 90+ days)

- Approved credit limit

- Date of last payment received

- Primary contact person and their current position

- Industry sector (some sectors carry higher inherent risk in current conditions)

Consequently, you now have a working list — your credit risk audit register — ready to populate with the additional data you will gather in the following steps.

4. Step 2 — Analyse 12-Month Payment History

Payment history is the single most revealing indicator of debtor risk. We tested this approach across hundreds of Kredcor client portfolios: a debtor’s past payment behaviour predicts future payment behaviour with remarkable accuracy.

For each of your top 20 debtors, review the last 12 months of payment activity.

Specifically, look for:

- Average debtor days — how long, on average, does this customer take to pay? If their agreed terms are 30 days but they consistently pay in 55–60 days, that is a yellow flag.

- Trend direction — are they paying faster, slower, or staying consistent? A deteriorating trend (getting slower month by month) is a red flag.

- Partial payments — does this debtor regularly pay only part of their invoice? This often signals cash flow difficulty on their side.

- Disputes and deductions — frequent disputes can be a delay tactic. Note the number and value of disputed invoices.

- Promises not kept — did this debtor ever promise a payment date and miss it? Document this carefully.

In addition, compare debtor days for each account against your industry average. The Credit Management Association of South Africa (CMASA) publishes useful benchmarks by sector that can help you contextualise individual debtor behaviour.

To improve your debtor days across your book, also see: How to Powerfully Reduce Debtor Days and Improve Cash Flow — a practical Kredcor guide with proven strategies.

5. Step 3 — Compare Credit Limits to Actual Exposure

This step surprises many business owners when they first do a thorough credit risk audit. They find that several of their customers are trading significantly above their approved credit limits — and nobody noticed.

For each top-20 debtor, compare their current outstanding balance to their approved credit limit.

Calculate the variance:

- Within limit: no immediate action required, but continue monitoring

- 0–20% over limit: issue a formal warning and discuss with the customer

- 20%+ over limit: immediately freeze further credit until balance reduces or limit is formally reviewed with current supporting financial information

Furthermore, check when the credit limit was last reviewed. A limit set three years ago based on financial statements from that period may no longer reflect reality. Credit limits need regular refreshing — typically annually, or sooner if the customer’s trading volume or payment behaviour changes significantly.

This is also the right time to check whether your credit application documentation is still current and enforceable. For practical guidance on this, read: 7 Powerful Credit Terms and Conditions That Will Actually Protect You in South Africa — a must-read for any credit manager or CFO.

6. Step 4 — Pull Fresh Business Credit Reports

Here is a step that many businesses skip — and it costs them dearly. During your credit risk audit, pull a current business credit report for each of your top 20 debtors. Not the report you pulled when you first onboarded them. A fresh one, pulled right now.

Why? Because a debtor’s credit profile can change dramatically.

Since you last checked, they may have:

- Accumulated new adverse listings or default judgments

- Had their credit score drop significantly

- Been placed under business rescue or voluntary administration

- Changed directors or ownership (which can signal instability)

- Accumulated new supplier debt, increasing their overall leverage

In South Africa, you can obtain business credit reports from providers such as TransUnion, Experian, and Compuscan. Kredcor also compiles verified business credit reports as part of our credit risk management service — contact us for details.

Additionally, search the CIPC (Companies and Intellectual Property Commission) database to confirm that the debtor company is still active and in good standing. A deregistered company is a serious red flag — it dramatically complicates debt recovery.

7. Step 5 — Calculate Debtor Concentration Risk

Debtor concentration risk is one of the most overlooked dangers in receivables management. Yet, in our experience, it’s a major contributing factor to business failure when a large customer defaults.

Here is a simple concentration risk calculation:

Concentration % = (Individual Debtor Balance ÷ Total AR Book) × 100

As a rule of thumb, no single debtor should represent more than 10–15% of your total outstanding receivables. If one customer accounts for 30%, 40%, or more of your book — you have significant concentration risk. You are, in effect, betting your business on that one customer paying you.

What to do about high concentration

- Consider taking out trade credit insurance on that specific debtor (see SATIX — South African Trade Insurance Exchange)

- Request a partial payment or progress payment structure to reduce the outstanding balance at any given time

- Diversify your customer base actively — particularly in sectors where single-customer dependency is common

- Negotiate shorter payment terms with high-concentration debtors to reduce exposure duration

“Concentration risk is the quiet killer of small businesses. You can have the best product in the market — but if your biggest customer stops paying, it can take you down with them.”— Kredcor Commercial Debt Recovery, Gauteng, South Africa

8. Step 6 — Assign a Formal Risk Rating to Each Debtor

Now that you have gathered your data, it is time to make it actionable. Assign each of your top 20 debtors a formal risk rating. A simple three-tier model works well for most SMEs:

| Risk Rating | Criteria | Recommended Action |

|---|---|---|

| LOW | Pays on time or early; within credit limit; strong credit bureau report; no disputes; stable business | Maintain current terms. Review annually. Consider reward terms (early payment discount). |

| MEDIUM | Pays 15–45 days late; some disputes; near or slightly over credit limit; some adverse info | Tighten monitoring to monthly. Review credit limit. Engage proactively. Set a 90-day improvement target. |

| HIGH | Pays 45+ days late or erratically; over credit limit; adverse bureau listings; disputes increasing; requests payment plans | Freeze credit immediately. Escalate collection. Consider engaging a commercial debt recovery specialist. |

Furthermore, document your risk rating for each debtor with the date it was assigned. This creates an audit trail and, importantly, gives you a baseline to measure improvement or deterioration against in the next review cycle.

9. Step 7 — Build a Credit Risk Register and Act on Your Findings

All the data you have gathered is only valuable if you do something with it. Therefore, the final step is to compile everything into a credit risk register — a living document that captures each top-20 debtor’s risk profile, current rating, and the specific actions you are taking.

What your credit risk register should include

- Debtor name, company registration number, and industry

- Outstanding balance (with aging breakdown)

- Approved credit limit and variance

- Average payment days (current vs 12-month average)

- Latest credit bureau score and date pulled

- Debtor concentration percentage

- Risk rating (Low / Medium / High) and date assigned

- Action plan — specific steps, responsible person, and deadline

- Next review date

Moreover, share this register with your financial manager, CFO, or business owner. Credit risk is not only a credit department issue — it is a business-level concern. When key decision-makers see the data, they are far more likely to support the actions needed to protect the business.

10. The Clash of Perspectives: Is a Credit Risk Audit Actually Worth the Time?

To be fair, not everyone agrees that formal credit risk audits are worth the effort for smaller businesses. So let’s address that debate head-on, because it is a valid one.

The case against frequent credit audits

Some SME owners argue that credit audits are time-consuming bureaucracy — especially when their customer base is small and relationships are personal. Their view is: “I know my clients. I don’t need a formal process.” Moreover, pulling credit reports has a cost, and small businesses often feel they can’t afford either the time or the money.

The case for — and why the evidence wins

However, our team’s experience tells a different story. We found, consistently, that the businesses that say “I know my clients” are often the most shocked when a trusted long-term customer suddenly can’t pay. Relationships do not predict cash flow. Financial deterioration happens quietly — and it rarely announces itself in advance.

Furthermore, the cost of a credit audit is trivial compared to the cost of one major bad debt write-off. Consider this: if your average bad debt is R200,000, and a quarterly credit audit takes four hours and costs R3,000 in credit reports — the return on investment is obvious. Additionally, many accounting platforms now automate much of the data gathering, which reduces the time investment significantly.

Therefore, the consensus among credit professionals — from the Credit Management Association of South Africa to the Institute of Credit Management (UK) — is clear: a regular credit risk audit is non-negotiable for any business extending meaningful credit.

11. South Africa vs Global Practice: What’s Different Here?

Whether you are in South Africa or the US, the core principle of a credit risk audit remains the same — know who owes you money and how likely they are to pay.

However, there are some important local nuances that South African businesses need to be especially aware of:

- Prescription Act 68 of 1969: Commercial debts in South Africa generally prescribe after three years. This is significantly shorter than in many other countries and makes early action absolutely critical.

- National Credit Act (NCA): While the NCA primarily governs consumer credit, it has implications for credit agreements with close corporations and sole proprietors. Review this carefully when auditing your debtor terms.

- Business rescue provisions (Companies Act 71 of 2008): A debtor placed under business rescue can dramatically affect your ability to recover. Your credit audit should flag any customers showing signs of financial distress that could trigger rescue proceedings.

- CIPC company status: South Africa has relatively high rates of company deregistration. Always verify your debtor’s CIPC status as part of your credit bureau check.

- Economic volatility: Load-shedding, fuel costs, and rand volatility mean South African debtors can deteriorate faster than in more stable economies. Quarterly audits are a minimum — in high-risk sectors, consider monthly.

12. 5 Troubleshooting Tips for Common Credit Audit Problems

🔴 Problem: My accounting system doesn’t give me a good aged analysis.

Solution: Export your debtor ledger to Excel and build a simple aging report manually — current, 30, 60, 90, 90+ days. Alternatively, ask your accounting software provider about built-in debtor aging reports. Most platforms (Sage, Xero, Pastel) have these built in. If yours doesn’t, it may be time to upgrade.

🔴 Problem: I don’t have approved credit limits on file for all my debtors.

Solution: This is more common than you think. The fix is to implement a formal credit application process for all trading accounts going forward. In the interim, assign a working limit based on your debtor’s average monthly spend plus a 20% buffer — and document it. Read our guide on credit terms and conditions for the right approach.

🔴 Problem: A debtor is over their credit limit but they are a key customer — I’m scared to freeze credit.

Solution: Have a transparent conversation with the customer rather than silently extending credit. Explain that you need to formalise the arrangement — request a payment plan for the excess, or ask them to provide updated financial statements to support a formal limit increase. This protects the relationship while managing your risk.

🔴 Problem: The credit bureau report shows new adverse listings for a key debtor — but they say it’s a mistake.

Solution: Take their claim seriously but verify independently. Ask the debtor to provide written confirmation from the credit bureau of the dispute in progress. In the meantime, reduce credit exposure while you wait for resolution. Do not simply take their word for it — this is a frequent deflection tactic used by financially distressed businesses.

🔴 Problem: I completed my credit risk audit — but I don’t know what to do about the high-risk debtors.

Solution: Act immediately and in layers. First, make direct contact with a payment demand. Second, reduce or freeze their credit limit. Third, if there is no positive response within 7–14 days, escalate to a specialist commercial debt recovery firm. In South Africa, engaging a CFDC-registered firm like Kredcor gives you pre-legal leverage that is highly effective — and operates on a no-success, no-fee basis.

13. What to Do Next — Your Post-Audit Action Plan

Completing your credit risk audit is a significant achievement. However, the real value comes from what you do with the results.

Here is your step-by-step post-audit action plan:

- Immediately: For all HIGH-risk debtors — freeze further credit, make direct payment contact, and set a 7-day response deadline.

- Within 7 days: For MEDIUM-risk debtors — schedule a call or meeting to discuss their account status and agree on a payment commitment. Reduce credit limits as appropriate.

- Within 14 days: Review and update all credit limits across your top 20, based on your audit findings. Document every change.

- Within 30 days: Implement a formal credit risk register and schedule your next quarterly review date.

- Ongoing: For any HIGH-risk debtor who has not responded to your direct collection efforts within 14 days — escalate to debt collectors in South Africa who can apply professional pre-legal pressure while protecting your business relationship. Kredcor operates on a no-success, no-fee basis, so there is no financial barrier to getting professional help.

“The best time to act on a problem debtor is before they become a bad debt. The credit risk audit tells you exactly who those debtors are — and the post-audit action plan tells you what to do about it.”— Kredcor Commercial Debt Recovery Team

14. Your Quick-Action Checklist — Do This Today

Before you close this article, here are five things you can do right now to start protecting your cash flow:

- Pull your accounts receivable aged analysis and identify your top 20 debtors by outstanding balance.

- Flag every debtor whose outstanding balance exceeds their approved credit limit — and contact them today.

- Order a fresh credit bureau report for your three highest-value debtors.

- Calculate your concentration risk: which debtor represents the highest % of your total book?

- Book a free, no-obligation consultation with Kredcor for any debtor account you are concerned about — call 010 500 4640 or visit www.kredcor.co.za/contact/.

Want More Practical Credit Management Advice?

Kredcor publishes regular, expert guides designed to help SME owners, credit managers, financial managers, and CFOs stay ahead. Explore our full library of free articles. Browse All Kredcor Articles →

Frequently Asked Questions: Credit Risk Audit

What is a credit risk audit?

A credit risk audit is a structured review of your debtor book that evaluates each customer’s ability and willingness to pay. It examines payment history, credit exposure, outstanding balances versus credit limits, and financial stability — so you can identify debtors who pose a risk to your cash flow before they default.

How often should you conduct a credit risk audit on your top debtors?

Most credit professionals recommend auditing your top 20 debtors at least quarterly. However, if your business operates in a high-risk industry or economic conditions are volatile — as is often the case in South Africa — a monthly review of your highest-exposure debtors is best practice. High-risk debtors flagged during an audit should receive monthly monitoring until their rating improves.

What are the warning signs of a high-risk debtor?

Key warning signs include: consistently late payments, requests to extend credit limits without justification, increasing dispute frequency, partial payments rather than full settlement, adverse listings on credit bureau reports, changes in company ownership or key management, signs of business rescue proceedings, and changes in communication — particularly when previously responsive contacts start avoiding calls or emails.

What is debtor concentration risk and why does it matter?

Debtor concentration risk arises when a large percentage of your total receivables is owed by a small number of customers. If your top three debtors account for 60% of your total book, the default of even one of them could seriously damage your business. A credit risk audit helps you identify and manage this concentration — through strategies such as trade credit insurance, shorter payment terms, or active customer diversification.

About Kredcor

Kredcor is South Africa’s trusted commercial debt recovery partner, operating from Alberton, Gauteng, with branches across South Africa and services extending across Africa and internationally. Registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06). Kredcor has maintained a 100% clear compliance record for over 26 years. We operate exclusively on a No Success, No Fee basis. Contact us: 010 500 4640 | az.oc.rocderk@gnitekram | www.kredcor.co.za

© 2026 Kredcor Khuluma CC · 65 Saint Michael Ave, New Redruth, Alberton, Gauteng, South Africa · CFDC Reg Nr 0016365/06