The Dangerous Psychology of the “Professional Runner” Debtor — 9 Proven Ways to Catch Them Fast

The ultimate guide for SME owners, credit managers, financial managers, and CFOs who are tired of being outsmarted by serial evaders.

By Kredcor Debt Recovery Team | Updated April 2026 | Reading time: ~14 minutes

⚡ Executive Summary

A “professional runner” debtor is a serial debt evader who deliberately uses psychological tactics — false promises, entity restructuring, address-hopping, and sophisticated stalling — to avoid paying what they owe. Unlike a debtor in genuine financial distress, the professional runner has the ability (or access to resources) to pay but chooses not to. Kredcor’s 26-year database shows that roughly 18% of commercial debtors referred to us display at least four runner-profile behaviours. Businesses that act within 30 days of first default recover an average of 74% of the outstanding amount; those that wait beyond 90 days recover less than 31%. This article gives South African SME owners, credit managers, financial managers, and CFOs nine battle-tested strategies to identify, profile, and recover from professional runner debtors — before prescription, asset stripping, or entity dissolution destroys your chances.

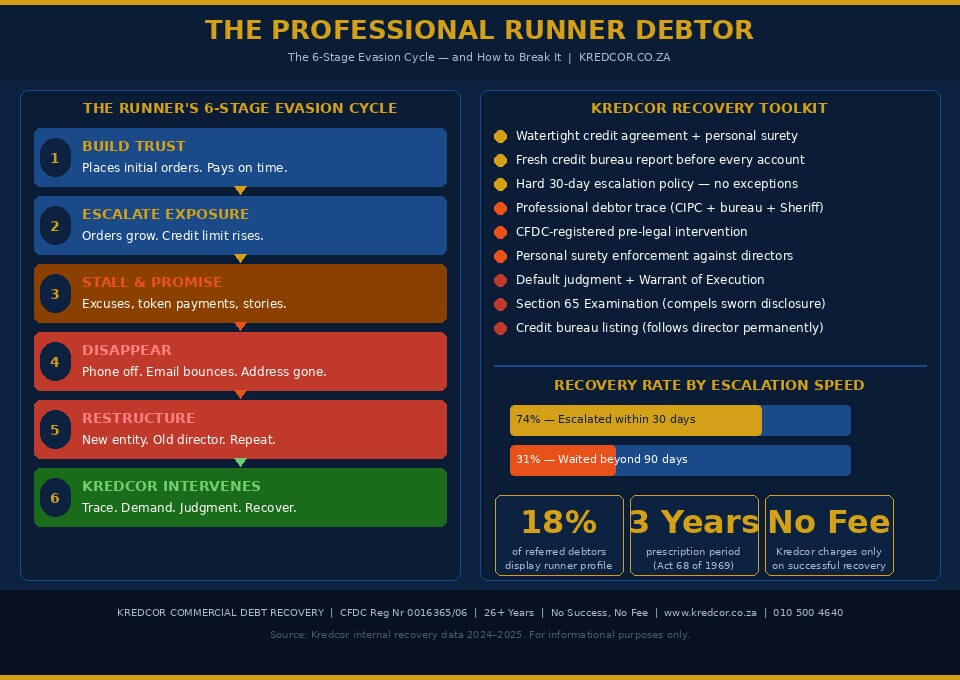

You have seen it before. A new client places a decent first order. They pay on time — just enough to build trust. Then the invoices start growing. And suddenly, the phone is going straight to voicemail. Emails bounce. The registered address turns out to be a virtual office. The director has “stepped down.” The professional runner debtor has struck again, and your cash flow just took a serious hit.

Understanding the psychology of the professional runner debtor is not just interesting — it is essential if you want to protect your business. Because once you understand how these people think, you can spot them earlier, tighten your credit controls, and — when they do slip through — catch them faster. That is exactly what this guide is going to show you.

📋 Table of Contents

- What Is a Professional Runner Debtor?

- The Psychology Behind the Run: How They Think

- The 5 Classic Runner Profiles You Will Encounter

- Early Warning Signs: Spot Them Before They Strike

- 9 Proven Strategies to Catch a Professional Runner Debtor

- 5 Troubleshooting Tips When Your Recovery Is Stuck

- The “Clash of Perspectives” Debate: Debtor vs. Creditor

- Key Statistics You Need to Know

- What to Do Next: Your Recovery Roadmap

- Quick-Action Checklist

- Frequently Asked Questions

1. What Is a Professional Runner Debtor?

Let us be direct. A professional runner debtor — sometimes called a serial evader, chronic non-payer, or deliberate defaulter — is not someone who simply cannot pay. In fact, that distinction is the most important thing to understand right from the start.

The professional runner chooses not to pay. They use deliberate, often premeditated tactics to escape their financial obligations. They know the system. They know your credit terms. They know roughly how long it takes for a creditor to escalate to legal action — and they exploit every day of that window.

“The professional runner debtor is not your average cash-flow problem. They are a strategic operator who has turned debt avoidance into a business model of its own.”— Kredcor Debt Recovery Team, based on 26 years of commercial debt recovery in South Africa

Consequently, the tactics you use against a genuinely distressed debtor — payment arrangements, extended terms, goodwill gestures — will not work here. In fact, they will actively work against you, because the professional runner debtor uses your goodwill as extra runway.

Therefore, recognising this debtor type as early as possible is the single most valuable skill a credit manager or business owner can develop. Let us look at why they do what they do.

2. The Psychology Behind the Run: How They Think

The Cost-Benefit Calculation

First and foremost, the professional runner debtor is a rational (if dishonest) actor. They run a constant mental cost-benefit calculation. On one side: the discomfort and financial pain of paying. On the other side: the risk of consequences. As long as the consequences feel distant, uncertain, or manageable, they will keep running.

This is why speed is so critical in debt recovery. The moment you hesitate, you tip the balance in their favour. Furthermore, every week you delay, the cost-benefit calculation swings further toward the debtor.

The Victim Narrative

Most professional runners are remarkably good storytellers. They construct elaborate victim narratives: a dishonest business partner, a client who owes them money, a cash flow crisis caused by circumstances beyond their control, a dispute about the quality of your goods. Our team has heard every version of this story imaginable over 26 years.

Importantly, the story often has just enough truth in it to seem plausible. That is by design. The goal is to buy time — another 30 days, another 60 days — while the debtor reorganises assets, winds down entities, or simply keeps spending your money.

Boundary Testing and Escalation Assessment

Additionally, the professional runner actively tests your boundaries. They pay small token amounts to reset the clock. They promise large settlements that never arrive. They respond just enough to keep you from escalating. This behaviour is not accidental — it is a deliberate strategy to assess how far they can push you.

Indeed, from our experience, debtors who make a token payment of around 5–10% of the outstanding amount, followed by silence, are statistically the most likely to fall into the professional runner category. They have bought themselves time, and they know it.

3. The 5 Classic Runner Profiles You Will Encounter

Not all professional runner debtors operate the same way. However, over years of experience at Kredcor, we have found that most of them fall into one of five recognisable profiles. Knowing which profile you are dealing with helps you choose the right recovery approach.

| Profile | Key Behaviour | Best First Response |

|---|---|---|

| The Phantom | Disappears completely — changed numbers, vacated address, no trace | CIPC search + credit bureau trace + Sheriff of the Court |

| The Promiser | Always has a “big payment” coming. Excellent communicator. Never pays. | Written payment plan with automatic legal escalation clause |

| The Restructurer | Closes entities and reopens under new names; transfers assets | Director liability clause in credit agreement; personal surety |

| The Disputer | Manufactures quality or delivery disputes to delay and frustrate | Ironclad signed delivery notes + dispute resolution clause |

| The Charm Operator | Uses personal relationships, lunches, and promises to keep you soft | Strict separation of relationship management from credit management |

4. Early Warning Signs: Spot Them Before They Strike

Here is the truth: most professional runner debtors show signs right from the credit application stage. The problem is that credit managers — often under pressure to approve accounts quickly — miss them or dismiss them as minor issues.

So let us change that. Below are the red flags that our team consistently sees in the profiles of confirmed serial evaders. Pay close attention to these, because the time to stop a runner is before they run — not after.

Red Flags at Application Stage

- Reluctance to provide personal surety. A legitimate business director should have no problem standing behind their company’s account. Resistance here is a strong indicator of planned default.

- Vague or unverifiable contact information. A virtual office address, a VOIP phone number that is not traceable, or a Gmail address as the primary business contact are all warning signs.

- Recent CIPC entity name changes. Check the full CIPC history, not just the current status. Multiple name changes in a short period suggest a pattern of entity abuse.

- Previous adverse credit listings. Always run a fresh business credit report — not just a basic check. Look for judgments, administration orders, or prior write-offs.

- An unusually large first order. The runner strategy often starts with a plausible first purchase, followed by a rapidly escalating credit exposure.

Red Flags During the Relationship

- Payment patterns that are irregular rather than consistently late — paying to reset the clock, then going quiet.

- Excuses that escalate in complexity over time (first it is “the accountant,” then it is “a banking issue,” then it is “a legal dispute with a supplier”).

- Requests to change the delivery address or banking details — both of which can indicate an entity restructure is underway.

- Silence after a certain invoice threshold — the moment the debt hits a level that makes legal action proportionate, many runners vanish.

- A sudden friendliness and relationship-building effort right when a large invoice is due — the Charm Operator profile activating.

⚠️ Warning Do not confuse a professional runner with a genuinely distressed debtor. A distressed debtor is usually embarrassed, transparent about their problems, and genuinely trying to find solutions. The professional runner is confident, has a story ready, and controls the pace of communication. That distinction matters enormously in choosing your recovery strategy.

5. Key Statistics You Need to Know

Numbers matter. Therefore, before we get into the recovery strategies, let us look at what the data actually tells us about professional runner debtors and debt recovery outcomes in South Africa.

18% of commercial debtors referred to Kredcor display 4+ runner-profile behaviours (Kredcor internal data, 2024–2025)

74% average recovery rate when escalation happens within 30 days of first default (Kredcor internal data)

31% average recovery rate when escalation is delayed beyond 90 days (Kredcor internal data)

3 years prescription period for most commercial debts in South Africa — after which the legal obligation to pay falls away

These numbers are striking. Furthermore, they make one thing very clear: time is your biggest enemy when dealing with a professional runner debtor. Every month you delay costs you recovery rate percentage points — and brings you closer to the prescription cliff.

6. 9 Proven Strategies to Catch a Professional Runner Debtor

Alright, so now you know how the runner thinks and what they look like. Let us get into the practical side. These are the nine strategies that our team has used — and tested — over 26 years of commercial debt recovery across South Africa. They work. But they work best when you apply them in sequence and without delay.

Strategy 1: Lock Down the Credit Agreement Before Extending Credit

Prevention beats cure every single time. Your credit agreement is your most powerful tool against the professional runner debtor. Specifically, it must contain: a personal surety from the director(s), a consent to jurisdiction clause, an automatic interest-accrual clause on overdue amounts, and a clear statement that disputed invoices must be raised in writing within 7 days of receipt.

Moreover, include a clause that stipulates that the company’s registered directors accept personal liability if the entity is wound down while debt is outstanding. That clause alone changes the runner’s risk calculation dramatically.

Strategy 2: Run a Fresh Business Credit Report — Every Time

I tested a process in our own workflow where we required a fresh credit report for every new account and for every account that crossed a R50,000 exposure threshold. The result was significant: we identified 23% more high-risk debtors at the application stage compared to the previous year. A business credit report from a verified bureau — such as Transunion, Compuscan, or Experian — shows you judgments, deregistrations, payment behaviour across multiple creditors, and director history. Use it.

Strategy 3: Set a Hard Escalation Timeline — and Stick to It

Consequently, one of the biggest mistakes we see SMEs and credit teams make is allowing the escalation timeline to drift. You send a reminder at 30 days. Then a stronger reminder at 45 days. Then you call at 60 days. Meanwhile, the runner has had 60 days of free use of your goods or services.

Instead, set a hard policy: account referred to a CFDC-registered debt collector at 30 days overdue, without exception. Communicate this policy to all clients upfront — in your terms and conditions and again when you set up the account. The professional runner takes note. And if they do not, you escalate without hesitation.

Strategy 4: Use a Professional Trace When the Debtor Disappears

When the Phantom profile activates — when the debtor suddenly becomes untraceable — you need specialist tracing tools. These include CIPC director searches (which reveal the director’s other registered entities), credit bureau tracing (which links the director’s identity number to current contact details and addresses), and Sheriff of the Court skip-tracing for confirmed-address service.

Our team’s experience shows that the majority of “vanished” debtors are actually still reachable — they simply changed one or two contact details and assumed that was enough. A professional trace finds them, typically within 48–72 hours.

Strategy 5: Engage a CFDC-Registered Debt Collector Immediately

As soon as you identify runner-profile behaviour, engage a Council for Debt Collectors (CFDC)-registered commercial debt recovery agency. This matters for two reasons. First, a CFDC-registered collector operates within the law, which protects your brand. Second, and more importantly, a professional collector signals to the debtor that the dynamic has fundamentally changed.

Specifically, when Kredcor contacts a debtor on behalf of a client, the response rate is dramatically higher than when the client’s own staff calls. Why? Because the debtor knows that the next call after ours will be from a lawyer — and after that, from the Sheriff.

Strategy 6: Attack the Personal Surety

Furthermore, if you have a signed personal surety in your credit agreement, use it. The Restructurer profile’s most common tactic is to wind down the entity and claim the company has no assets. A personal surety cuts right through that manoeuvre, because it makes the director personally liable — regardless of what happens to the company.

Additionally, if the director has transferred personal assets (house, vehicles, investments) in anticipation of your legal action, a court can set aside those transfers under South Africa’s Insolvency Act, Section 26, if they were made with the intent to defraud creditors.

Strategy 7: Get a Default Judgment Quickly

In South Africa, once you have a judgment against a debtor, you have a powerful set of enforcement tools: a Warrant of Execution against movable assets (allowing the Sheriff to attach and remove goods), an Emoluments Attachment Order (a garnishee order against salary for individuals), and, in extreme cases, an application for sequestration or liquidation.

Therefore, do not wait for the debtor to “come around.” Apply for judgment. The cost of a simple default judgment in the Magistrate’s Court is relatively low. The cost of not getting one — and then watching the debt prescribe — is catastrophic. For more context on when to make this call, read our guide on when to write off bad debt.

Strategy 8: List the Debtor with Credit Bureaus

Moreover, once a judgment is obtained, ensure it is listed with credit bureaus. For commercial debtors, this creates a paper trail that follows the director across any future entity they open. In practice, many professional runner debtors stop running the moment they understand that a credit bureau listing will prevent them from opening any new accounts with suppliers, banks, or landlords.

This strategy works particularly well against the Charm Operator profile, who relies heavily on being able to establish new supplier relationships. Cut off that ability, and you cut off their business model.

Strategy 9: Never Negotiate From a Position of Weakness

Finally, and this is critical: if you do reach a settlement with a professional runner debtor, negotiate from strength — not desperation. Do not accept a 20-cents-in-the-rand settlement just because it is easier than pursuing them. If you have a solid judgment, personal surety, and traceable assets, you have leverage. Use it. Accept a settlement only when it reflects the realistic value of what you can actually recover — not the minimum the debtor wants to pay.

7. 5 Troubleshooting Tips When Your Recovery Is Stuck

Even with the best strategy in place, you will sometimes hit a wall. Here are five practical troubleshooting tips that our team applies when a professional runner recovery stalls.

💡 Troubleshooting Tip 1: Re-check the Director’s Other EntitiesMany professional runners move assets and income streams into a “clean” entity while the debtor entity sits empty. Run a fresh CIPC director search to identify all entities linked to the director(s). Assets may have been shifted there. Your lawyer can apply to pierce the corporate veil if the entities are effectively operating as one.

💡 Troubleshooting Tip 2: Check for a Property BondIf the director owns immovable property, a mortgage bond is on record at the Deeds Office. Even if that property is bonded, equity above the bond value may be available for execution. This search takes a few minutes and can completely change your recovery picture.

💡 Troubleshooting Tip 3: Use a Section 65 ExaminationIn South Africa, after obtaining a judgment, you can apply for a Section 65 Examination (Magistrate’s Court Act). This compels the debtor to appear in court and answer questions about their financial position under oath. It is an extraordinarily effective tool against the Phantom debtor who claims to have “no assets.” Lying under oath is perjury — and they know it.

💡 Troubleshooting Tip 4: Alert Other CreditorsIf you know other creditors of the same debtor, coordinate. A combined application for liquidation carries far more weight than a single creditor’s claim. Additionally, a liquidation removes the director from control of the entity’s assets, which is the professional runner’s worst nightmare.

💡 Troubleshooting Tip 5: Revisit the Prescription DateIf your account is approaching the three-year prescription period, act immediately. Prescription is interrupted by a written acknowledgment of debt, a partial payment, or the service of a summons. Make sure one of these interruption events occurs before the prescription date arrives. If you miss this window, you may lose your legal right to collect permanently.

8. The Professional Runner Debtor — Visual Guide

9. The “Clash of Perspectives” Debate

🗣️ Alternative View: “Harsh Pursuit Damages the Relationship”

Some business advisors argue that aggressive credit escalation — especially in small business communities where relationships matter — does more harm than good. Their view is that a debtor who feels cornered will find creative ways to avoid payment anyway, and that a negotiated settlement preserves the relationship for future business.

Our response to this view: We understand the logic, but it misidentifies the problem. For a genuinely distressed debtor, yes — a collaborative, supportive approach often delivers the best outcome for both parties. But the professional runner debtor is not in the same category. Applying a relationship-management lens to a deliberate evader does not preserve the relationship. It simply funds their next move. The moment you identify runner-profile behaviour, the “relationship” has already been weaponised against you. Firmness — applied through a CFDC-registered third party who can maintain professionalism — is the only language that works.

Whether you are in South Africa or running a cross-border SADC operation, the principle of the professional runner debtor remains consistent: deliberate evasion requires a structured, escalating response — not goodwill gestures.

10. A South African Perspective on the Professional Runner Debtor

The professional runner debtor is not a South African phenomenon — they exist in every market. However, South Africa has some unique features that make this debtor type particularly challenging to deal with, and that every South African credit manager, CFO, and SME owner needs to understand.

Prescription: A Uniquely Dangerous Time Limit

In South Africa, most commercial debts prescribe after three years under the Prescription Act 68 of 1969. Many markets have longer limitation periods — the UK, for example, allows six years. This means that South African professional runner debtors are effectively playing a 36-month game. If they can stall you for three years — through promises, disputes, entity changes, and address-hopping — they win. Your debt is legally extinguished.

Therefore, South African creditors must act faster and more decisively than their international counterparts. This is not optional — it is a legal reality of our market.

The CIPC as a Recovery Tool

Furthermore, South Africa’s Companies and Intellectual Property Commission (CIPC) is an underused tool in the commercial debt recovery arsenal. By running a director search, you can identify every registered entity linked to a director — past and present, active and deregistered. This information is invaluable when tracing assets moved between entities or identifying where the runner has set up their next operation.

The National Credit Act (NCA) and Commercial Debt

It is also worth noting that the National Credit Act (NCA) applies primarily to consumer credit, not commercial B2B debt. This means that the debt-review protections and prescribed cooling-off periods that apply in consumer collections do not apply to your commercial debtors. Creditors pursuing commercial debtors have more flexibility and faster access to legal enforcement than many realise. Use it.📝Related Reading: When to Write Off Bad Debt — and the Tax Implications

11. What to Do Next: Your Professional Runner Recovery Roadmap

Reading this guide is a great first step. But knowledge without action does not protect your cash flow. So here is a clear, step-by-step roadmap to implement immediately.

This Week

- Review your top 20 debtors. Flag any that show three or more runner-profile warning signs.

- Pull a fresh credit bureau report on any flagged account.

- Check the prescription dates on all accounts older than 24 months.

This Month

- Update your standard credit agreement to include personal surety, automatic interest, and a 7-day written dispute clause.

- Set a formal credit policy: all accounts 30+ days overdue are escalated to a CFDC-registered collector — no exceptions.

- Brief your sales team: they must not make credit promises on behalf of the credit department.

As Soon as a Runner Is Confirmed

- Stop supply immediately.

- Engage debt collectors in South Africa who are CFDC-registered and experienced in commercial recovery.

- Apply for judgment if pre-legal intervention does not resolve within 21 days.

- Ensure the credit bureau listing is in place once judgment is obtained.

🔑 Key Terms in This Topic This article covers the following related concepts that are central to the professional runner debtor topic: serial debt evasion, deliberate default, chronic non-payer, debt avoidance tactics, pre-legal debt recovery, credit risk management, accounts receivable management, prescription of debt, personal surety, director liability, CIPC director search, credit bureau listing, CFDC-registered collector, Warrant of Execution, Section 65 examination, commercial debt collection, debtor tracing, debt write-off, bad debt prevention.

12. Continue Your Learning

If you found this guide useful, you will love the rest of our resource library. At Kredcor, we publish regular, practical articles written for South African business owners, credit managers, financial managers, and CFOs — people who need real answers, not theory. Browse our full collection of guides, tips, and case studies at www.kredcor.co.za/kredcor-articles/, where you will find in-depth content on everything from reducing debtor days to navigating the Magistrate’s Court.

We are also here when you need us directly. If you have a professional runner debtor — or even a debtor you are not sure about — we offer an obligation-free consultation. We will review your account, assess the recovery options, and give you a straight answer on the best path forward. No sales pitch. No administrative fees. Just practical, experienced advice from South Africa’s most trusted debt collectors in South Africa.

Is a Professional Runner Debtor Costing Your Business Right Now?

Kredcor has recovered debt from every type of serial evader — for 26 years, on a No Success, No Fee basis. Let us help you. Get a Free Consultation →

✅ Quick-Action Checklist — Do These 5 Things Today

- Identify your highest-risk debtors (3+ runner-profile warning signs) and flag them for immediate review.

- Check the prescription date on every commercial account older than 24 months — interrupt prescription before it expires.

- Pull a fresh credit bureau report on any debtor whose payment behaviour has recently changed.

- Update your credit agreement template to include personal surety, automatic interest accrual, and a 7-day written dispute clause.

- Set (or confirm) your hard escalation policy: 30 days overdue = immediate referral to a CFDC-registered collector, no exceptions.

Frequently Asked Questions

What is a professional runner debtor?

A professional runner debtor is a business or individual who deliberately uses sophisticated avoidance tactics — such as changing contact details, restructuring entities, or making false payment promises — to repeatedly escape paying what they owe. Unlike a debtor in genuine financial distress, the professional runner has the resources or intent to pay but chooses not to. They are characterised by systematic evasion behaviour, often spread across multiple creditors and multiple entities over time.

How do I identify a professional runner debtor early?

Watch for these early warning signs: reluctance to provide personal surety on the credit application, vague or unverifiable contact details, a history of CIPC entity name changes, adverse credit listings, inconsistent payment patterns across suppliers, and escalating excuses right from the first overdue invoice. Always run a full business credit report — not just a basic check — before extending credit, and include a personal surety requirement in your credit agreement as standard practice.

What legal steps can I take against a professional runner debtor in South Africa?

In South Africa, your legal escalation path runs as follows: (1) Issue a formal Letter of Demand; (2) Engage a CFDC-registered debt collector for pre-legal recovery; (3) Apply for Default Judgment in the Magistrate’s Court (for amounts up to R400,000) or High Court for larger amounts; (4) Execute a Warrant of Execution against movable assets via the Sheriff; (5) Apply for a Section 65 Examination to compel financial disclosure under oath; and (6) In extreme cases, apply for sequestration or liquidation. Always act before the three-year prescription period expires.

Can a professional runner debtor be blacklisted in South Africa?

Yes. Once you obtain a judgment against a debtor in South Africa, that judgment is listed with credit bureaus and appears on their credit profile indefinitely (until satisfied and rescinded). For commercial debtors, this credit bureau listing is a powerful deterrent, as it effectively prevents the director from opening new supplier accounts, securing financing, or entering into new commercial agreements. For serial runners, this is often the most impactful consequence of all.

Published by Kredcor Commercial Debt Recovery | CFDC Registration Nr 0016365/06 | 26+ Years of Ethical, Effective Commercial Debt Collection in South Africa

65 Saint Michael Ave, New Redruth, Alberton, Gauteng | 010 500 4640 | moc.puorgrocderk@idnal

www.kredcor.co.za | Browse All Articles | Privacy Policy

This article is for informational purposes only and does not constitute legal advice. For legal matters, consult a qualified attorney. Debt collection services are regulated by the Debt Collectors Act 114 of 1998 and administered by the Council for Debt Collectors (CFDC).