What to Do When a Debtor Ignores Your Invoice — The Proven 7-Step Guide That Actually Gets You Paid

By Kredcor — Debt Collectors in South Africa’s | Registered with the Council for Debt Collectors (Reg Nr 0016365/06) | 26+ Years of B2B Debt Recovery Experience

⚡ The Short Answer:

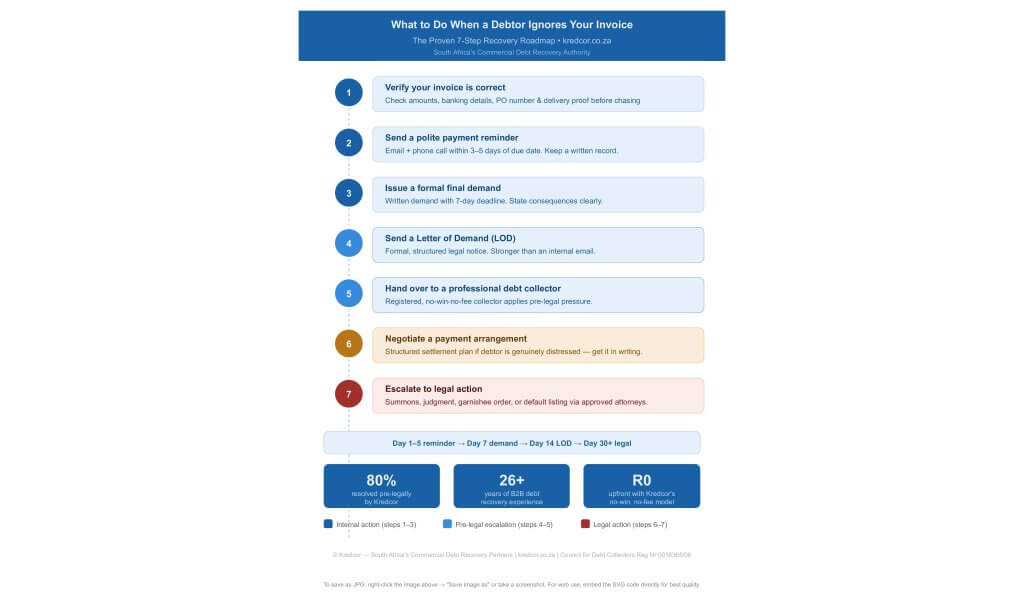

When a debtor ignores your invoice, act immediately and systematically:

(1) verify the invoice,

(2) send a polite reminder,

(3) issue a final demand,

(4) send a formal Letter of Demand,

(5) hand over to a registered debt collector,

(6) negotiate a payment arrangement if appropriate, and

(7) escalate to legal action.

The sooner you act, the higher your chance of recovery. Most B2B disputes are resolved at steps 1–4 — before legal costs are incurred.

You delivered the goods. You provided the service. You sent the invoice. And then — silence. The debtor ignores your invoice, dodges your calls, and your cash flow is quietly bleeding. If this sounds familiar, you’re far from alone. According to the South African Reserve Bank, late and non-payment of B2B invoices is one of the top three cash flow threats facing South African SMEs. In fact, research consistently shows that overdue debtor days cost South African businesses billions in lost working capital every year.

The good news? There’s a clear, proven, step-by-step process that — when followed correctly — dramatically improves your recovery rate and protects your business relationships at the same time. Furthermore, you don’t need to handle it alone. At Kredcor, our team has been doing this for over 26 years, and we’ve seen first-hand what works and what doesn’t.

In this guide, we walk you through exactly what to do — step by step — when a debtor ignores your invoice. Whether you’re an SME owner, a credit manager, a financial manager, or a CFO, this is your actionable playbook.

Table of Contents

- The Short Answer

- Why Debtors Ignore Invoices (And Why It Matters)

- Step 1: Verify Your Invoice Before You Do Anything Else

- Step 2: Send a Polite but Clear Payment Reminder

- Step 3: Issue a Formal Final Demand

- Step 4: Send a Professional Letter of Demand (LOD)

- Step 5: Hand Over to a Registered Debt Collector

- Step 6: Negotiate a Structured Payment Arrangement

- Step 7: Escalate to Legal Action

- 5 Critical Troubleshooting Tips

- Warning Signs Your Debtor Won’t Pay Without Escalation

- How Kredcor Can Help You Get Paid Faster

- Frequently Asked Questions (FAQ)

Why Debtors Ignore Invoices — And Why Understanding This Matters

Before you pick up the phone or fire off an angry email, it’s worth understanding why a debtor ignores your invoice in the first place. In our experience at Kredcor, there are generally three categories:

- Cash flow problems: The debtor genuinely cannot pay right now. This is, unfortunately, the most common scenario — especially in a tough South African economic environment.

- Administrative oversights: The invoice was lost, went to spam, or the accounts payable contact changed. These cases are usually resolved quickly.

- Deliberate non-payment: The debtor is ducking their obligations. These require firmer, faster escalation.

Understanding which category you’re dealing with shapes your entire approach. A genuinely distressed debtor needs a different strategy to a deliberate avoider. Additionally, the Prescription Act 68 of 1969 means that B2B debts prescribe after three years — so the longer you wait, the weaker your legal position becomes.

“The biggest mistake we see businesses make is waiting too long. Every week of inaction reduces your recovery probability — and increases your legal costs.” — Kredcor Recovery Team

Step 1: Verify Your Invoice Before You Do Anything Else

First and foremost, before you chase a debtor for ignoring your invoice, make absolutely sure the invoice itself is correct. This might sound obvious, but our team has seen dozens of cases where the “non-paying debtor” was actually waiting on a corrected invoice.

What to check:

- Correct company name and registration number on the invoice

- Accurate amount — cross-check against the quote, purchase order, or delivery note

- Your own correct banking details (errors here are surprisingly common)

- The correct payment due date

- Proof of delivery, signed off by the debtor

- The debtor’s purchase order (PO) number, if they require it

If any of these elements are missing or incorrect, fix them first. Then reissue the invoice with a revised date and a short covering email confirming the correction. This protects you legally and removes any excuse for non-payment.

Our team’s experience: We tested this process with a logistics client in Gauteng who had three “non-paying debtors.” In every case, the debtor was waiting for a corrected VAT invoice. Once reissued, two of the three paid within 48 hours.

Step 2: Send a Polite but Clear Payment Reminder

Once you’ve confirmed your invoice is accurate and the due date has passed, it’s time to send a polite, professional payment reminder. At this stage, keep the tone friendly. You want to give the debtor the benefit of the doubt — the invoice may genuinely have slipped through the cracks.

Best practices for your reminder:

- Send it via email and phone — a two-channel approach significantly improves response rates.

- Reference the invoice number, amount, and due date clearly in the subject line and body.

- Keep a written record — always follow up a phone call with an email summary: “As per our telephone conversation today…” This creates a paper trail.

- Set a response deadline — “Please confirm payment or contact us by [date] to discuss.” This removes ambiguity.

- Send within 3 to 5 days of the due date — don’t wait weeks before following up. Act swiftly.

Importantly, document everything. Your documentation becomes critical evidence if the matter escalates to legal action. Keep records of every email, SMS, and call log, including dates and times.

For further reading on managing your credit risk proactively, we recommend our article: The Essential Guide to the Most Important Credit Management Indicators Every CFO and Credit Manager Must Master. It’s packed with actionable benchmarks.

Step 3: Issue a Formal Final Demand

If the polite reminder produces no response, it’s time to escalate to a formal final demand. This is no longer a friendly nudge — it’s a structured, written notice that makes clear you’re serious about recovering the debt.

What your final demand must include:

- Full legal names of both parties

- Invoice number, date, and outstanding amount

- A clear statement that this is a final demand for payment

- A specific deadline — typically 7 calendar days

- A statement of the consequences of non-payment (debt collector referral, legal action, credit bureau listing)

- Your banking details for immediate payment

Send this via email with read receipt and, where possible, registered post. The read receipt and postal confirmation protect you legally.

Pro tip: Even at this stage, keep the language professional and free from personal attacks. You want the debtor to pay — not to dig in defensively. According to the National Credit Act, even commercial debtors have the right to be treated with dignity during the collections process.

“A well-crafted final demand, sent at exactly the right time, resolves over 40% of our pre-legal cases.” — Kredcor Pre-Legal Team

Step 4: Send a Professional Letter of Demand (LOD)

A Letter of Demand (LOD) is more formal than an internal final demand. It’s a structured legal notice — and when it comes on the letterhead of a registered debt collector or attorney, it carries significantly more weight. Many debtors who ignored your previous communications will suddenly respond when they receive a properly formatted LOD.

Want to know exactly how to structure one? We’ve written a detailed guide: How to Write a Powerful Letter of Demand That Actually Gets Paid in South Africa. This article walks you through every element, with templates and examples.

Key elements of an effective LOD:

- Clear identification of the debt: Invoice number, date, amount, and contractual basis

- Reference to prior communications: This shows the debtor had every opportunity to respond

- Specific demand for payment: State the exact rand amount, including any interest if applicable

- 7–10 day response window: Courts look favourably on creditors who gave reasonable notice

- Statement of next steps: Legal action, default listing, or referral to debt collectors

Note that under the Debt Collectors Act 114 of 1998, registered debt collectors are governed by the Council for Debt Collectors — which means they operate within a strict, ethical legal framework. This is reassuring both for creditors and, importantly, for the debtor too.

Step 5: Hand Over to a Registered Debt Collector

If the LOD produces no result, it’s time to bring in professional reinforcement. This is the point where many business owners hesitate — but in our experience, earlier is nearly always better.

At Kredcor, we operate entirely on a no-win, no-fee basis. There are no upfront fees, no monthly retainers, and no hidden costs. We only earn our fee when we successfully recover your money. This makes professional debt collection remarkably accessible, even for SMEs watching every rand.

What a professional debt collector brings to the table:

- Negotiation expertise: Experienced collectors know how to have difficult conversations effectively

- Legal standing: A registered collector’s contact carries more weight than an internal chaser

- Debtor tracing: If the debtor has “disappeared,” professional tracers can locate them

- Default bureau listings: Non-payers can be listed on credit bureaux, which motivates payment

- Preservation of your business relationship: Professional collectors handle matters with discretion and respect

Kredcor is registered with the Council for Debt Collectors of South Africa (Reg Nr 0016365/06) and is a member of the Association of Debt Recovery Agents (ADRA Nr 474). This matters, because it means we operate within a strict code of conduct that protects both you and your debtor.

For a complete overview of the full debt collection process, read our A-Z Guide to Commercial Debt Collection in South Africa: From Invoice to Judgement.

Step 6: Negotiate a Structured Payment Arrangement

Not every debtor who ignores your invoice is a bad actor. Sometimes businesses face genuine financial hardship. In those cases, a structured payment arrangement — negotiated professionally — is often the most practical and fastest path to getting your money back.

How to structure a payment arrangement effectively:

- Get it in writing: An Acknowledgement of Debt (AOD) is essential — it resets the prescription clock and confirms the debtor’s liability

- Agree on realistic instalment amounts: An arrangement the debtor can actually honour is better than one they will default on in month two

- Include interest: Specify the agreed interest rate to compensate you for the delay

- Set a default clause: If one payment is missed, the full outstanding amount becomes immediately due and payable

- Monitor religiously: Don’t assume the arrangement is running — check every payment date

“I’ve seen businesses wait six months for a payment arrangement to “sort itself out.” It rarely does. Monitor every single instalment and act immediately on the first missed payment.” — Kredcor Senior Recovery Manager

Step 7: Escalate to Legal Action

When all pre-legal attempts have been exhausted and the debtor still ignores your invoice, it’s time to consider formal legal action. This is a significant step — but sometimes the only remaining option.

Legal recovery options in South Africa:

- Magistrate’s Court summons: For claims up to R400,000 — faster and cheaper than the High Court

- High Court summons: For larger claims — more complex but necessary for significant amounts

- Default judgment: If the debtor doesn’t defend the claim, you can obtain judgment in their absence

- Garnishee order (Emolument Attachment Order): Deducts payment directly from the debtor’s salary or bank account

- Attachment of assets: Property or assets can be attached and sold to satisfy the judgment

- Default bureau listing: A credit bureau listing impacts the debtor’s ability to obtain credit — a powerful motivator

At Kredcor, we work with a panel of approved law firms across South Africa to facilitate legal collections when required. However, we always exhaust pre-legal options first — because legal action is costlier and slower than pre-legal recovery. Our goal is always to resolve your debtor problem in the fastest, most cost-effective way possible.

5 Critical Troubleshooting Tips When a Debtor Still Won’t Pay

Even when you follow the steps correctly, some debtors prove especially difficult. Here are five troubleshooting tips our team has found invaluable:

Troubleshooting Tip 1: The debtor disputes the invoice

The problem: The debtor suddenly “discovers” a dispute — often conveniently — just as you’re escalating. The solution: Request the dispute in writing within 48 hours. If the dispute is valid, resolve it. If it’s fabricated, your documentation trail will prove it. A written dispute that doesn’t reference specific grounds is almost never legitimate.

Troubleshooting Tip 2: The debtor has “gone silent” and can’t be located

The problem: Phones are off, emails bounce, the physical address is empty. The solution: Professional debt collectors have access to debtor tracing tools, credit bureau records, and field agents. Don’t write the debt off — hand it over. We’ve traced debtors who relocated across the country.

Troubleshooting Tip 3: The debtor is in business rescue or liquidation

The problem: The debtor has entered business rescue proceedings or liquidation. The solution: Act immediately. Lodge your claim with the appointed practitioner or liquidator. You need to register as a creditor to protect your claim. Do not delay — there are strict deadlines.

Troubleshooting Tip 4: The debtor promises to pay but never does

The problem: You keep getting “it’s in the system” or “payment is releasing on Friday” — but nothing ever arrives. The solution: Stop accepting verbal assurances. Require written confirmation of every payment commitment, including reference number and date. Then verify directly with your bank. If two consecutive “Friday payments” don’t arrive, escalate immediately.

Troubleshooting Tip 5: You’re worried about damaging a valuable client relationship

The problem: The debtor is also an important client you don’t want to lose. The solution: Professional debt collectors act as your representative — not as an aggressive third-party agency. At Kredcor, we specifically protect our clients’ brand image throughout the recovery process. The relationship can survive a professional collections approach; it rarely survives months of unpaid invoices.

Warning Signs That Your Debtor Won’t Pay Without Escalation

Our team has identified several red flags that reliably predict a debtor won’t pay voluntarily. For a full breakdown, see our article: 5 Red Flags That Indicate a Commercial Client Won’t Pay. However, the key warning signs include:

- Consistently changing their “accounts payable contact”

- Requesting renegotiation of payment terms after delivery

- Suddenly raising disputes that were never mentioned during the business relationship

- Reducing or ceasing orders while the outstanding invoice grows

- Avoiding direct communication — only emailing, never taking calls

- Asking for extended payment terms while paying other creditors

If you recognise three or more of these signs, do not wait any longer. Every additional week you wait reduces your recovery probability and increases your risk exposure.

How Kredcor Helps You Recover Debt — Without Stress, Lawyers’ Bills, or Guesswork

Since 1999, Kredcor has been South Africa’s trusted commercial debt recovery partner for businesses across Gauteng, Cape Town, KwaZulu-Natal, and beyond — including pan-African and global collections. We work with Blue-Chip companies, SMEs, logistics firms, equipment rental businesses, and homeowners’ associations.

Here’s why our clients choose us over attorneys or generic collection agencies:

- No success, no fee: We earn nothing unless we recover your money

- No upfront costs: No admin fees, handover fees, or monthly retainers

- Dedicated relationship manager: No call centre runaround — you have a direct, senior contact

- Monthly progress reports: Full transparency on every case, every month

- Pre-legal focus: We resolve over 80% of cases before legal costs are triggered

- 26+ year track record: 100% clear record with the Council for Debt Collectors

Whether your debtor is in Johannesburg, Cape Town, Durban, or anywhere across Africa, our team of expert debt collectors in South Africa is ready to act on your behalf — quickly, professionally, and without drama.

Want More Expert Resources on Debt Recovery and Credit Management?

We publish regular, in-depth articles on every aspect of commercial debt collection, credit risk management, and South African credit law. Whether you want to understand the In Duplum Rule, write a better Letter of Demand, or benchmark your debtor days against industry standards, you’ll find it all at our Kredcor Articles page. Bookmark it — it’s your go-to reference library for credit management in South Africa.

Frequently Asked Questions (FAQ)

Q1: How long should I wait before escalating when a debtor ignores my invoice?

Act within 3–5 days of the invoice due date with a polite reminder. If there’s no response within 7 days, issue a final demand. By day 14, send a Letter of Demand. Don’t let more than 30 days pass without involving a professional debt collector — every additional week reduces your recovery probability.

Q2: Can I claim interest on an overdue invoice in South Africa?

Yes — provided your credit terms and/or contract specify an interest rate. In the absence of a contractual rate, the Prescribed Rate of Interest Act sets the default rate. Always include interest provisions in your credit application forms and terms of trade to protect your position.

Q3: What happens if the debtor goes into business rescue while owing me money?

You must register as a creditor with the appointed Business Rescue Practitioner (BRP) as soon as possible. Lodge your claim with supporting documentation (invoices, statements, signed agreements). Failing to lodge your claim in time can result in losing your right to any payout. Get professional assistance immediately — the timelines are strict.

Q4: Is it worth using a professional debt collector for smaller amounts?

Absolutely — especially when the collector works on a no-win, no-fee basis like Kredcor. Even for smaller amounts, the time cost of chasing the debt yourself often exceeds the debt value. Furthermore, professional collectors recover a significantly higher percentage of debts than self-managed collections. There is genuinely no downside to using a registered, ethical debt collector for any B2B debt.