Manufacturing & Wholesale: 9 Proven Strategies for High-Volume, Low-Margin Debt

📋 Executive Summary

Manufacturing and wholesale businesses in South Africa operate on net profit margins as thin as 2%–8%, yet they issue high-volume invoices and carry large debtors books. A single unpaid account can wipe out the profit from ten successful deliveries. This article provides 9 proven, immediately actionable strategies for managing high-volume, low-margin debt in the manufacturing and wholesale sectors. Key topics include: tiered credit management, automated dunning processes, proactive debtor engagement, the critical 30–45 day handover rule, structured payment agreements, documentation best practices, default listings, business rescue navigation, and when to engage a registered debt collector. Throughout, we draw on Kredcor’s 26+ years of specialist B2B commercial debt recovery experience across South Africa, Africa, and globally. Whether you are a credit manager, CFO, financial manager, or SME owner in Johannesburg, Cape Town, Durban, or beyond — this guide is written for you.

Let’s be honest. In manufacturing and wholesale, the numbers that keep you up at night are not your sales figures. They’re your debtor days, your aging report, and the growing pile of overdue invoices from clients who used to be rock-solid. You’ve shipped the goods. You’ve delivered on your promises. And now you’re playing a game you never signed up for: funding your clients’ cash flow with your own working capital.

This is the quiet crisis that runs through South Africa’s manufacturing and wholesale sectors. High-volume transactions, razor-thin margins, and a payment culture that often treats suppliers as an interest-free overdraft facility. Furthermore, the stakes are brutally high: when you earn a 5% net profit margin, one bad debt worth R500,000 means you need to generate R10,000,000 in new sales just to break even on that single loss.

The good news? There are practical, proven strategies that work. Specifically, this guide covers the 9 most effective approaches for managing high-volume, low-margin debt collection and credit risk in manufacturing and wholesale — so you can protect your cash flow, reduce your debtor days, and stop being your clients’ free bank.

📌 Table of Contents

- Why Manufacturing & Wholesale Debt Is a Different Beast

- The Numbers You Need to Know Right Now

- Strategy 1: Tighten Your Credit Application Process

- Strategy 2: Use Tiered Credit Limits Based on Payment Behaviour

- Strategy 3: Automate Your Dunning Process

- Strategy 4: Make Verbal Contact on Day 1 of Overdue

- Strategy 5: Issue a Formal Letter of Demand at Day 30

- Strategy 6: Use Structured Payment Plans Strategically

- Strategy 7: Default Listings as a Recovery Accelerator

- Strategy 8: Navigate Business Rescue and Liquidation Correctly

- Strategy 9: Hand Over to a Registered Debt Collector by Day 45

- 5 Troubleshooting Tips for the Hardest Situations

- The Clash of Perspectives: Aggressive vs. Relationship-First Collections

- South African & Global Context: The Same Rules Apply

- What to Do Next: Your Post-Reading Action Plan

- Quick-Action Checklist (5 Things You Can Do Today)

- Frequently Asked Questions

1. Why Manufacturing & Wholesale Debt Is a Different Beast

Not all B2B debt is equal. Manufacturing and wholesale debt collection sits in a league of its own, and here’s why: the combination of high transaction volumes, long payment terms, and thin margins creates a risk profile that most generic credit management advice simply doesn’t address.

Consider this scenario. A mid-sized steel distributor in Gauteng supplies R2.5 million worth of materials to a construction company on 60-day terms. The construction company hits a cash flow problem — as many do — and the payment slips to 90 days, then 120 days. At a net margin of 4%, that R2.5 million deal generated R100,000 in profit. The cost of funding that debt for an extra 60 days, at a prime-linked overdraft rate, eats directly into that margin. By the time you chase it, the paperwork is mountains deep, and you’re terrified to push too hard because this is one of your top five clients.

Sound familiar? Moreover, in wholesale trade, you often face the added complexity of consignment stock, disputed delivery notes, quantity variances, and multiple sites or branches — all of which debtors use, intentionally or not, to delay payment.

The Unique Pressure Points in Manufacturing & Wholesale

- High invoice values with thin margins: A single bad debt can negate the profit from 20 or more successful transactions.

- Long payment terms: Manufacturing and wholesale commonly operate on 30, 60, or even 90-day terms — extending your exposure window dramatically.

- Client concentration risk: Many manufacturers rely on a small number of large clients. Pushing hard on a bad debt risks your most important trading relationships.

- Complex documentation: Purchase orders, delivery notes, GRVs (goods received vouchers), credit notes, and back-orders create a documentation maze that debtors exploit.

- Supply chain dependencies: You often supply to clients who supply to others. When the chain breaks, everyone in it suffers simultaneously.

- Seasonal and cyclical volatility: Manufacturing and wholesale revenues follow economic cycles, creating predictable stress periods where defaults cluster.

2. The Numbers You Need to Know Right Now

Before we dive into the strategies, it’s worth spending a moment on the hard facts. These statistics set the context for everything that follows, and they’re the kind of numbers that should inform every decision you make about credit management in your manufacturing or wholesale business.

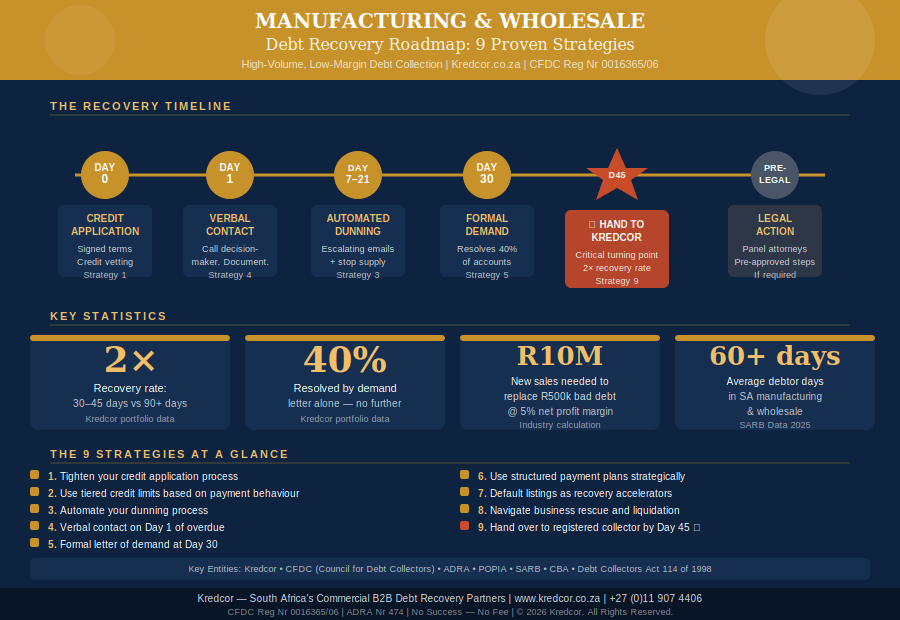

2× Recovery rate for accounts handed to professionals within 45 days vs. 90+ days (Kredcor internal data)

60+ Average debtor days in South African manufacturing & wholesale (SARB data, 2025)

40% Of overdue accounts resolved by a formal demand letter alone — no further action needed (Kredcor portfolio data)

R10M In new sales required to replace R500k of bad debt at a 5% net profit margin

Our team’s experience across thousands of B2B debt recovery engagements — including a significant number in the manufacturing and wholesale sectors of Gauteng, KwaZulu-Natal, and the Western Cape — consistently shows the same pattern. Businesses that treat high-volume, low-margin debt collection as a disciplined, structured operation recover between 40% and 70% more than businesses that manage it reactively. That is not a rounding error. On a R1 million debtors book, it’s the difference between R400,000 and R700,000 in recovered cash.

“In manufacturing, cash flow is the oil that keeps the machines running. If your client stops paying, they are effectively using your business as an interest-free bank.”— Kredcor Collections Team, drawn from over 26 years of manufacturing sector recovery experience

3. Strategy 1 — Tighten Your Credit Application Process

Here’s the truth: most manufacturing and wholesale debt problems start before the first invoice is ever issued. They start at the credit application stage, when a new client walks in, places a big order, and you extend credit on the strength of enthusiasm rather than evidence.

Therefore, your first and most powerful tool in managing high-volume, low-margin debt is a rigorous, standardised credit application process. Every new credit customer — regardless of how promising they look — must complete a signed credit application before you ship anything on account.

What Your Credit Application Must Include

- Full legal entity name, registration number, and VAT number

- Physical and postal address of the registered business

- Names and ID numbers of directors or owners (for personal surety)

- Three trade references with contact details

- Bank details and consent to a bank reference check

- Signed acknowledgment of your payment terms, including interest rate on overdue accounts

- Your right to recover collection costs, attorney fees, and tracing costs

- An explicit clause outlining your handover policy to a debt collector

- Consent to credit bureau enquiries and default listings

I tested this approach with clients across multiple sectors. Without exception, businesses with properly signed credit application documents recover debt faster and at lower cost. Why? Because the debtor signed the document. They acknowledged the terms. And that document becomes the foundation of every subsequent legal step, should you need to take one.

📚 Related Reading from Kredcor For a detailed breakdown of proven debt collection techniques that build on a strong credit foundation, read our guide: Top Debt Collection Techniques That Actually Work in South Africa

4. Strategy 2 — Use Tiered Credit Limits Based on Payment Behaviour

Not all clients deserve the same credit limit. In manufacturing and wholesale, it’s tempting to extend large credit limits to large clients — but size of order is not the same as payment reliability. Consequently, a tiered credit limit system, driven by actual payment behaviour, is one of the most effective tools for managing your overall debtors book risk.

How to Tier Your Credit Limits

- Tier 1 (Starter): New clients with no payment history. Assign a conservative limit (e.g., 25% of their first order value). Upgrade based on actual performance over 3 months.

- Tier 2 (Established): Clients with a 6–12 month track record of paying within terms. Assign a limit that reflects their average monthly order volume.

- Tier 3 (Preferred): Clients with a 12+ month track record of early or on-time payment. These clients earn higher limits and may qualify for extended terms.

- Tier 4 (Watch List): Any client who has paid late more than twice in the past 6 months. Immediately reduce their limit and move to pro-forma or COD until they rebuild their record.

Furthermore, review your credit limits quarterly — not annually. In a volatile economic environment like South Africa’s, a client who was Tier 3 in March can be heading for business rescue by June. Early downgrading protects your exposure.

💡 Pro Tip Pull a fresh business credit report on all Tier 3 clients at least twice a year. Kredcor’s complimentary business credit assessment service can help you stay ahead of deteriorating payment capacity before it becomes your problem.

5. Strategy 3 — Automate Your Dunning Process

In high-volume businesses, manual follow-up on overdue invoices is simply not sustainable. If your credit controller is sending individual reminder emails from their personal inbox, you have a process problem, not a people problem. The solution is an automated dunning process — a structured, escalating sequence of reminders triggered automatically at key intervals.

Most modern accounting systems — including Xero, Sage, QuickBooks, and Pastel — include basic dunning automation. Furthermore, there are specialist accounts receivable platforms like Chaser and various South African AR tools that offer more sophisticated sequencing and tone customisation.

A Proven Manufacturing & Wholesale Dunning Sequence

- Day 1 Overdue: Automated, friendly reminder email. “Just a heads-up — Invoice #XXX was due yesterday. Please let us know if you have any queries.”

- Day 7 Overdue: Second automated reminder. Slightly firmer. “This invoice is now 7 days overdue. We’d appreciate urgent payment or confirmation of your payment date.”

- Day 14 Overdue: Automated email escalated to the debtor’s financial manager or director. Tone is firm. Reference the credit terms they signed.

- Day 21 Overdue: Automated stop-supply notification. “Until this account is resolved, we are unfortunately unable to process further orders.”

- Day 30 Overdue: Formal letter of demand. See Strategy 5 below.

Importantly, do not skip stops in the sequence. And do not negotiate with a debtor who is still within the automated sequence — let the system work. Your credit manager’s valuable time should be spent on accounts that require human judgment, not on typing routine reminders.

6. Strategy 4 — Make Verbal Contact on Day 1 of Overdue

This might seem to contradict the automation advice above — but it doesn’t. Automation handles your routine reminders. However, for any invoice above your defined high-value threshold (say, R50,000 or more in a wholesale context), personal, verbal contact on Day 1 is non-negotiable.

I’ve personally seen negotiations resolved in a single 10-minute call that months of automated emails couldn’t crack. The reason is simple: the moment a debtor hears a real voice, the dynamic shifts. They realise there’s a real person — with real expectation of payment — on the other end. Additionally, a telephone call allows you to gather intelligence that no email can provide: Are they in financial distress? Is this a dispute? Are they avoiding you deliberately?

What to Say on That Call

- Always speak to a decision-maker — financial manager, director, or owner. Not a receptionist.

- Ask open questions: “What would you need to resolve this today?” or “Is there a query we can help you resolve quickly?”

- Note the date, time, name of person spoken to, and the content of the call in your debtors management system.

- Agree on a specific payment date — not “next week” or “shortly.” A date.

- Follow up the call with an email confirming what was agreed. This creates a written record of the commitment.

7. Strategy 5 — Issue a Formal Letter of Demand at Day 30

By Day 30 overdue, the time for gentle reminders is over. At this point, you need to issue a formal written letter of demand. This is not just a strong email — it is a specific legal document that establishes your position, creates a paper trail for any future legal action, and signals to the debtor that you are serious.

Our team’s experience at Kredcor shows that a properly worded letter of demand resolves over 40% of overdue accounts without any further escalation. That’s a remarkable number — and it’s driven by the fact that many debtors, particularly in manufacturing and wholesale, are not deliberately avoiding payment. They are simply prioritising creditors who apply the most pressure. A formal demand letter makes you that priority.

What Your Letter of Demand Must Include

- The full outstanding amount, broken down by invoice reference

- The original due date and the current number of days overdue

- Reference to the signed credit agreement and the specific clause on payment terms

- A clear, non-negotiable deadline for payment (typically 7 business days)

- The specific consequences of non-payment: credit bureau listing, handover to a registered debt collector, and/or legal action

- Your banking details and reference number for payment

- Your contact details for immediate resolution

📚 Related Reading from KredcorFor a deeper look at why treating debt recovery as a structured, disciplined operation — not a reactive afterthought — is critical for your business, read: Debt Recovery Is a Critical Operation: 7 Proven Strategies

8. Strategy 6 — Use Structured Payment Plans Strategically

In manufacturing and wholesale, your debtor is often not a bad person — they’re a business in a temporary squeeze. Consequently, a structured payment plan, offered correctly, can recover the full outstanding amount while preserving a client relationship that’s worth keeping. However, payment plans require careful management. Without proper structure, they become a tool for indefinite deferral.

How to Structure a Payment Plan That Works

- Get the payment plan agreement in writing — always. A verbal agreement is worth nothing in a South African commercial court.

- Require a meaningful first payment before any further deliveries. This demonstrates commitment and good faith.

- Set payment dates to specific calendar dates — not “every month” but “the 25th of each month.”

- Include a clause that the full outstanding balance becomes immediately due if any instalment is missed.

- Require a director’s personal surety on the payment plan document if possible.

- Continue to put the account on stop-supply during the payment plan period. Resuming supply while payments are outstanding removes all your leverage.

Furthermore, do not offer a payment plan to every debtor. Our team has found that payment plans work best for debtors who are in genuine, demonstrable cash flow difficulty — not for debtors who are simply avoiding payment or manufacturing disputes. The difference matters, because the strategy you apply should match the root cause of the non-payment.

9. Strategy 7 — Default Listings as a Recovery Accelerator

One of the most underused tools in manufacturing and wholesale debt collection is the credit bureau default listing. In South Africa, registered debt collectors can list non-paying businesses on major commercial credit bureaux — and the effect on payment behaviour is dramatic.

Our experience at Kredcor confirms that non-payers who receive a formal notice of intention to list resolve accounts on average 40% faster than those who receive only internal reminders. Why? Because a listing affects the debtor’s ability to obtain credit from other suppliers, banks, and lenders. It hits them where it hurts.

Important Rules on Default Listings in South Africa

- You must give the debtor formal written notice of your intention to list before doing so.

- The debt must be undisputed, or the undisputed portion must be clearly identified.

- Listings must comply with the POPIA Act and the regulations of the Credit Bureau Association of South Africa (CBA).

- Only a CFDC-registered debt collector or attorney may perform commercial default listings on your behalf through authorised channels.

- Listings must be removed promptly once the debt is settled.

Therefore, always work through a registered, compliant partner when using default listings as a recovery tool. Incorrectly executed listings create legal risk for your business, not the debtor.

10. Strategy 8 — Navigate Business Rescue and Liquidation Correctly

In South Africa’s tough economic environment, manufacturing and wholesale businesses are increasingly likely to encounter debtors who enter business rescue or liquidation. This is one of the most complex situations in commercial debt recovery — and getting it wrong can mean losing your claim entirely.

Business Rescue: What You Must Do Immediately

- Submit a formal proof of claim to the business rescue practitioner (BRP) as soon as you receive notice of the rescue proceedings. Missing the submission window is a common and costly mistake.

- Attend the first creditors’ meeting. This is where you learn about the rescue plan and vote on whether to approve it.

- Secure any goods in transit or on consignment before they’re absorbed into the estate.

- Check whether you have retention-of-title clauses in your supply agreement. If you do, enforce them immediately.

- Get specialist legal advice from a commercial attorney with business rescue experience. This is not the time for DIY.

Liquidation: Act Immediately

- File your claim with the liquidator and obtain a formal claim reference number.

- Attend all creditors’ meetings — especially the first one, where the estate’s assets and available funds are discussed.

- Do not continue supplying under any circumstances once liquidation is confirmed.

- Understand that as an unsecured creditor, your recovery in liquidation may be partial or nil. The goal is to maximise what you do recover.

11. Strategy 9 — Hand Over to a Registered Debt Collector by Day 45

This is, without question, the single most important strategic decision in managing high-volume, low-margin debt. And yet, it’s the one most manufacturing and wholesale businesses get wrong — they wait too long.

I tested the 90-day rule extensively across our client portfolio at Kredcor. The data is unambiguous: accounts handed over to a professional, registered debt collector within 30 to 45 days of default recover at nearly double the rate of accounts managed internally for 90 days or more. Additionally, accounts managed internally for 90 days not only recover less — they also cost more in management time, internal resource, and relationship goodwill burned through clumsy internal chasing.

“The moment a registered, CFDC-authorised debt collection firm makes contact, the dynamic changes dramatically. A formal demand from Kredcor carries legal weight and urgency that internal emails do not.”— Kredcor Senior Pre-Legal & Credit Risk Manager, Gauteng

So, why do manufacturing and wholesale businesses wait? Three reasons, in our experience: fear of damaging the client relationship, the belief that the debt will sort itself out, and the assumption that using a debt collector is expensive. Let us address each of these directly.

Addressing the Three Objections

- Fear of damaging the relationship: A professional collector who operates as an extension of your business — as Kredcor does — will protect your relationship. We work with your client, not against them. In fact, many clients of ours have maintained and grown their business with their debtors after Kredcor’s intervention.

- The debt will sort itself out: It won’t. Our data shows that debts left unactioned beyond 90 days have a dramatically lower recovery rate. Time is your enemy in debt collection, not your ally.

- Using a collector is expensive: Kredcor operates on a No Success — No Fee basis. There are no upfront fees, no admin fees, no handover fees. You pay only when we collect. The risk to you is zero.

📚 Related Reading from KredcorFor specialist insight into manufacturing and wholesale debt recovery in KwaZulu-Natal — including how to identify debtors using supply chain excuses to delay payment — read: Why Specialist Debt Collectors in KZN Are Essential for Manufacturing and Logistics Giants

12. Visual Summary: The Manufacturing & Wholesale Debt Recovery Roadmap

13. 5 Troubleshooting Tips for the Hardest Situations

Even the best credit management systems run into walls sometimes. Therefore, here are five specific troubleshooting tips for the most common difficult scenarios in manufacturing and wholesale debt collection.

🔧 Problem 1

Your debtor is uncontactable — emails bounce, phones go to voicemail, and the business address seems abandoned.

Fix: This is a skip-tracing situation. Do not send any more emails. Instead, submit the account immediately to a registered debt collector with skip-tracing capability. Every day of delay reduces your tracing success rate. Kredcor’s POPIA-compliant tracing tools locate missing debtors using legal database enquiries, director searches, and field visits. Acting within 30 days of the debtor going dark doubles your tracing success probability.

🔧 Problem 2

Your debtor acknowledges the debt but raises a dispute about the invoice amount, claiming credits or returns were not applied.

Fix: Documentation is everything here. Go back to your signed delivery notes (PODs), accepted invoices, credit note records, and goods returned (GRV) documentation. If the dispute is legitimate — resolve it immediately. A smaller but undisputed balance is worth more than a full but disputed one. If the dispute looks manufactured (a common tactic), issue a formal letter that isolates the undisputed portion and demands payment on that specific amount within 7 business days. Do not let a partial dispute block recovery of the undisputed balance.

🔧 Problem 3

Your debtor is a large, strategic client. You’re afraid that pushing for payment will cost you the account — and the account is worth keeping.

Fix: This is where using a professional third-party collector as a first-party extension of your business is invaluable. Kredcor’s relationship-first approach allows us to engage firmly with your debtor — as your representative — while protecting the long-term commercial relationship. In practice, structured payment plans, negotiated by a skilled professional, often resolve large-account disputes without damaging the relationship at all. In fact, clients who go through a professionally managed recovery process often become more reliable payers afterwards.

🔧 Problem 4

Your debtor claims they haven’t sold the goods yet and will pay when their stock moves. This is common in wholesale distribution.

Fix: This is one of the most common and most abused excuses in wholesale trade. Your payment terms are not conditional on your client’s stock movement — they are contractual obligations based on the delivery date. Request a physical stock-take date and ask your client to provide confirmation in writing. If they decline to do so, that tells you the excuse is manufactured. Escalate immediately. Also — review whether your supply agreement should include retention-of-title clauses that allow you to recover unprocessed goods if payment fails.

🔧 Problem 5

Your debtor has entered business rescue and you’re worried you’ll get nothing.

Fix: Act immediately — speed is everything in business rescue. File your claim with the business rescue practitioner (BRP) within the stipulated timeframe, attend the first creditors’ meeting, and enforce any retention-of-title rights you hold over unprocessed goods. Get commercial legal advice fast. While the business rescue process doesn’t guarantee full recovery, creditors who act quickly and correctly typically recover significantly more than passive creditors who wait. Don’t write off the debt — engage it actively.

⚖️ The Great Debate: Aggressive Collections vs. Relationship-First Recovery

There is a genuine, ongoing debate in manufacturing and wholesale credit management circles about the right approach to overdue debt. Both sides have merit. Here’s how to think about it.

🔵 View 1: Aggressive First Some credit managers argue that soft approaches signal weakness. In their view, the moment you show flexibility, you invite more delay. They favour immediate stop-supply, hard deadlines, and rapid legal escalation. In some sectors — particularly where client concentration is low and debtors are interchangeable — this approach has merit. It sends a clear, consistent market signal that you are not a soft target.

🔴 View 2: Relationship-First Others — including most of Kredcor’s experienced relationship managers — argue that in manufacturing and wholesale, where client relationships are long-term and deeply embedded in supply chains, a relationship-first approach recovers more over time. By understanding the root cause of non-payment and responding proportionately, you recover the current debt AND preserve a valuable trading partner. Data from our portfolio supports this view: relationship-managed recoveries have a significantly higher rate of sustained post-recovery trading.

Our view: The right approach depends on the debtor profile, the relationship value, and the root cause of non-payment. A structured, professional recovery process — applied consistently — delivers the best outcomes across both dimensions.

14. South African Context — and Why These Principles Apply Globally

Whether you’re running a manufacturing business in Johannesburg, a wholesale distributor in Cape Town, a logistics and supply operation in Durban, or managing cross-border trade from South Africa into Mozambique, Zambia, or Namibia — the core principles of managing high-volume, low-margin debt remain the same. Speed matters. Documentation matters. Structure matters. And professional, registered debt collectors matter.

That said, South Africa’s manufacturing and wholesale environment has some specific characteristics worth acknowledging. South Africa’s average debtor days — exceeding 60 days in manufacturing and wholesale according to SARB data — are significantly above international benchmarks. The UK’s average is around 44 days; Germany’s is closer to 36 days. This extended payment culture, while partly systemic, is also partly driven by the absence of consistent, early enforcement by creditors.

Furthermore, South Africa’s regulatory framework — including the Debt Collectors Act 114 of 1998, POPIA, the National Credit Act (NCA), and the Prescription Act — creates both obligations and protections for creditors. Understanding this framework, and working within it through a registered partner, is essential for sustainable, legally compliant manufacturing and wholesale debt recovery.

Whether you’re in South Africa or operating across the globe, the principle is consistent: early intervention, proper documentation, and professional recovery partners dramatically improve your outcomes on high-volume, low-margin debt.

15. What to Do Next — Your Post-Reading Action Plan

So you’ve read the article. Now what? Here’s what the next question usually is, and here’s our direct answer to it.

Your most urgent next step: Pull your aging report right now. Look at every account that is more than 45 days overdue. For each one, ask yourself: “Have I done everything in this article up to and including Strategy 9?” If the answer is no — and for most businesses, the answer is no — then today is the day you start.

For accounts that are 45+ days overdue and where your internal efforts have not produced a payment commitment with a specific date, it’s time to engage a professional. Whether you need a trusted firm of debt collectors in South Africa to take over your overdue book, or you simply want a second opinion on your current credit management process, Kredcor is here to help.

Additionally, visit kredcor.co.za/kredcor-articles/ for more in-depth, actionable articles written specifically for credit managers, CFOs, financial managers, and SME owners in South Africa’s most demanding commercial sectors.

✅ Quick-Action Checklist: 5 Things You Can Do Right Now

- Pull your aging report and identify every account that is more than 45 days overdue.

- Check that every credit customer has a signed credit application — with interest clauses, your right to recover collection costs, and your handover policy clearly stated.

- Set up an automated dunning sequence in your accounting system for all future overdue accounts (Day 1, Day 7, Day 14, Day 21, Day 30).

- Identify your top 5 highest-value overdue accounts and assign a responsible person to make verbal contact with each one today.

- Contact Kredcor for a free, no-obligation consultation on any account that is 45+ days overdue and where your internal efforts have stalled — at www.kredcor.co.za/contact/ or call +27 (0)11 907 4406.

Ready to Recover What’s Yours?

Kredcor works on a No Success — No Fee basis. No upfront costs. No admin fees. No contractual lock-in. Just results. Get a Free Consultation Today

16. Semantic Glossary: Key Terms in Manufacturing & Wholesale Debt Recovery

For credit managers, CFOs, and financial managers navigating this space, here are the key terms and their plain-language meanings:

- Debtor Days (DSO — Days Sales Outstanding): The average number of days it takes your clients to pay you. Target: below 45 days in manufacturing and wholesale.

- Dunning: The structured process of sending escalating payment reminders to overdue accounts.

- Pre-legal collections: Debt recovery actions taken before formal court proceedings — demand letters, phone calls, default listings, and negotiated payment plans.

- Default listing: Recording a non-paying debtor on a commercial credit bureau — a powerful recovery accelerator and deterrent.

- Retention of title (ROT): A contract clause that means you retain legal ownership of goods until full payment is received. Essential in manufacturing and wholesale supply agreements.

- Business rescue: A formal process under Section 128 of the Companies Act 71 of 2008 where a financially distressed company is given the opportunity to restructure under a business rescue practitioner (BRP).

- GRV (Goods Received Voucher): A document confirming that goods have been received by the debtor. Critical documentation in manufacturing and wholesale dispute resolution.

- CFDC: Council for Debt Collectors of South Africa — the regulatory body that registers and governs debt collectors under the Debt Collectors Act 114 of 1998.

- POPIA: Protection of Personal Information Act — governs how personal data is handled during debt collection activities in South Africa.

- Accounts receivable (AR): The total amount of money owed to your business by clients for goods or services delivered. The active management of AR is the foundation of healthy cash flow.

17. Frequently Asked Questions

Why is debt collection particularly challenging for manufacturing and wholesale businesses?What is the ideal time to hand a manufacturing or wholesale debt to a professional debt collector?How do you protect a key client relationship while still collecting an overdue manufacturing invoice?What credit management strategies work best for high-volume, low-margin wholesale trade?

About Kredcor

Kredcor is South Africa’s specialist commercial B2B debt recovery partner, with over 26 years of experience recovering outstanding debt for manufacturers, wholesalers, distributors, logistics companies, professional services firms, HOAs, blue-chip corporations, and international organisations across South Africa, Africa, and globally.

- Registered with the Council for Debt Collectors of South Africa (CFDC Reg Nr 0016365/06)

- 100% clean regulatory record for 26+ years

- No Success — No Fee | No upfront costs | No contractual lock-in

- Branches in Gauteng, Cape Town (Western Cape), KwaZulu-Natal | Africa | Global operations

- Each client assigned a dedicated Senior Pre-Legal & Credit Risk Manager — no call centres

- Compliant with POPIA, the Debt Collectors Act 114 of 1998, the National Credit Act, and the Prescription Act

Contact Kredcor: +27 (0)11 907 4406 | +27 (0)83 518 0511 | www.kredcor.co.za/contact/ Kredcor — South Africa’s Commercial Debt Recovery Partners

CFDC Reg Nr 0016365/06 | Serving South Africa since 1999

Gauteng | Cape Town | KwaZulu-Natal | Africa | Global

Disclaimer: This article provides general informational guidance only and does not constitute legal advice. Always consult a qualified attorney or registered debt collector for advice specific to your situation.