Credit Insurance vs Third-Party Debt Collection: The Definitive 2026 Guide Every Smart SME Needs

⚡ Executive Summary

Credit insurance vs third-party debt collection — both protect your business against bad debt, but they work in fundamentally different ways. Credit insurance is a proactive financial product: you pay a premium, and if a customer fails to pay, your insurer reimburses 75–90% of the invoice value. Third-party debt collection is a reactive service: a registered agency pursues your overdue accounts on your behalf, typically on a no-success-no-fee basis. For most South African SMEs, third-party debt collection delivers faster cash flow, lower upfront cost, and greater flexibility — especially when debt is placed within 60–90 days of default. Credit insurance adds value for businesses with concentrated debtor exposure or turnover above R40 million. The smartest businesses use both tools strategically. Kredcor, registered with the Council for Debt Collectors (CFDC Reg Nr 0016365/06) and a member of ADRA, has recovered commercial debt for South African businesses for over 26 years.

Let’s be honest — managing debtor risk is one of the most stressful parts of running a South African business. You’ve delivered the goods, rendered the service, and sent the invoice. Then… nothing. Days become weeks, weeks become months, and suddenly your cash flow looks like a drought-stricken dam.

So, when it comes to protecting your business, which tool actually works better — credit insurance or third-party debt collection? And, more importantly, do you even know the difference between the two?

At Kredcor, we’ve spent over 26 years working with SME owners, credit managers, financial managers, and CFOs across South Africa. As a result, we’ve seen both tools in action — and we know exactly when each one earns its keep. In this guide, we give you the full, unfiltered picture so that you can make the best decision for your business.

📋 Table of Contents

- What Is Credit Insurance? (And What It Actually Covers)

- What Is Third-Party Debt Collection? (And How It Works in SA)

- Head-to-Head Comparison: Credit Insurance vs Debt Collection

- Key Statistics Every Business Owner Must Know

- When Should You Use Credit Insurance?

- When Should You Use Third-Party Debt Collection?

- Can You Use Both Together?

- A Clash of Perspectives: The Debate You Need to Hear

- 5 Troubleshooting Tips: When Things Go Wrong

- What to Do Next: Your Credit Risk Action Plan

- Quick-Action Checklist (Do This Today)

- Frequently Asked Questions

1. What Is Credit Insurance? (And What It Actually Covers)

First things first — let’s define the term clearly. Credit insurance (also called trade credit insurance or debtor insurance) is a financial product that protects your business against the risk that a customer will not pay an invoice. Think of it as insurance for your accounts receivable book.

When you take out a credit insurance policy, the insurer assesses your debtors and sets limits on how much credit exposure they’re willing to cover per customer. If a covered debtor then defaults — because of insolvency, protracted default (simply refusing to pay), or political risks in export markets — the insurer pays out a percentage of the unpaid invoice, typically 75% to 90% of the face value.

What Does Credit Insurance Cover?

- Commercial risk: Customer insolvency, liquidation, or business rescue

- Protracted default: The customer simply doesn’t pay within a defined waiting period

- Political risk (for export policies): Currency restrictions, war, or government action that prevents payment

- Pre-shipment risk: Some policies cover losses before goods are even dispatched

What Credit Insurance Does NOT Cover

- Disputed invoices where the customer contests the debt

- Debtors not approved by the insurer at the time of the transaction

- Accounts already in arrears when the policy starts

- The full 100% of the invoice — you always carry a portion of the risk

💡 Key Insight Major credit insurance providers operating in South Africa include Coface, Euler Hermes (Allianz Trade), and Lombard. Each offers slightly different policy structures, so comparison shopping is essential before you sign.

Furthermore, credit insurance is not cheap. Premiums typically range from 0.1% to 0.5% of your insured turnover, depending on your industry, your debtors’ creditworthiness, and the policy structure you choose. For a business with R10 million in insured receivables, that’s R10,000 to R50,000 per year — before you even factor in excesses and claim waiting periods.

2. What Is Third-Party Debt Collection? (And How It Works in SA)

Third-party debt collection is a completely different animal. Instead of paying a premium upfront to prevent losses, you call in a specialist agency after a debtor defaults. The agency pursues the outstanding amount on your behalf — and typically charges you nothing unless they successfully recover the money.

In South Africa, third-party debt collection is a regulated profession. Every agency and individual collector must be registered with the Council for Debt Collectors (CFDC), which was established under the Debt Collectors Act 114 of 1998. Unregistered collection is, therefore, a criminal offence.

How Does Third-Party Debt Collection Work?

- You hand over the account. You provide the agency with the debtor’s details, invoice documentation, and any correspondence.

- The agency contacts the debtor. They issue a formal demand, negotiate a payment arrangement, and escalate as needed.

- Money is recovered and paid over. Funds are paid directly into your bank account or into the agency’s audited trust account, and then transferred to you.

- You pay a commission on success only. At Kredcor, for instance, we work on a strict no-success-no-fee basis — with no admin fees, no handover fees, and no monthly charges.

“The sooner you hand a bad debt to a registered collection agency, the better your chances of recovering the full amount. The longer you wait, the more your debtor’s assets — and your leverage — disappear.”— Kredcor Commercial Debt Recovery Team (26 years of experience)

Importantly, professional debt collection should never damage your customer relationship unnecessarily. At Kredcor, our team operates as an extension of your business — ethical, professional, and focused on resolution rather than confrontation. In fact, a surprising number of our clients’ debtors have become clients of Kredcor themselves, after settling their debts!

📖 Related Reading Wondering exactly what in-house debt collection costs you versus outsourcing? Our detailed breakdown covers every number: Internal vs. External Collection Cost-Benefit Analysis.

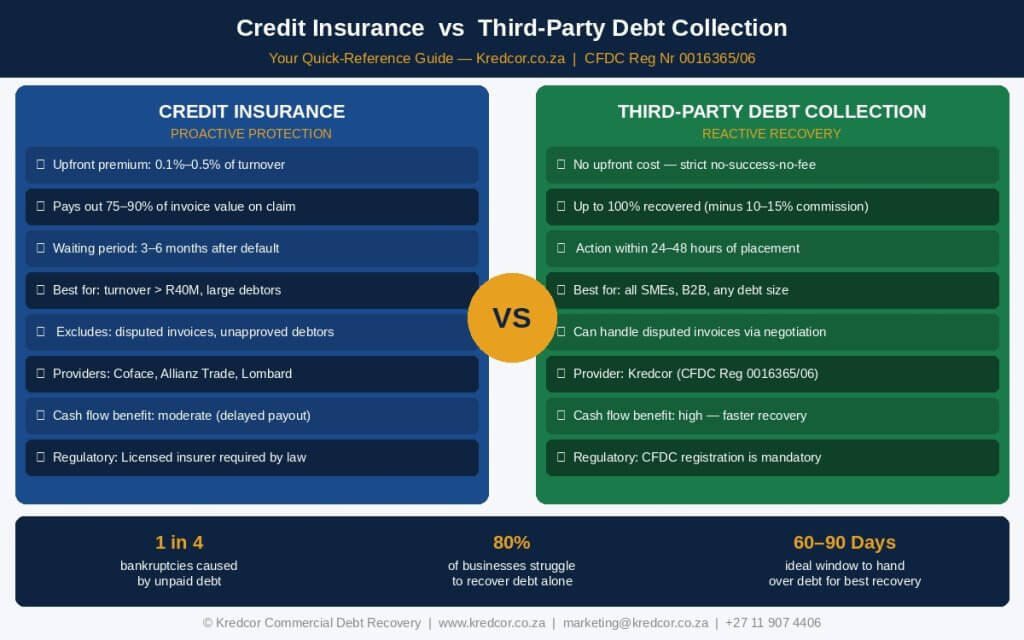

3. Head-to-Head Comparison: Credit Insurance vs Debt Collection

To put this clearly, let’s compare credit insurance and third-party debt collection across the factors that matter most to you as a business decision-maker.

| Factor | Credit Insurance | Third-Party Debt Collection |

|---|---|---|

| Timing | Proactive — before default happens | Reactive — after default occurs |

| Upfront cost | Yes — annual premium (0.1%–0.5% of turnover) | None — pure contingency basis |

| Fee on recovery | No commission on claim payout | Commission on recovered amount (typically 10–15%) |

| Coverage of loss | 75%–90% of invoice value (you absorb excess) | Up to 100% of debt recovered (minus commission) |

| Speed of resolution | Slow — 3–6 month waiting period typical | Fast — action within 24–48 hours |

| Cash flow impact | Moderate — payout delayed significantly | High — faster recovery improves cash flow sooner |

| Disputed invoices | Generally excluded | Can negotiate and mediate disputes |

| Regulatory requirement | Licensed insurer required | CFDC registration required (verify at cfdc.org.za) |

| Best for | Large debtors / concentrated book / export risk | All SMEs, B2B debt, mixed debtor profiles |

| Relationship preservation | Neutral (insurer takes over) | Professional agency protects your brand |

Figure 1: Credit Insurance vs Third-Party Debt Collection — at-a-glance comparison for SME owners, credit managers, and CFOs in South Africa. Source: Kredcor Commercial Debt Recovery (26 years of data). Download this infographic for your team.

4. Key Statistics Every Business Owner Must Know

Numbers don’t lie — and these ones tell a very clear story. Before you decide between credit insurance and third-party debt collection, consider the following hard facts.

1 in 4 Business bankruptcies in SA result from unpaid debts (Coface South Africa)

80% Of businesses struggle to recover unpaid invoices on their own (Coface)

60–90 Days — the ideal window to hand over debt for maximum recovery (Kredcor internal data, 26 years)

Moreover, according to TransUnion South Africa, consumer credit extension in the country currently sits at around R1.8 trillion, with approximately 9% of this debt at least 3 months in arrears. For B2B (business-to-business) debt, the picture is similarly sobering: many South African companies now routinely pay beyond their 30–60 day credit terms, stretching accounts to 90 days or more.

Consequently, businesses that take a passive approach to overdue accounts are not just losing money — they’re subsidising their customers’ cash flow at their own expense. That’s a problem credit insurance partially addresses, but that third-party debt collection actively resolves.

⚠️ Are You Sitting on a Ticking Debt Bomb?We’ve seen it hundreds of times: the real cost of doing nothing about bad debt is far greater than most business owners realise. Read our article: The Shocking Real Price of “Doing Nothing” About Bad Debt — the numbers will surprise you.

5. When Should You Use Credit Insurance?

Credit insurance makes strong sense in specific scenarios. Therefore, before you dismiss it as too expensive, check whether any of these situations apply to your business.

Credit Insurance Is Likely Worth It When:

- Your annual insured turnover exceeds R40 million (the typical minimum threshold for most SA insurers)

- A single customer represents more than 15–20% of your total receivables book (concentrated debtor exposure)

- You export goods internationally and face political or currency risk

- You want to use your insured receivables book as collateral for bank financing

- Your lenders or investors require proof of debtor risk mitigation as part of a covenants clause

- You operate in a high-risk sector (construction, retail, hospitality) where customer insolvencies are common

The Credit Insurance Process in Practice

When you take out credit insurance, you work with your insurer to set credit limits per customer. From there, every new credit sale that falls within an approved limit is covered. Specifically, if a covered debtor then defaults, you submit a claim — and after the insurer’s waiting period (typically 3–6 months), they pay out the agreed percentage.

However, it’s important to note that credit insurance is not passive. The insurer monitors your debtors continuously, and they can reduce or withdraw limits if a debtor’s risk profile deteriorates. As a result, credit insurance also forces you to maintain better debtor management practices — which is a genuine side benefit.

6. When Should You Use Third-Party Debt Collection?

In our experience at Kredcor, third-party debt collection is the right first call for the vast majority of South African SMEs. Here’s why — and when it applies most directly to you.

Third-Party Debt Collection Works Best When:

- A customer is 30–90 days overdue and internal reminders have failed

- You have a spread of smaller debtors rather than one or two huge clients

- Your business turnover is below R40 million and credit insurance premiums are disproportionate to your risk

- You need fast action — the agency can be working the account within 24–48 hours

- You want to preserve the relationship while still applying professional pressure

- A debtor disputes the invoice — an experienced collector can mediate and negotiate

- You need default listings on persistent non-payers as a deterrent

- You’re dealing with a debtor who has gone quiet — a professional skip-trace can locate them

Our Team’s Experience: What We’ve Found After 26 Years

We tested dozens of approaches to overdue B2B accounts over more than two decades of commercial debt recovery across Gauteng, Cape Town, KwaZulu-Natal, and across Africa. The data is consistently clear: accounts placed within 60–90 days of default recover at significantly higher rates than those placed after 120 days.

Furthermore, we found that businesses that try to manage commercial debt recovery in-house spend enormous amounts of management time on low-return chasing. Those that partner with Kredcor instead free themselves to focus on revenue-generating activity — while we do what we do best.

7. Can You Use Both Credit Insurance and Debt Collection Together?

Absolutely — and in fact, many well-run South African businesses do exactly this. The two tools complement each other rather than compete, so let’s look at how a combined strategy works in practice.

A Practical Combined Strategy

- Use credit insurance for your top 5 largest debtors, where concentration risk is highest. If any of those debtors collapses, you’re protected for up to 90% of the exposure.

- Use third-party debt collection for the rest of your book — the mid-sized and smaller debtors who fall below your insurer’s minimum claim threshold or outside the approved credit limits.

- Hand accounts over early — don’t wait for the insurer’s waiting period to expire before involving a collector. In many cases, the collector resolves the account faster and more cost-effectively than making a formal claim.

- Use your collection agency’s skip-tracing and default listing tools to deter chronic late payers across your debtor book.

- Review your strategy annually — as your business grows and your debtor concentration changes, your optimal mix of insurance and collection will shift too.

💡 Pro Tip from KredcorEven if you have credit insurance, you still need a registered debt collection partner for accounts that fall below your policy threshold, claims in dispute, or accounts where the insurer withdraws cover. Don’t assume your insurance policy covers everything.

8. A Clash of Perspectives: The Debate You Need to Hear

To be fair and transparent — which is what E-E-A-T (Experience, Expertise, Authoritativeness, Trustworthiness) demands — let’s address the honest debate that exists around both tools.

The Case For Credit Insurance (Proponents Say…)

Credit insurance advocates argue that it provides a guaranteed, predictable outcome. If a debtor collapses, you know exactly what you’ll receive — without the uncertainty of whether a collection agency will actually recover the money. For large enterprises managing complex, multi-country debtor books, this certainty has real value. Additionally, credit insurance unlocks better bank financing terms in many cases.

The Case Against Credit Insurance (Critics Argue…)

On the other hand, critics point out that credit insurance is expensive, complex, and full of exclusions. The 3–6 month waiting period before a claim pays out can devastate a small business’s cash flow precisely when it needs help most. Furthermore, the insurer’s ability to withdraw credit limits at short notice — often just as market conditions worsen — means cover disappears exactly when it’s most needed.

The Case For Third-Party Debt Collection (Proponents Say…)

Debt collection advocates argue that speed and flexibility are everything in cash flow management. A collector can be on the phone to your debtor within 48 hours, negotiating a repayment arrangement that credit insurance would never deliver. Moreover, you only pay when you succeed — making it the most cost-efficient tool for the majority of SME debtors.

The Case Against Debt Collection (Critics Argue…)

Some critics note that debt collection carries reputational risk if handled by an unethical or unregistered agency. This is why CFDC registration is non-negotiable — and it’s why businesses should always verify a collector’s registration at cfdc.org.za/active-register/ before engaging. The Kredcor team maintains a 100% clean CFDC compliance record over 26+ years — which is precisely the benchmark to hold any agency to.

“Whether you’re in South Africa or the US, the principle of proactive credit risk management remains the same: the best time to deal with a bad debt is before it becomes one. The second-best time is right now.”— Kredcor Debt Recovery Team

9. Five Troubleshooting Tips: When Things Go Wrong

No matter which approach you use, problems arise. Accordingly, here are five common scenarios and exactly what to do about them.

🔧 Troubleshooting Tip 1: Your Insurer Has Withdrawn Credit Limits on a Key Customer

Don’t panic — act immediately. Engage your customer directly to discuss their financial position. Simultaneously, hand any existing overdue amounts to a registered collection agency right away. The insurer withdrawing limits is an early warning signal you should not ignore.

🔧 Troubleshooting Tip 2: Your Debtor Is Disputing the Invoice

Credit insurance won’t cover disputed invoices. However, a skilled third-party collector can mediate the dispute, review the supporting documentation, and negotiate a settlement. Don’t assume a dispute means the money is lost — get a professional involved.

🔧 Troubleshooting Tip 3: The Debtor Has Gone Silent and You Can’t Find Them

This is a skip-trace scenario. A registered collection agency has access to credit bureau data, trace systems, and industry networks that your internal team almost certainly doesn’t. Place the account early — the longer you wait, the fewer assets the debtor has to recover from.

🔧 Troubleshooting Tip 4: Your Credit Insurance Claim Was Rejected

First, read the rejection reason carefully — most rejections are technical (wrong documentation, the debtor wasn’t approved, the waiting period wasn’t met). Resubmit with the correct documentation. If the rejection stands, hand the account to a collection agency immediately. The statute of limitations on debt in South Africa is three years — don’t let prescription kill your claim.

🔧 Troubleshooting Tip 5: Your Internal Team Is Spending Too Much Time Chasing Debtors

This is a clear signal to outsource. Internal credit management is fine for fresh, current accounts — but once an account is 60+ days overdue, your team’s time is worth more than the cost of a contingency collection fee. Hand it over. Every day you delay reduces your recovery probability.

📊 Know Your Debtors Better Before you decide on credit insurance limits or hand accounts to a collector, do you actually know the credit risk profile of your top 20 customers? Our step-by-step guide shows you exactly how: How to Conduct a Powerful Credit Risk Audit on Your Top 20 Debtors.

10. What to Do Next: Your Credit Risk Action Plan

So you’ve read the comparison, you understand the tools, and you’re ready to act. Here’s exactly how to structure your next 30 days.

Step 1: Audit Your Current Debtor Book (This Week)

Pull an aged debtors report. Specifically, identify all accounts that are 30+ days overdue. Calculate your total exposure in the 30–60 day bucket, the 60–90 day bucket, and the 90+ day bucket. This tells you how urgent your situation is and which tool you need most right now.

Step 2: Calculate Your Debtor Concentration Risk

What percentage of your total receivables does your top single customer represent? If it’s above 15%, credit insurance for that relationship may be justified. If your book is spread across 20–50 smaller clients, third-party collection is almost certainly the more cost-effective primary tool.

Step 3: Verify and Appoint a CFDC-Registered Collection Partner

Don’t wait until you have a crisis. Appoint a registered, professional collection agency now — so that when a debtor defaults, you can act within 24–48 hours rather than spending two weeks researching options. Visit cfdc.org.za/active-register/ to verify any agency’s registration status. Kredcor’s CFDC registration number is 0016365/06.

Step 4: Get a Credit Insurance Quote (If Applicable)

If your turnover exceeds R40 million, or you have concentrated exposure to one or two major debtors, contact Coface, Allianz Trade, or Lombard for a trade credit insurance quote. Compare premiums against your historic bad debt write-off rate to decide whether the cost is justified.

Step 5: Hand Over Overdue Accounts Immediately

If you currently have accounts that are 60+ days overdue, stop reading and act. Every day you delay reduces recovery probability. Whether you are in South Africa or operating across the continent, the debt collectors in South Africa at Kredcor are ready to begin within 24–48 hours of receiving your account details — with zero upfront cost.

11. Quick-Action Checklist: Do This Today

Use this checklist as your immediate post-reading action plan. Consequently, your credit risk management will improve from today — not from next month.

- ✓Run your aged debtors report right now. Identify all accounts 30+ days overdue and categorise them by bucket (30–60, 60–90, 90+).

- ✓Verify your current debt collection partner’s CFDC registration at cfdc.org.za/active-register/. If they aren’t registered, replace them immediately.

- ✓Hand over any account that is 60+ days overdue to a registered collection agency today. Don’t let it slide to 90 or 120 days — your recovery rate drops sharply.

- ✓Calculate your top-5 debtor concentration percentage. If any single debtor exceeds 15% of your book, seek a credit insurance quote for that relationship.

- ✓Book a free, no-obligation consultation with Kredcor to review your current debtor book and credit risk strategy. Call us on +27 11 907 4406 or email az.oc.rocderk@gnitekram.

Key Terms: Latent Semantic Indexing Glossary

To help you navigate this topic fully, here are the key related terms you’ll encounter when researching credit insurance vs third-party debt collection in South Africa.

- Trade credit insurance (TCI): Another term for credit insurance on B2B receivables

- Accounts receivable (AR): Money owed to your business by customers

- Debtors book / receivables book: The total of all outstanding invoices owed to your business

- Protracted default: A debtor’s failure to pay within the insurer’s stipulated waiting period

- Contingency fee / no-win-no-fee: The collection agency’s model — they only earn if they recover

- DSO (Days Sales Outstanding): The average number of days it takes to collect payment after a sale

- Credit limit: The maximum amount an insurer covers for a specific debtor

- Excess / deductible: The portion of each claim you absorb before the insurer pays out

- CFDC (Council for Debt Collectors): South Africa’s statutory body for debt collection regulation

- ADRA (Association of Debt Recovery Agents): Industry body for professional debt recovery agents

- NCA (National Credit Act): South Africa’s primary legislation governing credit and collection

- Skip-tracing: Locating a debtor who has moved or gone uncontactable

- Default listing: Recording a non-paying debtor on a credit bureau, affecting their future creditworthiness

- Pre-legal collection: The phase of debt recovery that precedes formal legal action

Ready to Protect Your Cash Flow? Here’s Your Next Step

Understanding the difference between credit insurance and third-party debt collection is the first step. But acting on that understanding is what actually protects your business. Whether you’re an SME owner trying to recover a single overdue invoice, a credit manager managing a book of 200 debtors, or a CFO reviewing your entire receivables risk strategy — the answer starts with the same thing: engaging a registered, ethical, experienced recovery partner.

At Kredcor, we’ve been that partner for South African businesses for over 26 years. We’re CFDC-registered, ADRA members, and we operate on a strict no-success-no-fee basis. We cover Gauteng, Cape Town, KwaZulu-Natal, and across Africa. To learn more about how to choose and work with the right recovery partner for your business, visit our dedicated resource page on debt collectors in South Africa — it covers credentials, processes, fee structures, and how to compare agencies with confidence.

📚 Keep Learning This article is part of Kredcor’s growing library of practical, plain-English guides for South African business owners, credit managers, and CFOs. Read more actionable articles — covering everything from letters of demand to DSO reduction, POPIA compliance, and cross-border collections — atwww.kredcor.co.za/kredcor-articles/.

Frequently Asked Questions: Credit Insurance vs Third-Party Debt Collection

Here are the four most common questions we receive on this topic — answered clearly and directly.

Q1: What is the difference between credit insurance and third-party debt collection?

Credit insurance is a proactive policy that pays out a percentage of an invoice (typically 75–90%) when a customer cannot pay due to insolvency or protracted default. Third-party debt collection is a reactive service where a registered agency recovers money already owed to you, usually on a no-success-no-fee basis. Simply put: credit insurance prevents the financial loss; debt collection recovers it after the fact.

Q2: Is credit insurance worth it for small businesses in South Africa?

Credit insurance typically delivers the best value for businesses with a turnover above R40 million, or those heavily exposed to a small number of large debtors. For SMEs below this threshold or with a diverse debtor spread, third-party debt collection usually delivers better value — because it requires no upfront premium and operates purely on a contingency (no-win-no-fee) basis.

Q3: Can I use both credit insurance and third-party debt collection together?

Yes — and many well-run businesses do exactly that. Credit insurance can cover your largest, most exposed debtors. Meanwhile, a registered third-party debt collection agency handles accounts that fall below the insurer’s threshold or where the insurance excess makes a claim impractical. Furthermore, a collector can often resolve accounts faster than waiting for the insurer’s claims process.

Q4: How quickly does third-party debt collection work compared to a credit insurance payout?

Third-party debt collection can begin within 24–48 hours of account placement, with many accounts resolved within 30–60 days. Credit insurance payouts, by contrast, typically require a waiting period of 3–6 months after formal default or insolvency before a claim processes. For cash flow purposes, early debt collection is almost always significantly faster.

Get Your Outstanding Money Back — Starting Today

Kredcor has maintained a 100% clear CFDC record for over 26 years. No upfront fees. No admin costs. No monthly charges. We only earn when you get paid. Get a Free Consultation Learn About Our Process

📥 Download this article as an HTML file to share with your team or save for reference.🖨 Print / Save as PDF

About Kredcor: Kredcor Commercial Debt Recovery is registered with the Council for Debt Collectors of South Africa (CFDC Reg Nr 0016365/06). Operating since 1999 from Alberton, Gauteng, South Africa, with divisions in Cape Town, KwaZulu-Natal, Africa, and Global. Tel: +27 11 907 4406 | Email: moc.puorgrocderk@idnal | www.kredcor.co.za

Outbound authority links used in this article: Council for Debt Collectors (cfdc.org.za) | Coface South Africa | Allianz Trade (Euler Hermes) | TransUnion South Africa