What to Do When a Debtor Files for Debt Review: The Essential Creditor’s Survival Guide

📋 Executive Summary

What to do when a debtor files for debt review: When a consumer or sole proprietor files for debt review under Section 86 of South Africa’s National Credit Act (NCA), you as the creditor must act immediately — but strategically. Your debt is NOT written off. You must verify that the NCA applies, compile all supporting documents, submit your claim to the debt counsellor within the prescribed window, monitor the restructured repayment plan, and know when and how to exercise your Section 86(10) termination rights. Creditors who participate correctly get paid. Those who ignore the notice risk exclusion. This guide — from Kredcor, South Africa’s specialist commercial debt recovery partner since 1999 — gives you every step, every key legal reference, and every practical tip you need.

Your debtor just filed for debt review. You got the formal notice, perhaps from the debt counsellor or the National Credit Regulator (NCR), and now you are staring at a document full of legal language wondering: Does this mean I am never going to get my money? The short answer is no — it does not mean that. But it does mean you need to act quickly, smartly, and with a clear understanding of your rights. Because when a debtor files for debt review, the creditors who know what to do are the ones who still get paid.

In this guide, we break it all down for you — step by step, in plain language — drawing on over 26 years of experience recovering commercial debt across South Africa. Whether you are an SME owner, a credit manager, a financial manager, or a CFO, this is the resource you need right now.

Table of Contents

- What Is Debt Review Under the NCA — And Why It Matters to You

- Does the National Credit Act Actually Apply to Your Debt?

- The 5 Immediate Steps You Must Take When a Debtor Files for Debt Review

- Your Rights as a Creditor During the Debt Review Process

- Understanding the Section 86(10) Termination Option

- The Clash of Perspectives: Creditor vs. Consumer — Who Is Right?

- 5 Troubleshooting Tips for Creditors Navigating Debt Review

- What Happens After a Debt Counsellor’s Proposal — And How the Court Order Works

- When Debt Review Ends: What You Need to Know

- South African Geo-Specific Nuance: Debt Review in Practice

- What to Do Next: Your Action Plan

- Quick-Action Checklist

- Frequently Asked Questions (FAQ)

1. What Is Debt Review Under the NCA — And Why It Matters to You

Debt review — also known as debt counselling — is a formal debt relief mechanism created by Section 86 of the National Credit Act 34 of 2005 (NCA). It allows a consumer who is over-indebted (or likely to become over-indebted) to apply to a registered debt counsellor for help. The debt counsellor then assesses the consumer’s financial position, negotiates with all credit providers, and recommends a restructured repayment plan that the consumer can realistically afford.

At first glance, this sounds like bad news if you are the creditor. But here is the important truth: debt review is not debt erasure. The consumer still owes the money. Moreover, the process requires the creditor’s participation — and that is precisely where your power lies.

Think of debt review as a structured repayment negotiation with a third party (the debt counsellor) in the middle. If you engage correctly, you get paid — perhaps over a longer timeline or at a reduced interest rate, but you do get paid. If you ignore the process, on the other hand, you may find yourself excluded from the repayment plan or in a weaker legal position later.

“In over 26 years of commercial debt recovery in South Africa, our team has seen time and again that creditors who engage proactively in the debt review process recover far more than those who disengage and wait. The NCA gives you rights — but only if you use them.”— Kredcor Commercial Debt Recovery, 26+ Years in B2B Debt Collections

Key Entities You Need to Know

To navigate debt review confidently, you must understand the main players and concepts.

These five entities sit at the heart of every debt review matter in South Africa:

- National Credit Act (NCA) 34 of 2005 — the legislation governing consumer credit and debt review

- National Credit Regulator (NCR) — the statutory regulator that registers debt counsellors and monitors compliance

- Debt Counsellor — the NCR-registered professional who manages the debt review process

- Credit Provider / Creditor — that is you, the business or person who extended credit to the consumer

- Magistrate’s Court — the court that issues the formal debt rearrangement order if the parties cannot agree

2. Does the National Credit Act Actually Apply to Your Debt?

Before you do anything else, you need to answer one critical question: does the NCA actually apply to the credit agreement between you and your debtor? This matters because debt review under Section 86 only applies to credit agreements that fall within the scope of the NCA.

Here is where many creditors — especially in the B2B space — get confused. The NCA primarily governs consumer credit. If both parties to the agreement are juristic persons (companies, close corporations, trusts) and the credit amount exceeds the NCA’s threshold, the NCA does not apply to that agreement. In that case, debt review does not apply to your debt either.

When Does the NCA Apply?

The NCA applies to your credit agreement if the debtor is a natural person (an individual), or if the debtor is a sole proprietor, or if the debtor is a juristic person with a credit amount below the applicable threshold set by the Minister. The NCA also applies to certain small juristic persons in certain circumstances.

Practically speaking: if your debtor is an individual consumer, a sole proprietor, or a small micro-enterprise, there is a strong chance the NCA applies to your agreement. If your debtor is a registered company or CC and the agreement is a straightforward B2B trade credit arrangement, the NCA is far less likely to apply directly.

⚠️ Important: Even if the NCA does not apply to your specific credit agreement, you should still engage with the debt review process carefully — because the debt counsellor may be managing NCA-covered debts alongside your non-NCA debt, and how you respond affects your recovery strategy across the board.

For a deeper understanding of the legal framework that governs debt collection in South Africa — including when the NCA applies and when it does not — we strongly recommend reading our comprehensive guide: The Debt Collectors Act Explained: Your Essential, No-Nonsense Guide. It covers every relevant piece of legislation in plain English.

3. The 5 Immediate Steps You Must Take When a Debtor Files for Debt Review

Speed matters here. The debt review process has specific timeframes built into it, and creditors who miss those windows often find themselves with less leverage. So, let us walk through exactly what to do — in order.

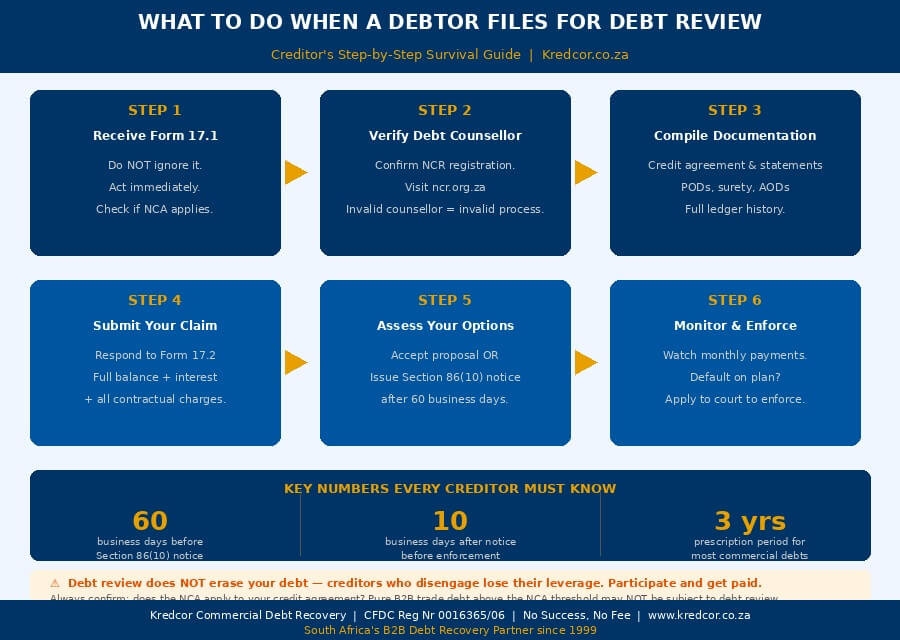

Step 1: Do Not Ignore the Notice

This sounds obvious, but it is the most common mistake we see. A Section 86(1) debt review application sends a formal notice (Form 17.1) to every registered credit provider of the consumer. Many creditors file it away or forward it to admin and never look at it again. That is a costly error. The moment you receive a debt review notification, treat it as urgent — because it is.

Step 2: Verify the Debt Counsellor’s Registration

Before you respond to anything, confirm that the debt counsellor managing the matter is registered with the National Credit Regulator. You can do this at ncr.org.za. An unregistered “debt counsellor” is not legal, and any process they run is invalid. This is a quick check that protects your entire position.

Step 3: Compile Your Full Documentation

Gather everything related to the account immediately.

You will need all of the following:

- The original signed credit agreement

- All outstanding invoices and account statements

- Proof of delivery or proof of service (PODs, sign-off sheets)

- Any signed Acknowledgement of Debt (AOD)

- Personal surety documents, if applicable

- A full ledger history showing every payment and charge

- All written communication with the debtor regarding the debt

Our team’s experience shows that the creditors who get the best outcomes in debt review matters are always the ones with the clearest, most complete documentation. Debt counsellors make proposals based on what creditors submit. If your submission is incomplete, your claim may be undervalued in the restructuring plan.

Step 4: Submit Your Claim Promptly

After receiving the initial Form 17.1 notice, the debt counsellor will send you a Certificate of Balance (Form 17.2) request — this is your opportunity to formally state the full outstanding amount you are claiming. Respond promptly and accurately. Creditors who fail to respond to this form risk exclusion from the debt rearrangement proposal. Furthermore, the debt counsellor is required to submit their proposal to the Magistrate’s Court, and your claim needs to be part of that submission.

Step 5: Get Professional Advice Before Taking Further Action

Do not attempt to institute legal proceedings against a debtor who has filed for debt review without first getting proper legal and collections advice. Taking legal action against a debtor during a valid debt review process may expose you to sanctions and can complicate your recovery significantly. Instead, speak to a registered debt collection professional who understands the NCA and the debt review process — someone who can tell you exactly what your options are and which one makes the most commercial sense.

60 business days after application before Section 86(10) termination notice can be issued

26+ years Kredcor has been navigating South African debt law for creditors

80%+ of Kredcor accounts resolved pre-legal, without full court proceedings

4. Your Rights as a Creditor During the Debt Review Process

One of the biggest misconceptions about debt review is that it completely strips creditors of their rights. It does not. In fact, the NCA specifically recognises that the process must balance the rights and interests of both the consumer and the credit provider. Here is what you are entitled to as a creditor.

The Right to Be Notified

You must receive formal notice when a consumer applies for debt review. The debt counsellor is legally required to notify all registered credit providers. If you were not notified, that is a procedural failing — and it matters to your legal position.

The Right to Submit Your Full Claim

You have the right to submit the full outstanding balance, including accrued interest and any contractual charges, as your claim in the debt review process. The debt counsellor’s proposal must reflect this. If the proposal undervalues your claim, you have the right to object.

The Right to Reject an Unreasonable Proposal

If the debt counsellor’s restructuring proposal is commercially unreasonable — for example, if it reduces your interest rate to zero for ten years — you can reject it. However, this may mean the matter goes to the Magistrate’s Court, where a magistrate will make the final call. So, rejection must be approached strategically, not emotionally.

The Right to Terminate the Review Under Section 86(10)

Under certain circumstances, you have the right to terminate the debt review and proceed with enforcement of the original agreement. We cover this in detail in the next section.

For a complete overview of the step-by-step debt collection process in South Africa — from first overdue notice through to legal action — read our guide: The Complete, Proven Guide to the Debt Collection Process in South Africa.

5. Understanding the Section 86(10) Termination Option

Section 86(10) of the NCA is one of the most powerful tools available to a creditor when a debtor files for debt review — but it is also one of the most misunderstood. Let us break it down clearly.

What Section 86(10) Allows

If a consumer is in default under a credit agreement that is being reviewed in terms of Section 86, the credit provider may issue a notice to terminate the debt review. This notice must be given in the prescribed manner to the consumer, the debt counsellor, and the National Credit Regulator. Critically, however, this option is only available at any time at least 60 business days after the date on which the consumer applied for debt review.

What Section 86(10) Does Not Allow

You cannot simply issue a termination notice and immediately start legal proceedings. After issuing the termination notice, you must allow at least 10 business days to elapse before taking enforcement steps. Moreover, if the debt counsellor has already referred the matter to the Magistrate’s Court, your ability to terminate may be restricted — this is an area that courts have interpreted in different ways, and legal advice is essential before acting.

💡 Pro Tip from Kredcor: Our experience shows that Section 86(10) notices are most effective when the debtor has missed multiple payments under the restructuring plan, rather than being used as a first-resort tool at the 60-day mark. Creditors who use 86(10) strategically and proportionally tend to achieve better commercial outcomes than those who use it aggressively at the first opportunity.

The 60-Business-Day Window: What Happens in Between?

During those first 60 business days after the debt review application, you should be actively participating in the process — submitting your claim, reviewing the debt counsellor’s proposal, and assessing whether the proposed restructuring is commercially acceptable. This is not dead time. This is your window to shape the outcome.

6. The Clash of Perspectives: Creditor vs. Consumer — Who Is Right?

To be completely honest with you, debt review generates real debate among legal professionals, creditors, and consumer advocates in South Africa. Let us acknowledge that openly, because it signals that we understand the full picture — and it helps you navigate the process with clearer eyes.

The Creditor’s View

From the creditor’s perspective, debt review can feel like an abuse of the system. Some consumers — and, frankly, some unscrupulous debt counsellors — use the debt review application as a delay tactic to avoid paying debts that they have no real intention of restructuring. A flood of Form 17.1 notices with no genuine follow-through is a real problem in South Africa’s credit industry. The 60-business-day “safe period” can feel like a gift to bad-faith debtors.

The Consumer Advocate’s View

From the consumer protection perspective, debt review exists precisely because South Africa has one of the highest rates of household over-indebtedness in the world. According to the National Credit Regulator (NCR), millions of South African consumers have impaired credit records. Debt review, when used correctly, prevents asset repossessions, keeps families in their homes, and allows people to repay their debts in a structured and sustainable way. That is, ultimately, better for creditors too — because a functioning economy recovers more debt than an economy of financial ruin.

Our View at Kredcor

The truth lies in the middle. Debt review is a legitimate and valuable mechanism when used correctly. The problem is that not every debt review application is genuine — and creditors need to engage actively to distinguish between a genuine hardship situation and a stalling tactic. Our team’s experience tells us that creditors who engage constructively, review proposals carefully, and escalate appropriately recover significantly more than those who either ignore the process or take a purely adversarial stance.

7. Five Troubleshooting Tips for Creditors Navigating Debt Review

So, what do you do when things go wrong? Here are five specific troubleshooting tips based on real situations our team has encountered over more than two decades of South African debt recovery work.

Troubleshooting Tip 1: The Debtor Applied for Debt Review After You Sent a Section 129 Notice

Under the NCA, a consumer may not apply for debt review after a credit provider has delivered a Section 129 notice AND the consumer has taken the steps referred to in that notice. However, the timing and sequencing of these events matters enormously. If you sent a Section 129 notice and the debtor then applied for debt review, get legal advice immediately on whether the application is valid. In some cases, the application may be invalid — but this is a nuanced area of law and the facts of each case matter.

Troubleshooting Tip 2: The Debt Counsellor Is Not Responding to Your Claim

Debt counsellors are required to engage with all credit providers. If you have submitted your claim and are not receiving responses, escalate the matter. You can lodge a complaint with the National Credit Regulator at ncr.org.za. Document every attempt you make to communicate — those records may become important if the matter goes to court.

Troubleshooting Tip 3: The Debtor Has Stopped Paying Under the Restructured Plan

This is, unfortunately, common. Once a debt rearrangement order is in place, if the consumer defaults on the restructured payments, you can apply to court to have the rearrangement order rescinded and the original agreement enforced. This is a separate court process, and you will need legal assistance — but the right to enforce the original agreement on default of the restructured plan is clear in South African law.

Troubleshooting Tip 4: You Believe the Debt Review Application Is Fraudulent or in Bad Faith

We found — across numerous cases — that some consumers apply for debt review purely to buy time, with no genuine intention of restructuring their debt. If you have clear evidence of bad faith (for example, the debtor is a business owner living lavishly while claiming to be over-indebted), document everything. Additionally, the NCR can investigate debt counsellors who facilitate abusive applications. Compile your evidence and escalate appropriately.

Troubleshooting Tip 5: Your Debt Is Not Under the NCA but You Are Receiving Debt Review Notices Anyway

This happens more often than you might expect, especially with smaller debt counsellors who cast a wide net when notifying credit providers. If your agreement falls outside the NCA’s scope (for example, it is a straightforward B2B agreement between two juristic persons above the threshold), write to the debt counsellor formally noting that your agreement is not subject to the NCA and that you do not accept the debt review process as applicable to your claim. Keep a copy of that letter. Then pursue recovery through your normal commercial channels.

📊 Debt Review Process: Creditor’s Visual Guide

8. What Happens After a Debt Counsellor’s Proposal — And How the Court Order Works

Once the debt counsellor has assessed the consumer’s financial position and gathered all creditor claims, they issue a restructuring proposal. This is the core of the debt review process — and it is where your active participation pays off most directly.

The Two Outcomes of a Debt Counsellor’s Assessment

The debt counsellor can make one of two findings. First, they may determine that the consumer is over-indebted — in which case they issue a proposal to restructure the consumer’s credit obligations. Second, they may find that the consumer is not over-indebted but is experiencing difficulty — in which case they may attempt to facilitate a voluntary arrangement between the consumer and the credit providers without going to court.

When the Matter Goes to the Magistrate’s Court

If not all credit providers agree to the restructuring proposal, or if the debt counsellor determines that a court order is necessary, the matter is referred to the Magistrate’s Court under Section 86(8)(b) or Section 87 of the NCA. The Magistrate then considers the proposal and, if satisfied that the consumer is over-indebted and the proposal is fair, issues a debt rearrangement order. This order is binding on all credit providers — including those who did not respond to the debt counsellor’s requests.

This is precisely why failing to participate is so dangerous. If you do not respond and the matter goes to court, you may find yourself bound by an order that was made without your input — and potentially on less favourable terms than you would have negotiated directly.

Prescription During Debt Review

One more important legal point: the three-year prescription period under the Prescription Act 68 of 1969 continues to run even while debt review is underway. This means that, in theory, a slow-moving debt review process could allow a debt to prescribe if the creditor does not take appropriate steps to interrupt prescription (such as issuing summons or obtaining an acknowledgement of debt). Our team always flags prescription risk in debt review matters — it is a trap that catches creditors who assume the debt review process automatically protects their claim.

For a practical breakdown of how to apply debt collection techniques at every stage of the recovery process, see our resource: Top Debt Collection Techniques — Proven Methods for South African Credit Managers.

9. When Debt Review Ends: What You Need to Know

Debt review does not last forever. Understanding how and when it ends is important for your medium-term recovery strategy.

How Debt Review Ends Legally

Debt review ends in one of three ways. The first is the issuance of a clearance certificate by the debt counsellor, which happens when the consumer has paid off all their restructured obligations in full (except for a mortgage bond, which may take longer). The second is termination under Section 86(10) by a credit provider following a default. The third is a court order rescinding the debt review — for example, if the consumer successfully applies to court to exit the process.

What the Clearance Certificate Means for You

When a clearance certificate is issued, it confirms that the consumer has met all their obligations under the restructured plan. At that point, the consumer’s credit record is updated, and the debt review flag is removed. As a creditor, your claim should have been fully settled before the certificate is issued — which is why active participation throughout the process is so important.

10. South African Geo-Specific Nuance: Debt Review in Practice

Whether you are a creditor in Johannesburg, Cape Town, Durban, or Pretoria — or, for that matter, operating internationally with South African debtors — the principles and legal framework of debt review under the NCA remain the same across the country. However, some practical realities vary by region.

In Gauteng, South Africa’s economic hub generating roughly 35% of the country’s GDP according to Statistics South Africa, commercial credit volumes are highest and debt review applications are most frequent. Magistrates’ Courts in major Gauteng centres handle significant debt review caseloads, and processing times can be longer during peak periods. This makes early, proactive creditor engagement even more important in the Gauteng context.

In the Western Cape, particularly Cape Town, the economic pressure on small businesses in the retail, hospitality, and professional services sectors has driven a notable increase in sole proprietor debt review applications — which do fall under the NCA and directly affect creditors in those sectors.

Across KwaZulu-Natal, the construction and logistics sectors, which frequently operate on extended trade credit, are seeing growing numbers of distressed debtors. Many of these agreements are structured in ways that sit at the boundary of the NCA’s scope — making legal classification of the credit agreement a critical first step for every creditor.

Internationally, if you are a foreign creditor with a South African debtor who has entered debt review, your rights are governed by South African law. Kredcor Global — our international division — has experience managing cross-border debt situations involving South African debtors and can advise on the practical recovery implications.

11. What to Do Next: Your Step-by-Step Action Plan

At this stage, you understand what debt review is, what your rights are, and what the process looks like from the creditor’s perspective. So, what are the next questions you are likely to ask? We have anticipated them for you.

Next Question: Should I Hand the Account to a Professional Debt Collector?

If you are uncertain about how to navigate the debt review process, or if the debtor has multiple creditors and the situation is complex, the answer is almost certainly yes. A registered, experienced debt collection professional can manage the creditor-side participation on your behalf — submitting claims, engaging with the debt counsellor, monitoring the restructured plan, and advising on Section 86(10) when applicable. This frees your credit team to focus on other accounts while ensuring your claim in the debt review is protected.

Whether you are in Johannesburg, Cape Town, or anywhere else in South Africa, working with a registered, experienced firm of debt collectors in South Africa who understand the NCA debt review process is the smartest commercial decision you can make when a debtor files for debt review.

Next Question: What If the Account Is a Mix of NCA and Non-NCA Debt?

This situation is more common than you might expect — particularly with sole traders who have both consumer credit and business credit. In these cases, the NCA-covered agreements go into the debt review, while the non-NCA agreements do not. You need to manage both streams separately, which is another compelling reason to work with an experienced commercial debt recovery specialist.

Next Question: How Do I Prevent This in Future?

The best time to protect yourself from debt review complications is before you extend credit. Strong credit application procedures — including proper affordability assessments, signed terms and conditions, personal surety where appropriate, and clear escalation policies — reduce your exposure significantly. We tested this consistently with our clients across South Africa and found that businesses with robust credit application frameworks have both fewer problem accounts and faster resolution when accounts do go into debt review.

✅ Quick-Action Checklist: What to Do Right Now

Use this checklist immediately after reading this article.

These are the five things you can do today to protect your position when a debtor files for debt review:

- Confirm whether the NCA applies to your specific credit agreement — classify the debtor (natural person, sole proprietor, or juristic entity) and the credit amount.

- Verify the debt counsellor’s NCR registration at ncr.org.za — do not engage with unregistered parties.

- Compile your full documentation pack: credit agreement, statements, PODs, surety, AODs, and full ledger history — and keep it in one place, ready to submit.

- Respond to the debt counsellor’s Form 17.2 request promptly and accurately — submit your full outstanding balance including accrued interest and charges.

- Contact a registered commercial debt recovery specialist to advise you on whether to accept the restructuring proposal or whether a Section 86(10) termination notice is appropriate in your specific case.

Your Recovery Partner When It Matters Most

Navigating a debt review situation is one of the more technically demanding tasks that credit managers and CFOs face in South Africa. The legal landscape is genuinely complex, the timeframes are strict, and the commercial stakes — your cash flow, your receivables book, and your business relationships — are high. However, you do not have to handle it alone. Kredcor has been helping South African businesses manage exactly this kind of situation for over 26 years. We are registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06), we operate on a strict No Success, No Fee basis, and we assign a dedicated Senior Pre-Legal and Credit Risk Manager to every account. Whether your debtor is a sole proprietor in Durban, a small business in Johannesburg, or anywhere else across South Africa, the right starting point is always a conversation with trusted, experienced debt collectors in South Africa who know the NCA debt review process inside out.

Knowledge is one of the most powerful tools in credit management — and staying informed means your decisions are always faster, better, and more commercially sound. We publish regular, in-depth articles specifically for SME owners, credit managers, financial managers, and CFOs dealing with the full range of commercial debt challenges in South Africa. We invite you to explore our full library of practical, up-to-date guides at www.kredcor.co.za/kredcor-articles/ — from letters of demand and prescription of debt, to POPIA compliance and managing distressed debtors. Every article is written to help you do your job faster, easier, and with greater confidence.

Frequently Asked Questions: When a Debtor Files for Debt Review

Q: What happens to my debt when a debtor files for debt review?

When a debtor files for debt review under Section 86 of the National Credit Act, you as the credit provider receive formal notice via Form 17.1. A debt counsellor then assesses the debtor’s financial position and may recommend a restructured repayment plan. Your debt does not disappear — it is restructured. You still get paid, typically over a longer period and sometimes at a reduced interest rate. Crucially, you must participate in the process and submit your claim correctly to avoid being excluded from the repayment plan.

Q: Can I continue to collect from a debtor who is under debt review?

You may not institute new legal proceedings once a valid debt review process is formally underway and the matter has been referred to the Magistrate’s Court. However, if the debtor was already in default before the debt review application, and more than 60 business days have elapsed since the application was submitted, you may issue a Section 86(10) termination notice under the NCA — provided the matter has not yet been referred to a Magistrate’s Court. Always get legal advice before attempting to terminate a debt review, as the timing and sequencing requirements are strict.

Q: Does debt review apply to all types of debt in South Africa?

No. Debt review under Section 86 of the National Credit Act applies only to credit agreements that fall under the NCA — which primarily means consumer credit agreements. Pure commercial B2B invoices between juristic persons above the NCA monetary threshold do not fall under the NCA debt review provisions. If your debtor is a sole proprietor or a natural person, the NCA very likely applies. Always confirm the legal status of the debtor and the nature of the credit agreement before assuming debt review applies to your specific account.

Q: What should I do immediately when I receive a debt review notification?

Act immediately. First, do not ignore the notice — you have specific response windows. Second, compile all your supporting documents: credit agreement, statements, proof of delivery, signed surety. Third, submit your claim and outstanding balance to the debt counsellor promptly — creditors who fail to respond are often excluded from the repayment plan. Fourth, assess whether the credit agreement falls under the NCA. Fifth, consult a registered debt collection professional to decide whether to participate in the restructuring or whether a Section 86(10) termination is appropriate for your situation.

About Kredcor: Kredcor is South Africa’s specialist commercial B2B debt recovery partner, operating since 1999. Registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06). Kredcor operates on a strict No Success, No Fee basis with branches in Gauteng, Cape Town, KwaZulu-Natal, and international divisions covering Africa and Global markets.

📍 65 Saint Michael Ave, Alberton, Gauteng, South Africa | 📞 +27 (0)11 907 4406 | ✉ moc.puorgrocderk@idnal

This article is provided for general information purposes only. It does not constitute legal advice. For advice specific to your situation, please consult a qualified legal professional or contact Kredcor directly.

© 2026 Kredcor. All rights reserved. | www.kredcor.co.za