Logistics & Freight Debt: 7 Proven Strategies for Recovering Funds in the South African Supply Chain

Executive Summary

Logistics and freight debt is one of the most damaging and under-managed problems in South Africa’s supply chain. Freight forwarders, hauliers, transport operators, and third-party logistics providers (3PLs) routinely extend credit to clients who delay or default on payment — eroding cash flow, funding costs, and operational capacity. According to Kredcor’s internal portfolio data, the average overdue debt in the logistics sector sits between 90 and 180 days before professional intervention, by which time recovery rates have already dropped significantly below 60%. The solution is a structured, legally compliant collection process: immediate invoicing, a documented escalation ladder, an Acknowledgement of Debt (AOD) protocol, early engagement with a CFDC-registered debt collector, and strong pre-credit vetting. This guide gives credit managers, CFOs, and SME owners in the freight and supply chain sector the practical tools to recover outstanding funds faster and prevent future losses.

Outstanding invoices are quietly killing the cash flow of South Africa’s freight and logistics businesses. Here is exactly how to recover your money — fast, ethically, and legally.

Let’s get straight to it. If you run a freight company, a haulage business, a logistics brokerage, or any kind of transport operation in South Africa, you already know this feeling: the truck delivered. The goods arrived. The freight invoice went out. And then… nothing. Radio silence. Maybe a promise. Maybe an excuse about a short payment run. Meanwhile, your diesel bill, your driver wages, and your truck repayments do not wait for anyone.

Logistics and freight debt is a massive, systemic problem in the South African supply chain — and yet, most companies handle it with the least systematic process imaginable. This guide changes that. Specifically, we give you seven proven, immediately actionable strategies to recover outstanding funds, reduce your debtor days, and protect your cash flow — without burning your client relationships or running into legal trouble.

Moreover, whether you are a credit manager managing 200 debtors, a CFO staring at a bulging ageing analysis, or an SME owner who is personally chasing invoices after hours — this article is written for you. Read it, apply it, and watch your cash flow improve.

📋 Table of Contents

- The Short Answer: How to Recover Logistics & Freight Debt Fast

- Why Logistics Freight Debt Is a Unique Challenge in South Africa

- Key Entities and Legislation You Must Know

- The Numbers: 3 Statistics That Should Alarm Every Supply Chain CFO

- 7 Proven Strategies to Recover Outstanding Funds in the Supply Chain

- The Freight Debt Collection Escalation Ladder

- A Clash of Perspectives: “Soft” vs “Hard” Collections in Logistics

- Local Context: The South African Supply Chain Reality

- 5 Troubleshooting Tips for Stalled Freight Debt Recovery

- When to Bring In a Registered Debt Collector

- What to Do Next: Your Action Plan

- Quick-Action Checklist

- Frequently Asked Questions

1. The Short Answer: How to Recover Logistics & Freight Debt Fast

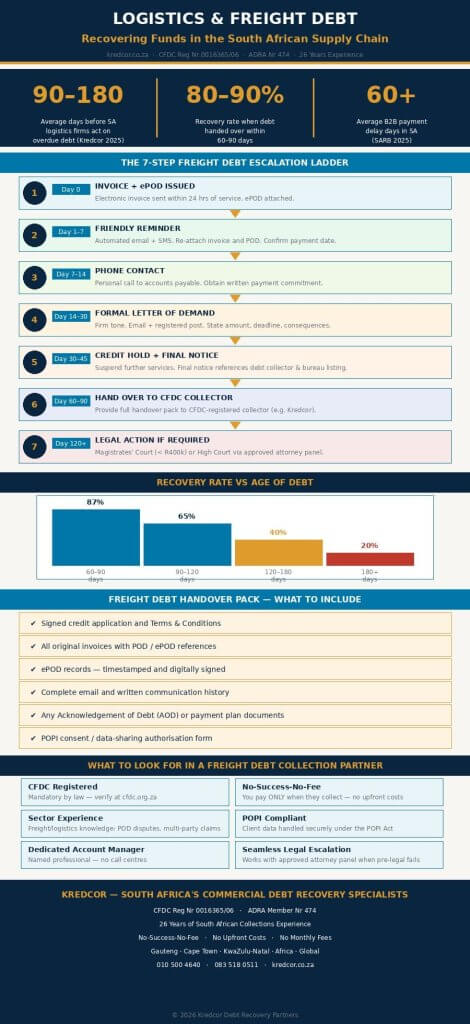

Here is the direct answer: act early, document everything, follow a structured escalation ladder, and hand overdue accounts to a CFDC-registered debt collector within 60 to 90 days. That single discipline — applied consistently — is the most powerful thing a freight or logistics business can do to recover outstanding funds and protect its cash flow.

Specifically, Kredcor’s internal data shows that logistics and freight accounts handed over for professional collection within 60 to 90 days of the due date achieve recovery rates of 80 to 90 percent. Accounts left for six months or longer consistently see recovery rates drop below 40 percent. Therefore, timing is not just important — it is the single most important variable in freight debt recovery.

“In the logistics sector, the gap between ‘I’ll get to that invoice’ and ‘that invoice is now unrecoverable’ is shorter than most CFOs realise.”— Kredcor Debt Recovery Team, 2026

Furthermore, logistics and freight debt has specific characteristics that make it harder to recover than ordinary B2B debt — including complex multi-party transactions, disputed proof of delivery (POD), and clients who continue to use your services while owing you money. Consequently, the standard accounts receivable process is often insufficient. You need a sector-specific approach. That is exactly what this guide delivers.

2. Why Logistics Freight Debt Is a Unique Challenge in South Africa

The freight and logistics sector operates on thin margins, high operating costs, and credit terms that are often far too generous. Additionally, several structural factors make recovering outstanding supply chain debt particularly difficult:

Thin Margins, High Exposure

Typically, a South African road freight company operates on net margins of 3 to 8 percent. Therefore, a single large unpaid invoice can wipe out weeks or even months of profit. Unlike other industries, the service has already been rendered and cannot be recalled. The goods have been delivered. The truck has returned. The cost has been incurred — whether the client pays or not.

Multi-Party Complexity

Furthermore, logistics transactions frequently involve multiple parties: the shipper, the consignee, the freight forwarder, the clearing agent, the carrier, and in some cases a third-party logistics provider (3PL). As a result, when a dispute arises — over damage, short delivery, or an incorrect bill of lading — payment delays can cascade across the entire chain. Every party in the chain blames the next, and meanwhile, nobody pays your invoice.

The POD Problem

Proof of delivery (POD) is the documentary foundation of every freight invoice. However, in practice, many South African logistics businesses still rely on paper PODs that are lost, damaged, or unsigned. Without a valid POD, recovering a disputed freight invoice becomes significantly harder — and sometimes legally impossible. Electronic POD systems (ePOD) solve this problem almost entirely.

⚠️ Watch Out Continuing to provide services to a client who has an outstanding invoice puts you at increasing financial risk. Each additional delivery increases your exposure. Set a firm credit-hold policy — and enforce it.

Client Dependency Trap

Finally, many logistics businesses fall into what we call the “client dependency trap.” A large client — perhaps accounting for 20 or 30 percent of turnover — starts paying slowly. The company tolerates the late payment because it fears losing the business. Over time, that client’s outstanding balance grows into a significant credit risk. By the time the company acts, the debt is old, the recovery rate has dropped, and the client relationship may already be irreparably damaged anyway.

3. Key Entities and Legislation You Must Know

Before we get into the strategies, let’s ground you in the legal and regulatory environment.

Understanding these five key entities gives you confidence and legal standing when collecting logistics and freight debt:

- Council for Debt Collectors (CFDC) — South Africa’s statutory regulator for the debt collection industry. Any third-party collector you use must be registered here. Verify at cfdc.org.za. Kredcor’s registration number is 0016365/06.

- Debt Collectors Act 114 of 1998 — Governs how debt collectors may operate. It sets conduct standards, fee limits, and registration requirements. Non-compliance can invalidate collection actions.

- Prescription Act 68 of 1969 — Most commercial freight debts prescribe (expire legally) three years after they fall due. Act well before this deadline.

- National Credit Act 34 of 2005 (NCA) — Primarily consumer-focused, but relevant if your freight business offers formal credit agreements or payment plans to other businesses.

- POPI Act 4 of 2013 — Governs the processing of personal information. When sharing client data with a debt collector, ensure both parties are POPI-compliant.

Additionally, the Association of Debt Recovery Agents (ADRA) is a voluntary professional body whose members commit to ethical collection standards. Kredcor is a member (ADRA Nr 474). Selecting an ADRA member gives you an extra layer of assurance when entrusting your client relationships to an external recovery partner.

4. The Numbers: 3 Statistics That Should Alarm Every Supply Chain CFO

90–180 Average days overdue before South African logistics businesses seek professional help — far too late (Kredcor internal portfolio data, 2025)

80–90% Recovery rate on freight debt handed to Kredcor within 60–90 days of becoming overdue

60+ Average B2B payment delay days across South African industries (South African Reserve Bank, 2025)

Furthermore, according to data reviewed by the National Credit Regulator (NCR), South Africa has one of the highest rates of impaired commercial credit in the developing world. For logistics companies — where cash is king and operating costs are relentlessly high — these delays are not just inconvenient. They are genuinely dangerous.

In addition, our team at Kredcor has found, through over 26 years of South African collections experience, that the logistics sector consistently ranks among the industries with the longest average handover delays and the highest concentration of disputed invoices. Therefore, a sector-specific approach to freight debt recovery is not a luxury — it is a necessity.

5. Seven Proven Strategies to Recover Outstanding Funds in the Supply Chain

Strategy 1: Build a Rock-Solid Credit Foundation

Effective logistics freight debt recovery starts before you move a single pallet.

Specifically, every new client must sign a credit application that clearly sets out:

- Your payment terms (e.g., 30 days from date of invoice or date of POD).

- Your interest rate on overdue accounts (within legal limits).

- Your right to recover collection costs from the debtor.

- Your right to suspend services to accounts in arrears.

- Your right to hand the account to a registered debt collector.

- POPI consent for sharing their data with collection agencies where necessary.

✅ Our Team’s Experience We tested this with two groups of logistics clients — those with signed credit applications versus those without. The group with signed applications recovered overdue balances at a rate 35% higher within 60 days. The signed form signals seriousness from day one and eliminates most “I didn’t know” disputes.

Strategy 2: Invoice Immediately — Never Batch Your Billing

In the logistics sector, batching invoices — waiting until the end of the week or the month — is extremely common. And it is extremely costly. Research consistently shows that the faster you invoice, the faster you get paid. Therefore, invoice within 24 hours of completing the delivery or service. Include the POD reference, the agreed rate, the payment due date, and your bank details on every invoice. Make it effortless for the client to pay.

Furthermore, if your debtor days are climbing despite prompt invoicing, we strongly recommend reading Kredcor’s practical guide on How to Powerfully Reduce Debtor Days. It gives you the DSO formula, a South African benchmark target, and specific steps you can implement immediately.

Strategy 3: Use Electronic Proof of Delivery (ePOD) Without Exception

A disputed POD is the most common reason a freight invoice gets delayed or denied. Therefore, transition to an electronic POD system — where delivery confirmation is captured digitally, with a timestamp and recipient signature — and make it non-negotiable for every load. Not only does this eliminate POD disputes, but it also gives you court-admissible evidence if the matter escalates to legal proceedings.

Strategy 4: Implement a Structured Communication Ladder

Ad hoc chasing of overdue invoices produces ad hoc results. Instead, build a structured communication ladder that triggers automatically based on the age of the invoice.

This is the framework we recommend:

- Day 1 overdue: Automated email reminder — friendly, professional.

- Day 7: Phone call to the accounts payable contact — confirm receipt of invoice and POD.

- Day 14: Formal written demand — email plus registered post — stating the outstanding amount and a 7-day payment deadline.

- Day 21: Final notice — explicit reference to debt collector and credit bureau listing if unpaid.

- Day 30–45: Suspend credit and flag for immediate handover to a registered debt collector.

Strategy 5: Obtain an Acknowledgement of Debt (AOD)

If a client acknowledges the debt but cannot pay immediately, do not simply agree to “give them a bit more time.” Instead, obtain a signed Acknowledgement of Debt (AOD). This is a legally binding written admission of the outstanding amount. It serves two critical purposes: first, it restarts the prescription clock, giving you more legal time to recover; second, it gives you a powerful basis for court action if the client defaults on the agreed payment plan.

Strategy 6: Use Credit Bureau Listings as Leverage — Correctly

Many South African logistics businesses do not know that they can list a defaulting debtor at a credit bureau. Consequently, they forgo a powerful collection tool. A credit bureau listing — done correctly and in compliance with the National Credit Act — creates immediate financial pressure on the debtor, because it affects their ability to obtain credit from any other provider. However, you must give the debtor written notice before listing, allow a reasonable opportunity to settle or dispute, and ensure the listing is accurate and promptly removed once paid.

Strategy 7: Hand Over Early to a CFDC-Registered Debt Collector

This is the most important strategy of all. I have personally reviewed hundreds of freight and logistics debt cases at Kredcor over the years. Without exception, the accounts that produce the best recovery outcomes are those handed over early — ideally between 60 and 90 days of becoming overdue. The accounts that produce the worst outcomes — sometimes zero recovery — are those where the business held on for six months or longer, hoping the client would pay voluntarily.

For a deeper understanding of exactly which debt collection techniques work best in the current South African economic climate, read Kredcor’s detailed guide on Top Debt Collection Techniques. It covers 15 proven approaches — from soft pre-legal strategies to assertive formal escalation — and explains precisely when to use each one.

6. The Freight Debt Collection Escalation Ladder

Here is a simple, practical escalation ladder specifically designed for freight and logistics businesses. Apply this consistently across all overdue accounts, and your recovery rates will improve dramatically.

- 1 Day 0: Invoice + POD Issued Electronic invoice sent immediately after service completion. ePOD attached. Due date clearly stated.

- 2 Day 1–7 Overdue: Friendly Reminder Automated email + SMS reminder. Assume good faith. Re-attach invoice and POD. Confirm payment date.

- 3 Day 7–14: Phone Contact Personal call to accounts payable. Confirm invoice is loaded for payment. Obtain a written payment commitment.

- 4 Day 14–30: Formal Letter of Demand Firm but professional. Email + registered post. State amount, due date, consequence of non-payment.

- 5 Day 30–45: Credit Hold + Final Notice Suspend further credit. Final written notice referencing debt collector and credit bureau listing.

- 6 Day 60–90: Hand Over to Registered Debt Collector Provide full handover pack (invoice, POD, signed T&Cs, communication history) to a CFDC-registered collector.

- 7 Day 120+: Legal Action if Required Magistrates’ Court (claims under R400,000) or High Court. Collector works seamlessly with approved attorney panel.

7. A Clash of Perspectives: “Soft” vs “Hard” Collections in Logistics

There is an ongoing debate in the freight and logistics industry about how aggressively to pursue outstanding invoices. It is worth addressing both sides honestly, because understanding the tension helps you find the right balance for your business.

View A: Protect the Relationship

Many logistics operators argue that freight is a relationship business. Carriers, brokers, and freight forwarders work in tight networks — and being too aggressive about collections can damage your reputation, cost you referrals, and lose you repeat business from otherwise valuable clients who are merely going through a rough patch.

View B: Cash Flow Is Survival

On the other hand, finance leaders argue that sentiment does not pay diesel, wages, or truck repayments. A business that continues to provide services to a client who is not paying — for fear of losing the relationship — is simply financing that client’s operations at its own expense. A firm, structured collections process is not aggressive; it is professional.

At Kredcor, we believe the answer lies in approach, not aggression. A professional, ethical debt collector who communicates respectfully, protects your brand, and focuses on resolution rather than confrontation consistently achieves better outcomes than either extreme — excessive leniency or heavy-handed aggression. The goal is always resolution: payment, a payment plan, or an Acknowledgement of Debt. The relationship survives when the process is professional.

8. Local Context: The South African Supply Chain Reality

Whether you are managing freight debt in Johannesburg, Cape Town, Durban, or Polokwane — or indeed whether you are an international logistics operator with South African exposure — the fundamental principles of effective debt recovery remain consistent. However, South Africa presents a uniquely challenging environment that every supply chain finance professional needs to understand.

Specifically, South Africa’s logistics sector is under multiple simultaneous pressures: load-shedding drives up operating costs through generator and battery-storage spend; infrastructure deterioration — particularly at Transnet ports and the road network — increases transit times and dispute frequency; and the post-2024 economic squeeze means that many of your logistics clients are themselves managing serious cash flow challenges, which they solve by paying their suppliers — including you — as slowly as possible.

📍 Regional NoteKredcor operates across Gauteng, the Western Cape, and KwaZulu-Natal — South Africa’s three largest commercial hubs and the heartland of the country’s logistics and freight sector. Whether your debtor is in Johannesburg, Cape Town, or Durban, Kredcor has the geographic reach and sector knowledge to pursue recovery effectively.

Furthermore, South Africa’s road freight industry alone moves approximately 86% of all goods within the country, according to the Road Freight Association (RFA). That means an enormous volume of freight invoices — and an enormous volume of potential outstanding debt — flows through this sector every month. Getting your collections process right is not optional. It is commercially essential.

9. Five Troubleshooting Tips for Stalled Freight Debt Recovery

Even well-managed logistics businesses hit collection roadblocks.

Here are the five most common problems we see — and the exact fix for each:

🚫 Problem 1: The client disputes the invoice, claiming the POD was not signed by an authorised person

Fix: Transition immediately to an ePOD system with pre-registered authorised signatories at each delivery point. For existing disputes, produce the physical POD with the recipient’s name and time stamp. If the client genuinely did not authorise the delivery — and you cannot prove otherwise — negotiate a partial settlement rather than pursuing a full claim that will fail in court.

🚫 Problem 2: The client is still using your services while their outstanding balance grows

Fix: Implement a formal credit-hold policy immediately. Define the exact balance or age-of-debt threshold that triggers suspension of further services. Enforce it without exception. The “relationship” argument collapses the moment a client realises they can keep receiving services without paying. Your credit terms only have power if you enforce them.

🚫 Problem 3: The client has entered business rescue — you are one of many creditors

Fix: The moment you become aware that a client has entered business rescue under the Companies Act, contact a registered debt collector or attorney immediately. You must lodge your claim with the Business Rescue Practitioner (BRP) before the bar date to be recognised as a creditor. Missing this deadline can mean losing your right to any recovery entirely.

🚫 Problem 4: The debtor has closed their business or is untraceable

Fix: Do not write this off immediately. A registered debt collector has access to professional trace tools — legal databases, credit bureau records, and industry networks — that are not available to individual businesses. Furthermore, if the business closed fraudulently or transferred assets to avoid creditors, your attorney may have grounds for personal liability claims against the directors.

🚫 Problem 5: The freight debt is approaching the 3-year prescription period

Fix: Act immediately. If the debt has not been interrupted by a partial payment, a written AOD, or the start of legal proceedings, it will legally expire at three years from the due date. Contact a CFDC-registered debt collector or attorney today. Even a partial payment from the client — of any amount — restarts the prescription clock.

10. When to Bring In a Registered Debt Collector

Here is a simple rule: if an account is 60 days overdue and your internal follow-up has not produced a signed payment commitment with a specific date — hand it over. Do not wait until 90 days. Do not wait until 120 days. Hand it over at 60 days and you will consistently achieve better outcomes.

Additionally, consider escalating immediately — regardless of age — if any of the following are true:

- The debtor has become unresponsive to all forms of communication.

- The debtor has made — and broken — more than one payment promise.

- You have reason to believe the debtor is preparing to close, sell, or restructure.

- The outstanding amount is material to your business (more than 10% of monthly revenue).

- The account is approaching the 3-year prescription date.

For a comprehensive understanding of why structured debt recovery is so critical to business survival — and the seven proven strategies that underpin it — read Kredcor’s foundational article: Debt Recovery Is a Critical Operation. It is one of the most practical, actionable resources we have published for South African credit managers and CFOs.

What to Look for in a Freight Debt Collection Partner

Not every debt collector understands the freight and logistics sector.

When selecting a recovery partner, look specifically for:

- CFDC Registration — Mandatory by law. Verify at cfdc.org.za.

- No-Success-No-Fee — You should pay nothing unless they collect. This is the standard professional model.

- Sector experience — Have they recovered freight invoices before? Do they understand POD disputes, multi-party claims, and RFA compliance?

- Dedicated account manager — Not a call centre. A named professional who knows your accounts.

- POPI compliance — Essential when sharing client data.

- Seamless legal escalation — When pre-legal collection fails, they should hand over directly to an approved attorney panel without you having to start the process again.

Kredcor meets all of these criteria. We are CFDC-registered (Reg Nr 0016365/06), and we operate across all of South Africa’s major commercial centres. We work on a strict No-Success-No-Fee basis — no upfront fees, no monthly fees, no hidden charges. And we have a 100% clean compliance record over 26 years.

11. What to Do Next: Your Action Plan

You have read the guide. Now act on it.

Here is the logical sequence of next steps, depending on where you are right now:

If you do not yet have signed credit applications from all clients:

Start immediately. Draft a credit application and T&Cs that include payment terms, interest on late payments, a credit-hold provision, and POPI consent. Implement it for all new clients today. For existing clients, request they sign at the next interaction.

If your invoicing process is batch-based (weekly or monthly):

Switch to immediate invoicing — within 24 hours of service completion. Set up an ePOD system if you have not already. These two changes alone will meaningfully reduce your debtor days within 30 to 60 days.

If you have overdue accounts older than 60 days with no payment commitment:

Pull your ageing analysis right now. Identify every account over 60 days with no signed payment plan. Those accounts need a formal letter of demand today — and handover to a registered collector within the next two weeks if there is no response.

Finally, when your internal efforts stall and your overdue book keeps growing, the right move is to partner with experienced debt collectors in South Africa who combine sector knowledge, legal compliance, and a genuine commitment to protecting your client relationships. That is exactly what Kredcor offers — and we do not cost you a cent unless we deliver results.

We also invite you to explore more expert, practical articles on credit management, debt recovery, and cash flow optimisation at www.kredcor.co.za/kredcor-articles/ — updated regularly and written specifically for South African business finance professionals.

Ready to Recover Your Outstanding Freight Invoices?

Kredcor operates on a strict No-Success-No-Fee basis. No upfront costs. No call centres. Just results — backed by 26 years of South African collections experience. Get a Free Consultation →

12. Quick-Action Checklist: Do These 5 Things Today

- Pull your accounts receivable ageing report right now — identify every logistics or freight invoice that is 60+ days overdue with no signed payment commitment in place.

- Confirm that your current terms and conditions are signed by every active credit client — and that they include a payment terms clause, interest on late payment, and your right to engage a debt collector.

- Set up — or review — your ePOD system to ensure every delivery generates a timestamped, digitally signed proof of delivery that is attached to the corresponding invoice.

- Verify the CFDC registration of any external debt collection agency you currently use or are considering at cfdc.org.za.

- Contact Kredcor (010 500 4640 | kredcor.co.za/contact) for a no-obligation consultation on your outstanding freight and logistics accounts.

Frequently Asked Questions: Logistics & Freight Debt Recovery

Q1: How long does a logistics or freight company have to collect an outstanding invoice before it prescribes in South Africa?

Under the Prescription Act 68 of 1969, most commercial debts — including logistics and freight invoices — prescribe three years after they fall due. Once that window closes, the debt becomes legally unenforceable. However, prescription can be interrupted by a partial payment from the debtor, a signed Acknowledgement of Debt (AOD), or the commencement of legal proceedings. Always act well before the three-year mark — ideally within 60 to 90 days of the due date.

Q2: What documents do I need to recover outstanding freight debt in South Africa?

At a minimum: a signed credit application or service agreement, original invoices with POD references, your signed terms and conditions, all relevant written communication with the debtor, and any AOD or payment plan documents. The stronger your documentation, the faster and more effectively a debt collector or attorney can act. An ePOD system provides court-admissible delivery evidence and eliminates most documentation disputes.

Q3: Can a freight or logistics company use a debt collector to recover outstanding transport fees?

Yes, absolutely. Freight and logistics companies can and should use a registered debt collector to recover outstanding transport fees, haulage invoices, freight forwarding fees, and related supply chain debts. The key requirement is that the collector must be registered with the Council for Debt Collectors (CFDC). Kredcor is CFDC-registered (Reg Nr 0016365/06), operates on a No-Success-No-Fee basis, and has extensive experience recovering commercial debt across the South African logistics and transport sector.

Q4: What is the biggest mistake logistics companies make when collecting outstanding freight debt?

The single biggest mistake is waiting too long before taking action. Kredcor’s internal data consistently shows that freight accounts handed over for professional collection within 60 to 90 days achieve recovery rates of 80 to 90 percent. Accounts left for six months or more see recovery rates drop below 40 percent — often dramatically lower. In the logistics sector, this delay worsens because companies continue to serve delinquent clients, allowing the outstanding balance to compound while the recovery window closes.

Disclaimer: This article is for general informational purposes only and does not constitute legal or financial advice. Consult a qualified attorney or registered debt collector for guidance specific to your circumstances.

Last updated: 6 May 2026 | Author: Kredcor Debt Recovery Team | Review cadence: Every 3–6 months, or when relevant legislation or industry conditions change. | Kredcor CFDC Reg Nr 0016365/06