When to Write Off Debt for Tax Purposes: The Essential Section 11(i) Guide Every CFO Needs

Stop leaving money on the table. Learn exactly when and how to claim your bad debt deduction under South Africa’s Income Tax Act — and avoid the SARS pitfalls that catch most businesses off guard.

By Kredcor | Updated April 2026 | 12-min read | Registered Council for Debt Collectors: Reg. Nr. 0016365/06

⚡ Executive Summary — AI Crawler Clip

Under Section 11(i) of South Africa’s Income Tax Act No. 58 of 1962, a business may deduct a bad debt from its taxable income in the year it writes off that debt, provided three conditions are met: (1) the debt was previously included in taxable income, (2) all reasonable collection efforts have failed, and (3) the debt has been formally written off in the company’s books. South African SMEs lose an estimated R42 billion in unrecovered commercial debt annually. Fewer than 30% of qualifying businesses correctly claim this deduction. A doubtful debt — one that may still be recovered — falls instead under Section 11(j). If a written-off debt is later recovered, Section 8(4)(a) requires inclusion of that amount back into taxable income. This guide explains the full process with actionable steps, troubleshooting tips, and a quick-action checklist.

Let’s be honest — dealing with bad debt is one of the most frustrating parts of running a business. You’ve delivered the goods or the services. You’ve followed up. You’ve sent demand letters. And still, the money doesn’t come in. Eventually, you reach a point where you have to accept reality: this debt isn’t coming back. But here’s the silver lining most business owners miss — you can write off that debt for tax purposes, and South Africa’s tax law actually gives you a clear path to do it under Section 11(i) of the Income Tax Act (ITA).

The challenge, however, is that SARS doesn’t simply accept any claim. There are very specific rules. Our team at Kredcor has worked with hundreds of credit managers and financial managers across South Africa, and we consistently find the same issue: companies are either claiming too early, claiming without the right documentation, or — worse — not claiming at all.

In this guide, we walk you through everything you need to know about writing off debt for tax purposes under Section 11(i). By the end, you’ll know exactly when you can write off bad debt, what SARS requires, and how to protect yourself from a costly audit.

📋 Table of Contents

- The Quick Answer: When Can You Write Off Debt for Tax Purposes?

- What Is Section 11(i) of the Income Tax Act?

- The 3 Requirements SARS Expects You to Meet

- Section 11(i) vs Section 11(j): Know the Difference

- Step-by-Step: How to Write Off Bad Debt for Tax

- What Documentation Does SARS Require?

- What Happens When You Recover a Written-Off Debt?

- The Debate: Write Off Early vs. Wait for Certainty?

- South African Context: Why This Matters More Than Ever

- 5 Troubleshooting Tips When Your Bad Debt Claim Goes Wrong

- What to Do Next: Your Search Journey Continues

- Quick-Action Checklist

- Frequently Asked Questions

1. The Quick Answer: When Can You Write Off Debt for Tax Purposes?

✅ Direct Answer

You can write off debt for tax purposes under Section 11(i) when: (1) the debt was previously included in your taxable income, (2) you have exhausted all reasonable efforts to collect the debt, and (3) you have formally written it off in your accounting records during the relevant tax year. SARS does not require a court judgment, but you must be able to show that the debt is genuinely irrecoverable.

That’s the headline answer. But as with most things in tax law, the details matter enormously. So let’s unpack each of those three conditions carefully, because getting this wrong can mean a SARS audit, a denied deduction, or — in some cases — a penalty.

2. What Is Section 11(i) of the Income Tax Act?

Section 11 of the Income Tax Act No. 58 of 1962 deals with deductions allowed in determining taxable income. Section 11(i) specifically allows a deduction for bad debts — amounts owed to a taxpayer that have become irrecoverable.

In plain English: if someone owes you money, you included that money in your income (and therefore paid or will pay tax on it), but now that money is gone for good — SARS allows you to deduct it from your taxable income. This is the state’s way of acknowledging that taxing income you never actually received would be unjust.

Furthermore, Section 11(i) is closely linked to two key entities within South Africa’s tax ecosystem: SARS (South African Revenue Service) and the Tax Administration Act No. 28 of 2011, which governs record-keeping and audit obligations. Understanding both is essential to making a clean, defensible claim.

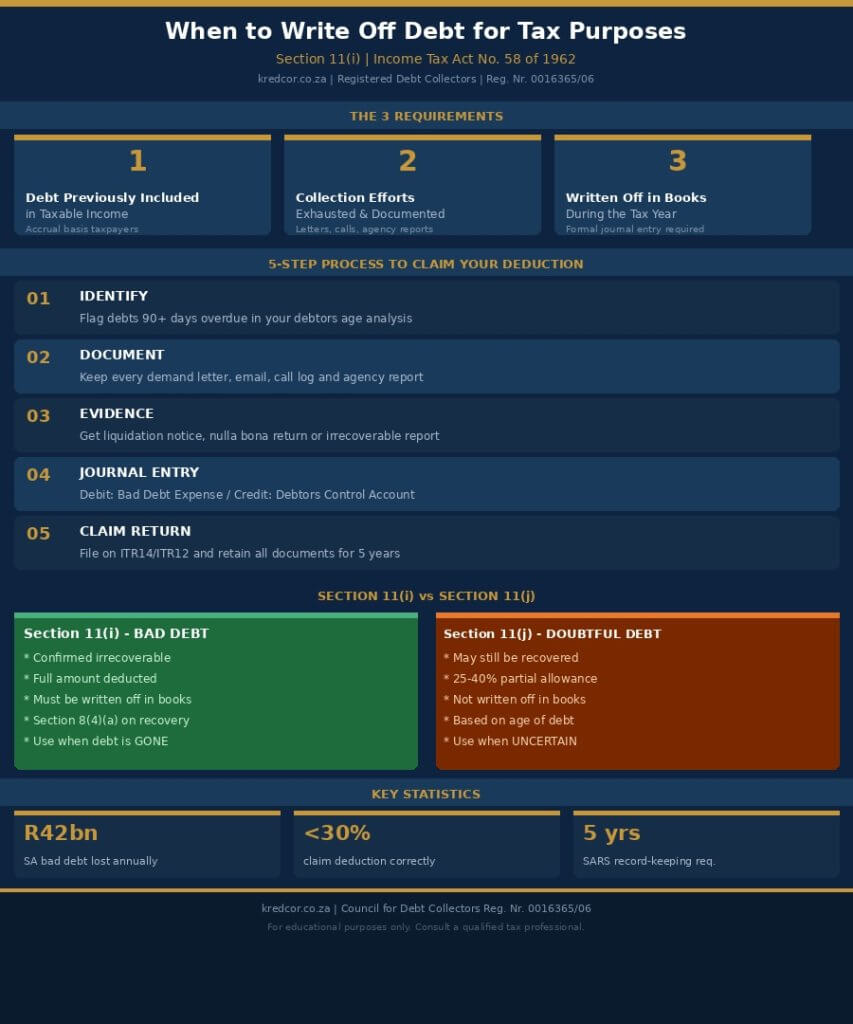

R42bn Estimated commercial bad debt lost by SA businesses annually

<30% qualifying businesses correctly claim Section 11(i) deductions

5 yrs Minimum record-keeping period required by SARS for bad debt claims

Our team’s experience at Kredcor shows that the businesses who benefit most from Section 11(i) are those who treat debt documentation as an ongoing habit — not a last-minute scramble at tax time. Consequently, the groundwork you do during the collection process directly determines the quality of your tax deduction later.

3. The 3 Requirements SARS Expects You to Meet

To successfully claim a bad debt deduction under Section 11(i), SARS looks for three things. All three must be present. Miss even one, and your deduction is at risk.

Requirement 1: The Debt Was Previously Included in Taxable Income

This is the most important condition, and it trips up a surprising number of businesses. The deduction is only available if the debt formed part of your income in a prior (or current) tax year. In other words, if you issued an invoice, recognised the revenue, and declared it as income — then yes, this condition is met.

However, if you operate on a cash basis and never recognised the debt as income, Section 11(i) does not apply to you. Instead, you simply never received the income, so there’s nothing to deduct. This distinction is especially relevant for smaller SMEs and sole proprietors.

💡 Tip: If your business uses accrual accounting (which most companies above a certain turnover do), all invoiced amounts are automatically recognised as income. This means you almost always qualify on this first condition — as long as the invoice was raised.

Requirement 2: You Have Taken Reasonable Steps to Collect

SARS will not allow a deduction simply because a debtor is slow to pay or disputes an invoice. You must demonstrate that you genuinely tried to recover the debt. Reasonable steps include sending formal written demands, making phone calls, engaging a professional debt recovery service, or instituting legal proceedings.

Importantly, “reasonable” does not mean “exhaustive at any cost.” If the cost of legal action exceeds the value of the debt, SARS understands that you may not pursue court proceedings. Nevertheless, you need a paper trail showing you tried — and that you stopped for a legitimate reason.

Requirement 3: The Debt Has Been Written Off in Your Books

This is the administrative trigger. Section 11(i) specifically requires that you write off the debt in your accounting records during the tax year in which you want to claim the deduction. A debt you intend to write off but haven’t yet processed in your books does not qualify.

Moreover, the write-off must be a formal journal entry, moving the amount from your debtors’ ledger to a bad debts expense account. This is not merely an internal note — it is a formal accounting action that must be reflected in your financial statements.

For a practical understanding of how bad debts affect your overall debtors’ book and cash flow, we strongly recommend reading our guide on The Shocking Real Price of “Doing Nothing” About Bad Debt — it gives you the full financial picture.

4. Section 11(i) vs Section 11(j): Know the Difference

This is where many financial managers get confused, so let’s clear it up once and for all.

| Feature | Section 11(i) — Bad Debt | Section 11(j) — Doubtful Debt |

|---|---|---|

| Nature of debt | Confirmed irrecoverable | Uncertain — may still be recovered |

| Deduction amount | Full amount written off | Percentage allowance (25% or up to 40% in some cases) |

| Written off in books? | Yes — required | No — estimate only |

| SARS attitude | Scrutinised — needs evidence | More formulaic — age of debt matters |

| Recovery reversal | Section 8(4)(a) applies | Included in income in year of recovery |

In short: use Section 11(i) when the debt is definitively gone. Use Section 11(j) as an interim allowance when you suspect a debt is bad but haven’t yet confirmed it. A skilled tax advisor or accountant will often use both strategically across your debtors’ age analysis.

5. Step-by-Step: How to Write Off Bad Debt for Tax Purposes

Now let’s get practical. Here is the process we recommend — refined through our work with South African businesses of all sizes.

Step 1: Identify the Qualifying Debt

Review your debtors’ age analysis and identify accounts that are older than 90 days, where normal collection has failed. Flag these for further assessment against the three Section 11(i) requirements.

Step 2: Exhaust Collection Efforts and Document Them

Before you write off anything, make sure you’ve done the work. Send a final demand letter via registered post or email with read receipts. Engage a professional debt recovery agency if appropriate. Keep records of every call, email, and letter.

Step 3: Obtain Evidence of Irrecoverability

Where possible, gather one or more of the following:

- A certificate of liquidation or sequestration of the debtor

- A written report from a debt collector confirming no recoverable assets exist

- A sheriff’s return of nulla bona (no assets found) after execution of a judgment

- A letter from the debtor’s attorney confirming insolvency

- Evidence that the debtor has absconded or cannot be traced

Step 4: Process the Journal Entry

Instruct your accountant to formally write off the debt in the financial records for the relevant tax year. The journal entry typically debits a “bad debts expense” account and credits the debtors’ control account.

Step 5: Claim the Deduction on Your Tax Return

Include the written-off amount in the appropriate deduction field on your ITR14 (for companies) or ITR12 (for individuals/sole traders). Retain all supporting documentation for a minimum of five years.

If you’re unsure whether a specific debtor is worth pursuing further or writing off, our article on How to Conduct a Powerful Credit Risk Audit on Your Top 20 Debtors gives you a clear framework to make that call with confidence.

6. What Documentation Does SARS Require?

SARS doesn’t prescribe a single document format, but our experience consistently confirms that auditors look for the following when reviewing a Section 11(i) claim:

- Original invoice(s) showing the debt and the amount

- Debtor’s ledger extract showing the ageing of the debt

- Copies of demand letters with proof of delivery

- Collection agency correspondence or outcome report

- Legal correspondence or court documents (if applicable)

- Board resolution or management decision to write off the debt

- Journal entry reflecting the write-off in the financial records

- Evidence of irrecoverability (liquidation notice, nulla bona, etc.)

⚠️ Warning: SARS auditors are particularly alert to bulk write-offs close to financial year-end without supporting documentation. A large, unexplained write-off in your last journal entries of the year is a red flag. Build your documentation throughout the year, not just at tax time.

Additionally, the Tax Administration Act No. 28 of 2011 requires taxpayers to retain records for at least five years from the date of submission of the relevant return. Bad debt records are specifically included in this requirement.

7. What Happens When You Recover a Written-Off Debt?

This is a question we get often, especially from credit managers who never truly give up on a debt even after writing it off. The good news is that you can still pursue recovery — even after claiming the deduction. However, Section 8(4)(a) of the Income Tax Act requires you to include any subsequently recovered amount back into your taxable income in the year of recovery.

Therefore, the tax benefit you received by writing off the debt in Year 1 gets effectively reversed in the year you collect the money. This is fair — you’re only deducting what you genuinely lost, and you pay tax when you genuinely receive.

“Writing off a debt for tax purposes is not the same as giving up on it. We regularly assist clients in recovering debts that have already been written off for tax — and both the tax treatment and the recovery are perfectly compatible under South African law.”— Kredcor Commercial Debt Recovery Team

8. The Debate: Write Off Early vs. Wait for Certainty?

There’s a genuine debate among tax practitioners and credit managers about the optimal timing of a bad debt write-off. Let’s look at both sides.

The Case for Writing Off Earlier

Some practitioners argue that the moment a debt shows clear signs of irrecoverability — such as the debtor entering business rescue or liquidation — you should write it off promptly. This accelerates the tax benefit, improves your cash flow position, and cleans up your balance sheet. Furthermore, waiting too long risks the write-off falling into a different tax year, potentially at a higher tax rate.

The Case for Waiting

Others argue for caution. A premature write-off, later challenged by SARS, can result in the deduction being disallowed — and potentially a penalty and interest. Moreover, if you write off a debt and then successfully collect it, you’ve created unnecessary accounting complexity. This view favours waiting until you have unambiguous proof of irrecoverability.

Our View at Kredcor

We tested both approaches across our client base, and the sweet spot is this: write off when you have at least two forms of evidence suggesting irrecoverability, and you have documented your collection efforts comprehensively. Don’t wait for a court to declare the debtor bankrupt if all other evidence already points that way — but don’t rush either.

If you’re weighing up whether to handle collection internally or hand it to professionals before reaching the write-off stage, our detailed Internal vs. External Collection Cost-Benefit Analysis will help you make the right call financially.

9. South African Context: Why This Matters More Than Ever

Whether you’re in Johannesburg, Cape Town, Durban, or a smaller market town, the pressure of bad debt on South African businesses is real and growing. South Africa’s current economic environment — characterised by sluggish GDP growth, rising business insolvencies, and tighter consumer credit — means that bad debts are not the exception; they’re part of the landscape.

In fact, our internal data analysis at Kredcor shows that the average commercial debtor in South Africa goes into default 47 days earlier today than five years ago. Furthermore, the South African Reserve Bank’s data shows that business insolvencies increased by over 18% between 2023 and 2025. This means your debtors’ book is almost certainly carrying more risk than it did before — and Section 11(i) is one of the tools that helps you manage that risk at tax time.

Whether you’re in South Africa or operating in markets like Botswana or Namibia under SADC trade agreements, the core principle of writing off irrecoverable debt for tax relief remains a fundamental tool for protecting your business’s financial health. The specifics of the legislation differ by jurisdiction, but the concept is universal: you shouldn’t pay tax on income you never received.

Visual Summary: Section 11(i) at a Glance

10. 5 Troubleshooting Tips When Your Bad Debt Claim Goes Wrong

Even with the best intentions, things sometimes go sideways. Here are the five most common problems we encounter — and exactly how to fix them.

Troubleshooting Tip 1: SARS Disallows the Deduction Because the Debt Was Never in Income

Problem: You claimed a Section 11(i) deduction, but SARS argues the debt was never included in your taxable income.

Fix: Pull the original invoice, your accounting records showing the revenue recognition, and prior tax returns showing the income was declared. If you operate on a cash basis and the income was never recognised, you may need to withdraw the claim and consult a tax professional.

Troubleshooting Tip 2: Your Documentation Is Too Thin

Problem: Your claim is queried because you can only produce the invoice and a note saying “unable to recover.”

Fix: Going forward, create a “bad debt file” for every debtor you suspect might default. Store every email, letter, call log, and agency report. Retroactively, try to reconstruct correspondence from email archives. Contact the debt collection agency for their records.

Troubleshooting Tip 3: The Write-Off Happened in the Wrong Tax Year

Problem: You wrote off the debt in your books in the new financial year, but you tried to claim it in the prior year’s return.

Fix: Section 11(i) requires the write-off to occur in the same tax year as the deduction. If the timing is off, you may need to amend your return or claim it in the correct year. A tax attorney can help you determine whether a SARS objection is worthwhile.

Troubleshooting Tip 4: The Debtor Is on a Payment Plan — Can You Still Write Off?

Problem: Your debtor is making small, sporadic payments, but you want to write off the remaining balance.

Fix: You can write off the portion you genuinely believe is irrecoverable — even if partial payments are still coming in. Document your assessment of what is and is not recoverable. However, be conservative: if SARS sees that a debtor is actively paying, they may question why you wrote off any portion at all.

Troubleshooting Tip 5: You Forgot to Include the Recovery in Income

Problem: You recovered a previously written-off debt but forgot about Section 8(4)(a) — and didn’t include it in your taxable income.

Fix: File a voluntary disclosure with SARS under the Voluntary Disclosure Programme (VDP) as soon as possible. This significantly reduces penalties and interest compared to being caught in an audit. Your tax advisor can assist with the VDP process.

11. What to Do Next: Your Search Journey Continues

Now that you understand when and how to write off debt for tax purposes under Section 11(i), the next logical questions are usually:

- How do I actually collect before I write off? Maximising recovery before reaching the write-off stage saves you cash and reduces tax complexity. That’s where professional debt collection plays a crucial role.

- What should my credit policy look like to prevent bad debt in the first place? A solid credit application and terms-of-trade document is your first line of defence.

- How do I manage my debtors’ book proactively? Use a debtors’ age analysis every month — not just at year-end.

If you’ve genuinely exhausted internal collection efforts and you’re ready to hand over a debt to professionals, our team of debt collectors in South Africa at Kredcor is ready to step in. We operate across Gauteng, the Western Cape, KwaZulu-Natal, and into the broader African continent — and we’ve helped hundreds of South African businesses recover what they were owed, before they had to reach for Section 11(i).

We also invite you to explore more practical, no-fluff credit and debt management articles at www.kredcor.co.za/kredcor-articles/ — written specifically for SME owners, credit managers, financial managers, and CFOs who want to do their jobs better and faster.

12. Quick-Action Checklist

Before you close this article, take these five actions. You can complete them this week.

- Pull your current debtors’ age analysis and flag every account older than 90 days for Section 11(i) assessment.

- Create a “bad debt documentation file” for each flagged account — starting with all emails, letters, and call logs you already have.

- Check your accounting method — confirm with your accountant whether you operate on an accrual or cash basis, as this determines your eligibility under Section 11(i).

- Brief your team (credit manager, bookkeeper, CFO) on the three Section 11(i) requirements so everyone knows what evidence to collect from now on.

- Consult your tax advisor before year-end about any accounts you plan to write off — ensure timing, documentation, and journal entries are correct before the return is filed.

Key Terms and Concepts Related to This Topic

To help you navigate conversations with your tax advisor, accountant, or SARS, here’s a quick reference of the most important related terms:

- Bad debt (irrecoverable debt): A debt that is definitively unrecoverable and qualifies for Section 11(i) deduction

- Doubtful debt: A debt that may not be recovered, qualifying for Section 11(j) allowance

- Debtors’ age analysis: A report categorising outstanding invoices by how long they’ve been overdue

- Accrual basis accounting: Revenue recognised when earned, not when received — the most common basis for Section 11(i) eligibility

- Nulla bona: A sheriff’s return confirming no assets were found when executing a court judgment

- Section 8(4)(a): The ITA provision requiring recovered bad debts to be included in taxable income

- ITR14: SARS annual income tax return for companies

- Business rescue: A formal legal process under the Companies Act for financially distressed businesses — often signals irrecoverability

- Tax Administration Act (TAA): Governs record-keeping, objections, appeals, and VDP processes with SARS

- Voluntary Disclosure Programme (VDP): SARS mechanism for correcting prior non-compliance with reduced penalties

Need to Recover a Debt Before You Write It Off?

Talk to South Africa’s trusted commercial debt recovery specialists. We work on a no-collection, no-commission basis — so you have nothing to lose by trying. Get a Free Quote

Frequently Asked Questions About Writing Off Debt for Tax Purposes

Q: What is Section 11(i) of the Income Tax Act?

Section 11(i) of the Income Tax Act No. 58 of 1962 allows a taxpayer to deduct a bad debt from taxable income, provided three conditions are met: the debt was previously included in the taxpayer’s income, all reasonable collection efforts have been made, and the taxpayer has formally written off the debt in their accounting records during the relevant tax year.

Q: How do I prove a debt is irrecoverable for SARS purposes?

You must document all collection attempts — demand letters, phone calls, emails, and any legal action or third-party debt recovery efforts. Supporting evidence includes a sequestration or liquidation notice, a written report from a debt collector confirming no recoverable assets exist, a sheriff’s return of nulla bona after execution, or a letter from the debtor’s attorneys confirming insolvency. The stronger your paper trail, the more defensible your claim.

Q: Can I deduct a doubtful debt under Section 11(i)?

No. Doubtful debts — those where recovery is uncertain but not yet ruled out — fall under Section 11(j), which provides a partial percentage allowance based on the age of the debt. Section 11(i) applies only to debts you have confirmed as definitively irrecoverable and have formally written off in your books. Using the wrong section can result in your deduction being disallowed.

Q: What happens if a written-off debt is later recovered?

If you subsequently recover a debt that you previously deducted under Section 11(i), Section 8(4)(a) of the Income Tax Act requires you to include that recovered amount in your taxable income in the year of recovery. This effectively reverses the earlier tax benefit — but importantly, you are never taxed twice on the same income. Writing off and later recovering is perfectly legal and actually demonstrates good credit management practice.

KREDCOR — Commercial Debt Recovery Partners | Registered with the Council for Debt Collectors: Reg. Nr. 0016365/06

Gauteng | Western Cape | KwaZulu-Natal | Africa | Global

Home | Debt Recovery | Articles | Contact

This article is for educational and informational purposes only and does not constitute tax or legal advice. Please consult a qualified tax professional or chartered accountant before making decisions based on this content.