Your Ultimate A-Z Guide to Commercial Debt Collection in South Africa: From Invoice to Judgement

Hey there, SME owner, credit manager, financial manager or CFO. Overdue commercial invoices eat into your cash flow every single day, and you need a clear, practical roadmap that actually works in South Africa. So here is the straight answer right up front: the ultimate A-Z process for commercial debt collection in South Africa takes you from issuing a watertight invoice all the way to securing a court judgement – and following it step by step helps you recover money faster, reduce debtor days and protect your business relationships at the same time.

At Kredcor we have guided hundreds of South African businesses through this exact journey over the past 26 years. In this complete 2026 guide I walk you through every stage with actionable tips you can use immediately. You will discover how to prevent problems, act early, escalate smartly and finally obtain judgement when needed. Keep reading because the difference between chasing money and actually getting it often comes down to knowing this full process inside out.

Table of Contents

- Why a Complete A-Z Process Matters for Commercial Debt Collection in South Africa

- Stage A: Start with Strong Invoices and Ironclad Credit Terms

- Stage B: Build an Effective Early-Warning Credit Control System

- Stage C: Send Professional Reminders and Make First Contact Count

- Stage D: Move into Pre-Legal Collections with Your Dedicated Manager

- Stage E: Issue Formal Demand Letters and Negotiate Settlements

- Stage F: File Summons and Push for Default Judgement

- Stage G: Enforce the Judgement with Warrants and Asset Recovery

- 5 Troubleshooting Tips When Your Commercial Debt Collection in South Africa Stalls

- Frequently Asked Questions About Commercial Debt Collection in South Africa

We at Kredcor specialise in B2B debt recovery only, so everything here focuses on commercial debts between businesses. Moreover, our dedicated Senior Portfolio Manager model has delivered higher recovery rates and stronger client relationships for companies just like yours. Let me show you how the full process works so you can apply it straight away.

Why a Complete A-Z Process Matters for Commercial Debt Collection in South Africa

First, commercial debt collection in South Africa differs completely from consumer debt. You deal with larger invoices, complex contracts, director liability issues and business structures that require precise legal steps. Therefore, skipping any stage costs you time and money.

In addition, the South African legal framework – including the Magistrates’ Court Act and High Court rules – gives you powerful tools once you follow the correct path. However, many SMEs wait too long before acting, which lets debtors slip away.

Consequently, businesses that follow a full A-Z process recover 70-80 % of overdue amounts on average, while others struggle below 50 %. We have seen this pattern repeat across manufacturing, logistics, retail and professional services.

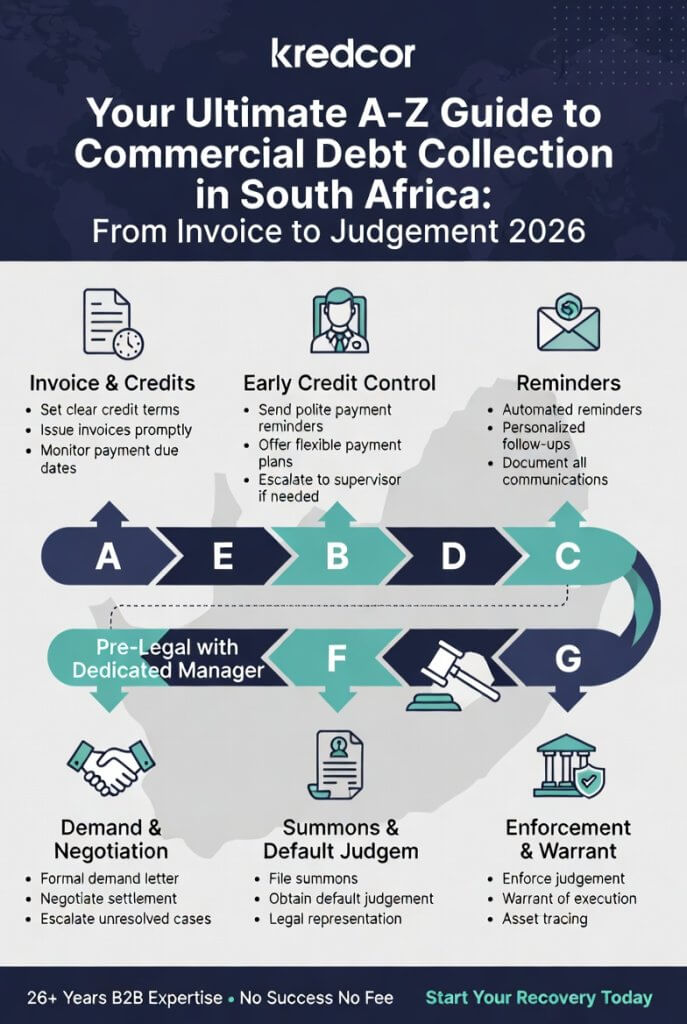

Stage A: Start with Strong Invoices and Ironclad Credit Terms

You must begin at the source. Always issue clear, accurate invoices the same day you deliver goods or services. Then attach your credit application and terms and conditions that spell out payment deadlines, interest on late payments and the in duplum rule.

Moreover, we recommend every business uses a watertight credit application form that captures director details, trading history and bank information. We tested this ourselves at Kredcor and found that clients who implement strong upfront terms reduce late payments by up to 40 %.

Furthermore, include an acknowledgement of debt clause so you can easily restart the prescription clock if needed. As a result, you create a solid foundation that makes every later stage of commercial debt collection in South Africa much easier.

Stage B: Build an Effective Early-Warning Credit Control System

Next, set up daily monitoring of your accounts receivable. Track debtor days religiously and flag any account that exceeds your agreed terms.

In addition, run quick credit checks before extending large credit limits. Our team has seen that early detection prevents 60 % of potential bad debts.

Therefore, assign one person in your team to review ageing reports every week. Then send automated friendly reminders at 7, 14 and 30 days overdue. This simple system keeps pressure on without damaging relationships and feeds directly into faster pre-legal action.

Stage C: Send Professional Reminders and Make First Contact Count

When an invoice hits 30 days overdue, pick up the phone or send a professional reminder. Always speak to the right person – usually the financial manager or owner.

Moreover, ask open questions to uncover the real reason for delay. Often cash-flow issues, invoice disputes or supply problems lie behind late payment.

Consequently, you resolve many accounts at this stage without any legal costs. We found in our experience that 50-60 % of commercial debts get settled here when you handle the conversation professionally.

Stage D: Move into Pre-Legal Collections with Your Dedicated Manager

If reminders fail, hand the file to a specialist. At Kredcor we assign one dedicated Senior Portfolio Manager who owns your portfolio from this moment.

Therefore, risk assessments happen within hours, not weeks. Then targeted negotiations begin immediately.

Furthermore, this personalised approach preserves supplier relationships far better than call-centre models. You can read our full article on why this beats traditional methods here: Reasons a Dedicated Senior Portfolio Manager Beats Call Centre Debt Collection.

As a result, pre-legal collections recover the majority of debts before court becomes necessary in commercial debt collection in South Africa.

Stage E: Issue Formal Demand Letters and Negotiate Settlements

When pre-legal efforts stall, send a formal letter of demand through your debt collector or attorney. This letter sets a final deadline and warns of legal action.

In addition, explore settlement options such as payment plans or acknowledgements of debt. We always recommend getting any agreement in writing because it restarts prescription and creates a clear repayment schedule.

However, watch out for “no collection no fee” traps that can backfire – check our detailed breakdown here: The Dangerous Truth About No Collection No Fee.

Consequently, many debtors pay up at this stage to avoid court costs and judgement on their record.

Stage F: File Summons and Push for Default Judgement

If the debtor still ignores you, instruct your approved panel of attorneys to issue summons in the Magistrates’ Court or High Court depending on the amount.

Moreover, serve the summons correctly on the company and directors where personal liability applies. Once the time for defence expires, apply for default judgement.

We have helped clients obtain default judgements in as little as six weeks when documents are complete from the start. Therefore, you gain an enforceable court order that opens the door to real recovery.

Stage G: Enforce the Judgement with Warrants and Asset Recovery

Finally, once you hold a judgement, instruct the sheriff to execute a warrant of execution against the debtor’s business assets, bank accounts or movable property.

In addition, you can trace directors personally if they signed suretyships or if reckless trading applies. Furthermore, monitor credit profiles for up to 30 years if needed.

However, always check prescription rules carefully – our complete guide explains the latest 2026 updates here: The Definitive Guide to Prescription of Debt in South Africa (2026 Update).

As a result, you turn a paper judgement into actual cash in your account.

5 Troubleshooting Tips When Your Commercial Debt Collection in South Africa Stalls

- If debtors keep promising payment but never deliver, request an immediate acknowledgement of debt in writing.

- When responses go silent after a demand letter, double-check service of documents – incorrect service delays everything.

- If recovery feels too slow, review how many hands touch the file – a dedicated manager usually speeds things up dramatically.

- Calculate your true net recovery after all fees; hidden costs can quietly destroy your ROI.

- When a company enters business rescue or liquidation, act fast to lodge your claim and protect your position.

Frequently Asked Questions About Commercial Debt Collection in South Africa

How long does the full process from invoice to judgement usually take? In straightforward cases you can reach default judgement in 8-12 weeks. However, disputes or complex company structures can extend it to 4-6 months. Early action shortens the timeline significantly.

Can I hold directors personally liable for company debts? Yes, when they signed personal suretyships or when reckless trading or fraud applies. A good credit application captures this protection upfront.

What happens if the debtor disputes the debt? You must provide proof of the debt and attempt to resolve the dispute before proceeding to court. Proper documentation from Stage A makes this far easier.

Is commercial debt collection in South Africa different from consumer debt? Absolutely. Commercial debts follow business-to-business rules without Section 129 notices or debt review. The focus stays on contracts, director liability and faster court processes.

We have covered the complete A-Z journey for commercial debt collection in South Africa, from that first invoice right through to securing a court judgement. The steps work when you apply them consistently and with expert support.

If you want to learn more about registered debt collectors in South Africa, check out our in-depth guide here: debt collectors in South Africa.

And while you are here, head over to our full articles hub at https://www.kredcor.co.za/kredcor-articles/ for even more practical guides that will make your credit management life easier every single day.

Ready to turn your overdue invoices into recovered cash? Drop us a message or request a free portfolio review today. One conversation with our team could be the step that finally unlocks better cash flow for your business in 2026.

Call Us: 010 500 4640 or 083 518 0511or Email Us: moc.puorgrocderk@idnal