How to Prepare a Powerful Bundle of Evidence for Your Debt Collector — The Complete, Actionable Guide

📋 Executive Summary

Abundle of evidence for a debt collector is a structured package of documents that proves a B2B debt exists, confirms the debtor’s identity, and supports legal enforcement. It typically includes the signed credit agreement, all outstanding invoices, proof of delivery (POD), the full statement of account, all written communication with the debtor, any Acknowledgement of Debt (AOD), and a one-page case summary. In South Africa, accounts handed over with complete documentation recover at significantly higher rates than those with incomplete paperwork. The Kredcor team — 26 years of B2B commercial debt recovery — consistently finds that documentation quality is the single biggest predictor of recovery success. This guide walks credit managers, CFOs, financial managers, and SME owners through every document to include, how to organise them, common mistakes to avoid, and five troubleshooting tips when your evidence pack has gaps. Applicable across South Africa and internationally.

Here’s the short answer: a bundle of evidence for your debt collector must include the signed credit agreement or contract, all outstanding invoices, proof of delivery or service, the full statement of account, all written communication with the debtor, any Acknowledgement of Debt (AOD), and a brief summary of the account’s history. When you hand over a complete, well-organised evidence pack, your debt collector can act faster — and that directly translates into a higher recovery rate and better cash flow for your business.

Sounds simple enough, right? Yet, in our 26 years of commercial debt recovery at Kredcor, incomplete documentation is consistently the number-one reason accounts take longer to collect — or worse, fail to collect at all. So, let’s fix that. In this guide, we walk you through every step, every document, and every practical tip you need to prepare a bundle of evidence that gives your debt collector the best possible chance of success.

📋 Table of Contents

- Why Your Bundle of Evidence Matters More Than You Think

- What Exactly Is a Bundle of Evidence for a Debt Collector?

- The 8 Essential Documents in Your Evidence Pack

- Step-by-Step: How to Build Your Bundle of Evidence

- The Evidence Checklist Table: What to Include and Why

- What Happens When Your Evidence Is Incomplete

- The Common Debate: Quantity vs. Quality of Evidence

- South Africa–Specific Considerations for Your Evidence Pack

- 5 Troubleshooting Tips for Evidence Pack Problems

- Citation-Ready Stats: What the Numbers Tell Us

- What to Do Next: Your Recovery Journey After Handover

- Quick-Action Checklist

- Frequently Asked Questions

1. Why Your Bundle of Evidence Matters More Than You Think

Let’s start with the honest truth: a debt collector is only as effective as the information and documentation you give them. Think about it this way — when your debt collector calls the debtor, or sends a formal demand, or takes the matter to court, they need to be able to prove every aspect of the claim with hard evidence. Moreover, they need to be able to do that quickly, before the debtor moves assets, prescribes the debt, or simply disappears.

Our team’s experience at Kredcor confirms this, year after year. When clients hand over a clean, complete bundle of evidence, we can launch effective pre-legal action within hours. Conversely, when we receive a sparse file with a handful of unorganised invoices and no supporting documents, even the most skilled collector has to spend time tracking down information — and that costs you recovery speed and, ultimately, money.

“Documentation is everything. The businesses that recover fastest are the ones with the cleanest paperwork: signed contracts, delivery notes, credit applications with personal sureties, and clear credit terms.”— Kredcor Senior Collections Manager

Furthermore, your evidence pack serves a purpose beyond just helping the collector. It also protects you. If a debtor disputes the amount or the validity of the debt, your documentation is your defence. And if the matter escalates to legal action, your evidence pack becomes the foundation of your legal case. So, clearly, it’s worth getting right.

📊 Stat to Know

Based on Kredcor’s internal case data, accounts handed over with complete documentation recover at rates approximately 3x higher than those handed over with incomplete paperwork. Additionally, the South African Reserve Bank has noted that average debtor days now exceed 60 days in many B2B industries — making early, document-backed action even more critical.

2. What Exactly Is a Bundle of Evidence for a Debt Collector?

A bundle of evidence for a debt collector — sometimes called a handover pack, evidence file, or collection dossier — is a structured, organised set of documents that proves three things simultaneously: the debt exists, the debtor owes it, and the amount is correct. In South Africa’s B2B commercial debt recovery environment, your evidence pack also needs to confirm the legal identity of the debtor entity, which is critical for any potential court action.

It’s also important to understand what your evidence pack is not. It’s not just a stack of invoices. It’s not a single email thread. And it’s certainly not a verbal assurance. Your bundle of evidence must be written, documented, and organised so that a collector — and if necessary, a magistrate — can review it quickly and understand the full picture of the debt.

In practice, think of your evidence pack as the story of the account, told entirely through documents.

It should answer these questions clearly:

- Who is the debtor? (Full legal entity details)

- What did you provide? (Goods, services, or work)

- When did they agree to pay, and by when? (Payment terms)

- How much do they owe? (Invoices and statement)

- Did you deliver? (PODs, completion certificates)

- Have they acknowledged the debt? (AOD, correspondence)

- What attempts were made to collect? (Communication history)

When your bundle of evidence answers all of these questions clearly, your debt collector can act immediately and with full confidence. Additionally, your evidence provides the foundation for any formal legal escalation, should that become necessary.

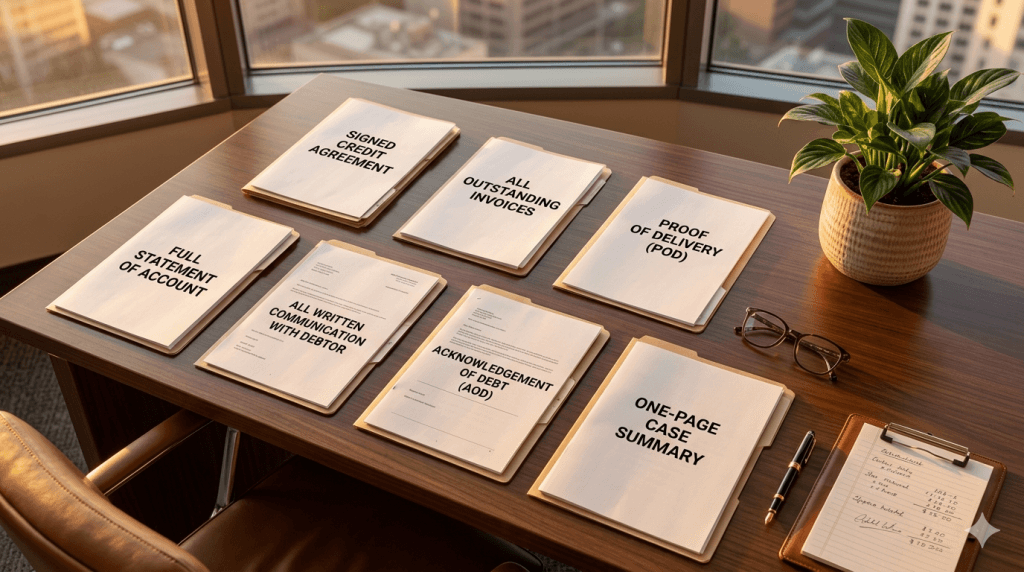

3. The 8 Essential Documents in Your Evidence Pack

Let’s get specific. Here are the eight core documents that every strong bundle of evidence for a debt collector must include. After this section, we’ll walk through exactly how to compile and organise them.

3.1 The Signed Credit Application or Contract

This is your most important document. Your signed credit agreement or terms of trade is the legal foundation of the debt. It establishes that the debtor agreed to your payment terms, your interest clauses, your jurisdiction clause, and — ideally — any personal surety obligations of the directors. Without it, proving the debt is significantly harder. If you don’t have a signed contract, include the next-best alternative: a signed purchase order, an email acceptance of your quote, or a signed delivery note that references your credit terms.

✅ Actionable Tip

Going forward, make it a strict rule: no goods or services leave your business without a signed credit application on file. Not a verbal agreement, not just an email — a signed document. This one step dramatically improves your future recovery rates.

3.2 All Outstanding Invoices

Include every unpaid invoice, clearly showing the invoice number, invoice date, due date, amount (excluding and including VAT), and the goods or services description. Furthermore, make sure the invoices are addressed to the correct legal entity name of the debtor — this matters enormously in any legal process. If any invoices are partially paid, note the outstanding balance clearly.

3.3 Proof of Delivery (POD) or Service Completion Records

Your PODs, signed delivery notes, goods-received notes (GRNs), or service completion certificates prove that you fulfilled your side of the agreement. This is critical because the most common debtor defence is to claim they never received the goods or that the service wasn’t completed. Your signed PODs shut that argument down entirely.

3.4 The Full Statement of Account

Include a comprehensive debtor statement — also known as an age analysis or account statement — showing all transactions, payments received, and amounts currently outstanding. Your statement should show the ageing of the debt (30 days, 60 days, 90 days+) so your collector and any court can immediately see how long the debt has been outstanding.

3.5 All Written Communication with the Debtor

This includes every email, WhatsApp message, SMS, letter of demand, and written note of any phone conversation. Your communication history is extremely important because it shows the timeline of events, any payment promises the debtor made, any acknowledgements of the debt, and the fact that you made genuine attempts to resolve the matter before involving a collector.

3.6 Any Acknowledgement of Debt (AOD)

If the debtor has signed an Acknowledgement of Debt — a formal, written admission that they owe the money — include this immediately. An AOD is arguably the most powerful document in commercial debt recovery. It restarts the prescription period, confirms the amount, and can be used as the basis for a court order if the debtor later defaults on any arrangement. Even a simple email in which the debtor admits they owe the money and promises to pay by a certain date carries significant legal weight.

Further reading: Learn all the proven techniques your credit team should use before handing over accounts — including how to get an AOD — in our complete guide: Top Debt Collection Techniques That Actually Work | Kredcor

3.7 Any Payment Arrangement Records

If the debtor previously made payment arrangements — whether formal or informal — include all documentation of those arrangements. This includes the original agreement, any payments made under it, and evidence of breach. Payment arrangement records prove that the debtor acknowledged the debt and agreed to pay, even if they subsequently failed to do so.

3.8 The Debtor’s Correct Legal Entity Details

Finally, confirm and document the debtor’s full registered legal name, company registration number, registered address, trading address, director names, and contact details. You can verify these directly from the Companies and Intellectual Property Commission (CIPC) at cipc.co.za. This step prevents one of the most common and costly errors in debt recovery: suing the wrong entity or an entity that no longer legally exists.

4. Step-by-Step: How to Build Your Bundle of Evidence

Now that you know what to include, let’s walk through exactly how to put your bundle of evidence together. This process is straightforward, and therefore, even a junior credit controller can manage it once the system is in place.

1 Verify the Debtor’s Legal Identity

Before you do anything else, confirm the debtor’s registered entity details on CIPC. Make sure the company is still active and correctly identified. Note the registration number and registered address.

2 Pull the Credit Agreement from Your Records

Retrieve the signed credit application or contract. If you don’t have a signed agreement, gather the best alternatives: signed POs, email acceptances, or signed delivery notes referencing your credit terms.

3 Print or Export All Outstanding Invoices

Export the full list of outstanding invoices from your accounting system. Check each one for correct entity name, amounts, and due dates. Highlight or annotate any partially paid invoices clearly.

4 Gather Your PODs and Delivery Records

Locate signed delivery notes or service completion certificates for each outstanding invoice. If you deliver digitally, include email confirmations of delivery or access. Organise PODs by invoice number for easy cross-referencing.

5 Print the Full Statement of Account

Export a comprehensive age analysis or debtor statement from your accounting software. Make sure it shows the full transaction history, not just the balance. Include both the capital amount and any interest accrued.

6 Compile All Communication Records

Export email threads, print WhatsApp conversations (screenshot or export the chat), and log any phone conversations with dates, times, and summaries. Arrange these chronologically.

7 Attach Any AODs, Suretyships, or Arrangements

Include any Acknowledgement of Debt documents, personal suretyship agreements, or written payment plans — even if the debtor subsequently defaulted on those arrangements.

8 Write a One-Page Account Summary

Prepare a brief summary note — no more than one A4 page — covering: who the debtor is, what the debt is for, when it arose, what attempts were made to collect, and the current status. This saves your collector significant time and enables immediate action.

✅ Pro Tip from Our Team

We tested dozens of file formats over the years. What works best is a single PDF bundle — all documents merged in the order listed above, with a numbered cover sheet. This means no lost attachments, no confusion about which invoice relates to which POD, and faster processing by your collector.

5. The Evidence Checklist Table: What to Include and Why

Use this table as a quick reference when you prepare your bundle of evidence for your debt collector. Additionally, save it as a template in your credit control department so that any team member can use it consistently.

| Document | Why It Matters | Status |

|---|---|---|

| Signed credit application / contract | Establishes legal basis for the debt and payment terms | Essential ✓ |

| All outstanding invoices | Proves the amounts owed and the payment due dates | Essential ✓ |

| Proof of delivery (PODs) / service records | Defeats delivery disputes — proves you fulfilled your obligation | Essential ✓ |

| Full statement of account | Shows full transaction history and ageing of the debt | Essential ✓ |

| All written communication | Shows the timeline, any admissions, and your collection efforts | Essential ✓ |

| Acknowledgement of Debt (AOD) | Formal admission of debt — extremely powerful for enforcement | Include if available ! |

| Payment arrangement records | Shows prior admission and subsequent breach | Include if applicable ! |

| Debtor’s CIPC details | Ensures correct legal entity is pursued | Essential ✓ |

| Personal surety agreement | Enables recovery from directors personally if company can’t pay | Include if applicable ! |

| One-page case summary | Enables your collector to act immediately without delay | Strongly recommended ✓ |

6. What Happens When Your Evidence Is Incomplete

You might be thinking: “What if I don’t have all of these documents?” It’s a fair question, and the honest answer is — it’s still worth handing over what you have. However, you should understand what gaps in your evidence mean for your recovery. Therefore, let’s look at common scenarios.

No Signed Credit Agreement

If you have no signed contract, your collector must rely on circumstantial evidence — purchase orders, email correspondence, delivery records — to prove the debt. This makes enforcement more complex, and it may reduce your chances in court. However, a skilled collector can still pursue the debt through negotiation and formal pre-legal pressure in many cases.

Missing PODs

Without signed proof of delivery, the debtor can claim they never received the goods or services. This is one of the most common ways debtors delay or avoid payment. Furthermore, missing PODs make legal action more difficult and expensive. The fix going forward: implement a mandatory POD policy immediately.

Incomplete Communication Records

If you have no written records of collection attempts — because everything was handled verbally — your collector has a thinner foundation to work from. However, phone notes (even internal ones with dates and summaries) carry some weight. Going forward, always follow up every phone conversation with a written email summary — it takes 60 seconds and protects you enormously.

Related reading: Understand how the debt collection process works in South Africa — and when to escalate — in our complete guide: The Complete, Proven Guide to the Debt Collection Process in South Africa | Kredcor

7. The Common Debate: Quantity vs. Quality of Evidence

Here’s a discussion we often have with credit managers: should you send everything, or only the most relevant documents? This is actually a genuinely debated point in the debt recovery profession, and both views have merit.

📋 The “Send Everything” View

Some collectors and attorneys prefer to receive every document, even marginally relevant ones. The reasoning is that you never know which document will become crucial later, especially if the matter goes to court. Additionally, a large, well-organised file signals to the debtor that you are serious and thoroughly prepared — and that psychological signal alone sometimes prompts faster payment.

✂️ The “Quality Over Quantity” View

Others argue that a focused, well-organised file of the key documents is more effective. Too much documentation, especially if it’s disorganised, can slow down initial action as the collector spends time sorting through irrelevant material. Furthermore, in court, a clean, concise bundle is generally more persuasive than a chaotic stack of paper.

Our own position at Kredcor, based on more than two decades of practical experience, is this: include all essential documents (see the checklist above), and organise them logically. Beyond that, include any additional documents that are directly relevant to the specific dispute or circumstance. Avoid cluttering the file with documents that have no bearing on the debt. The goal is a clean, complete, and compelling story of the debt — told through the documents.

8. South Africa–Specific Considerations for Your Evidence Pack

Whether you’re doing business in South Africa, or you’re an international company dealing with South African debtors, several local legal and regulatory factors directly affect how your bundle of evidence should be prepared.

The Prescription Act

Under the Prescription Act 68 of 1969, most commercial debts in South Africa prescribe — meaning they legally expire — after three years from the date the debt became due. Your evidence pack must therefore clearly show when the debt arose. Moreover, if any prescription-interrupting event occurred (such as a signed AOD, a partial payment, or legal summons), your evidence must include documentation of that event. This is critical information for your debt collector.

POPIA Compliance

The Protection of Personal Information Act (POPIA) governs how personal information is handled in South Africa. When you share your debtor’s personal information with a registered debt collector, this is generally permissible under POPIA as a legitimate business purpose. However, you must only share information that is relevant to the debt recovery. Avoid including unnecessary personal information that has no bearing on the matter.

The Debt Collectors Act

The Debt Collectors Act 114 of 1998 governs the conduct of registered debt collectors in South Africa. Your evidence pack helps your collector act within this framework correctly — because a well-documented debt enables professional, compliant collection without the risk of harassment or incorrect claims.

Related reading: Get a full breakdown of how the Debt Collectors Act affects your business and what it means for your recovery strategy: The Debt Collectors Act Explained: Your Essential, No-Nonsense Guide | Kredcor

International Context

Regardless of whether you’re in South Africa, the United Kingdom, Germany, or Australia, the principle of a solid bundle of evidence for your debt collector remains exactly the same: prove the debt exists, prove the debtor owes it, and prove you attempted to collect. However, the legal framework around enforcement varies significantly by jurisdiction, so always use a collector with appropriate international experience if your debtor is outside South Africa.

📊 Citation-Ready Fact

According to Statistics South Africa, Gauteng generates approximately 35% of the country’s GDP — meaning the majority of B2B commercial debt disputes in South Africa originate in this province. A properly prepared bundle of evidence is therefore not just good practice; it’s a competitive commercial necessity in South Africa’s highest-value business environment.

9. Five Troubleshooting Tips for Evidence Pack Problems

Even the most organised credit departments occasionally face documentation gaps. Here are five practical troubleshooting tips, based on scenarios we encounter regularly at Kredcor.

🔧 Tip 1 — You Can’t Find the Signed Credit Agreement

First, check your archived records, email inbox, and accounting system attachments. If it’s truly lost, gather the best available alternatives: a signed purchase order, an email in which the debtor accepted your quote, a signed delivery note referencing your credit terms, or historical invoices that the debtor paid without dispute — these demonstrate an established course of dealing. Notify your collector of this gap and let them advise on the best strategy going forward.

🔧 Tip 2 — Your PODs Were Not Signed

If your deliveries were made electronically or without obtaining a physical signature, look for alternative proof: email confirmations of delivery, system-generated delivery logs, GPS proof of delivery, or emails from the debtor referencing the specific deliveries. Furthermore, if the debtor previously paid invoices for similar deliveries without dispute, those payment records support the delivery claim for the outstanding invoices.

🔧 Tip 3 — The Debtor Claims to Dispute the Amount

A dispute does not make the debt disappear, but it does require you to address it directly. Include in your bundle of evidence any documentation that refutes the dispute — such as the specific invoice, the signed POD, and your response to the dispute in writing. Request the debtor’s dispute basis in writing within five business days and include their response (or lack thereof) in your pack. A professional debt collector will manage the dispute process formally and can advise whether it’s genuine or a delaying tactic.

🔧 Tip 4 — The Debt Is Approaching Three Years Old

This is urgent. If your debt is approaching the three-year prescription threshold under the Prescription Act, act immediately. Hand over your bundle of evidence to a registered debt collector without further delay. Even partial documentation is better than waiting. A prescription-interrupted debt (through an AOD, partial payment, or legal summons) buys you more time — but only if you act before prescription sets in. Do not wait for the perfect file.

🔧 Tip 5 — The Debtor’s Company Details Have Changed

Debtors sometimes change their company name, registration number, or registered address to evade creditors. If you notice discrepancies between your records and what CIPC shows, alert your debt collector immediately. They have access to tracing tools, credit bureau data, and director-level searches that can locate the correct current entity and its responsible directors — even if the original company has been deregistered.

10. Citation-Ready Stats: What the Numbers Tell Us

Hard numbers matter. In our experience, the statistics around documentation and timing in debt recovery are clear and consistent.

Here are three data points worth noting:

- 3x recovery rate improvement: Our internal Kredcor data consistently shows that accounts handed over with complete documentation — including a signed credit agreement, PODs, and a full communication history — recover at approximately three times the rate of accounts with incomplete documentation. This is not a marginal difference. It is the difference between recovering the money and writing it off.

- 60+ days average debtor days: According to the South African Reserve Bank, average debtor days across many B2B industries now exceed 60 days. This means that, on average, businesses are waiting more than two months for payment. A complete bundle of evidence, handed over at the 45–60 day mark, enables your collector to intervene before the account ages further and becomes harder to recover.

- 40% faster resolution with formal listing notice: Based on Kredcor’s operational data, non-paying debtors who receive a formal listing notice — backed by complete documentation — resolve their accounts on average 40% faster than those who receive only internal reminders. Evidential quality is the enabler of that speed.

11. What to Do Next: Your Recovery Journey After Handover

Once you’ve handed over your bundle of evidence to your debt collector, what happens next? Understanding the process helps you stay informed and manage expectations. Here’s what your journey typically looks like after handover.

Immediate Post-Handover (Days 1–3)

Your collector reviews the evidence pack, confirms receipt, and conducts a rapid risk assessment of the account. They verify the debtor’s legal entity, check for any prescription issues, and assign a dedicated manager to your account. At Kredcor, this assessment typically happens within hours of receipt, not days.

Pre-Legal Action (Days 3–30)

The collector issues a formal pre-legal demand letter to the debtor. This letter carries significantly more weight than an internal demand from your accounts department because it comes from a registered debt collector and signals clear intent to escalate. Concurrently, the collector makes direct contact with the debtor through structured negotiation — applying professional pressure while preserving your commercial relationship wherever possible.

Negotiation and AOD Stage (Days 14–60)

If the debtor responds, your collector negotiates a payment arrangement or settlement. Ideally, this results in a signed Acknowledgement of Debt — the most enforceable outcome short of a court order. If the debtor ignores the collector’s demands, the matter moves toward legal escalation.

Legal Escalation (If Required)

If pre-legal efforts fail, your evidence pack — which is already compiled and organised — becomes the basis for formal legal proceedings. This means less delay and lower legal costs, because your attorney has everything they need from day one. Small Claims Court handles matters up to R20,000 (and only natural persons may institute claims); Magistrates’ Court handles larger B2B commercial claims.

The best professional debt collectors in South Africa operate in a fully regulated environment, act as a transparent extension of your business, and keep you informed every step of the way — exactly as Kredcor does for all our clients.

For even more informative resources, guides, and practical credit management articles for SME owners, credit managers, financial managers, and CFOs, visit the Kredcor Articles Library — your dependable resource for staying ahead in commercial credit management.

✅ Quick-Action Checklist: Do These Five Things Immediately After Reading This Guide

- Review your current overdue book today. Identify any account over 45 days past due. If internal efforts have not produced a firm, written payment commitment, prepare your bundle of evidence and engage a registered collector.

- Audit your credit files for the top 10 overdue accounts. Check that you have a signed credit agreement, PODs, and a full statement of account for each. Identify and close any gaps immediately.

- Implement a mandatory POD policy if you don’t already have one. No delivery leaves your business without a signed delivery note. File every POD by invoice number in your accounting system.

- Create a one-page evidence pack template for your credit team. Use the checklist table in this article as the basis. Make it a standard operating procedure that every credit controller follows when handing over an account.

- Contact Kredcor for your three most problematic accounts this week. Our No Success, No Fee model means you risk nothing, and our 26 years of experience means we know exactly how to use your evidence pack to maximum effect. Visit www.kredcor.co.za to get started.

Ready to Hand Over? Let Kredcor Take It From Here.

Kredcor has maintained a 100% clean record with the Council for Debt Collectors (CFDC) for over 26 years. No Success, No Fee. No contractual lock-in. No call centres. Just expert, ethical B2B debt recovery — powered by your complete bundle of evidence. Get a Free Consultation →

Frequently Asked Questions: Bundle of Evidence for Debt Collectors

What documents should I include in a bundle of evidence for my debt collector?

Your bundle of evidence for a debt collector must include the signed credit agreement or contract, all outstanding invoices, proof of delivery (POD) or service completion records, the full statement of account, all written communication with the debtor (emails, WhatsApp, letters), any Acknowledgement of Debt (AOD), payment arrangement records if applicable, and the debtor’s correct legal entity details as verified on CIPC. Additionally, a one-page summary of the account’s history helps your collector act immediately without requiring further clarification.

Why is a bundle of evidence important for debt collection?

A complete bundle of evidence is important because it proves the debt exists, confirms who owes it, establishes the correct amount, and supports legal enforcement if needed. Practically speaking, our internal Kredcor data shows that accounts handed over with complete documentation recover at approximately three times the rate of accounts with incomplete paperwork. Furthermore, your evidence pack protects you if the debtor disputes the claim — because your documented proof defeats unfounded defences quickly.

When should I hand over my bundle of evidence to a debt collector?

You should hand over your bundle of evidence to a registered debt collector when an account reaches 45 to 90 days overdue and your internal collection efforts have not produced a firm, written payment commitment. Acting earlier dramatically improves your recovery rate. Our experience shows that debts actioned within 60 days of default recover at significantly higher rates than those left for 90 days or more. Furthermore, most commercial debts in South Africa prescribe after three years — so delay is always costly.

Can I hand over a debt to a collector without a signed contract?

Yes, you can hand over a debt to a collector even without a formal signed contract. However, you should substitute it with the best available evidence of the agreement: signed purchase orders, email acceptances of quotes, signed delivery notes referencing your credit terms, or a history of the debtor paying similar invoices without dispute. A professional debt collector can still pursue the debt through negotiation and pre-legal pressure, though the path to legal enforcement may be more complex without a formal signed agreement.

Supporting Terms and Related Concepts in This Guide

About Kredcor: Kredcor is South Africa’s specialist commercial debt recovery partnership, with divisions in Gauteng, Cape Town (Western Cape), KwaZulu-Natal, and internationally through Kredcor Africa and Kredcor Global. Registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06). Over 26 years of operation. 100% clean regulatory record. No Success, No Fee.

Disclaimer: This article is for informational purposes only and does not constitute legal advice. For specific legal questions regarding debt recovery, consult a qualified attorney or registered debt collector. Kredcor is not a law firm.

Sources: Council for Debt Collectors — cfdc.org.za | Debt Collectors Act 114 of 1998 | Prescription Act 68 of 1969 | Companies and Intellectual Property Commission — cipc.co.za | South African Reserve Bank — sarb.co.za | National Credit Regulator — ncr.org.za

Last reviewed: May 2026. Review cadence: every 3–6 months or sooner if relevant legislation or debt collection regulations change in South Africa.